Banking 1Q20

Banks are fighting a war on multiple fronts at the moment…

Low rates pinching net interest margins

Coronavirus impacting their profitable business clients

Unemployment / shutdowns impacting their profitable consumer clients

First quarter earnings highlighted the impact of these battles:

A few charts from 1Q20 earnings releases tell the story…

Wells Fargo (WFC) reached deep into its pockets to pull out the 1 penny earnings number in the first quarter.

They did take an extra $3.2bn in provisions for loan losses compared to 1Q19, but even adjusting for that you’re looking at declining revenue and earnings by a good amount. Net interest margins fell to 2.58% (from 2.91%) in Q1.

WFC suffered some body blows in 1Q20. Not just from the $3.8bn in reserves added, but also in the $1.4bn loss on equity securities (compared to a gain of $814m in 1Q19). Even adjusting for these amounts, pre-tax earnings still would have been down 15%!

JPMorgan (JPM) wasn’t much better… Although the business looks more “flat” than “decline.” Reserves of $8.3bn dented earnings but even normalizing that leads to a 12% pre-tax earnings decline from last year.

Citigroup (C) probably fared best in revenue performance over the past 5 quarters. Particularly helpful was a $5.3bn piece of revenue from “principal transactions” (i.e. investing/trading on behalf of their own account). Without this, revenue is essentially flat for the past 5 quarters. Citi took $4.3bn in additional reserves.

Bank of America (BAC) is more of the same… $4.8bn in reserves. Pre-tax earnings flattish even adjusting for that amount. Flat-to-declining revenue over the past 5 quarters.

Adjusting each banks’ earnings for the additional provisions — WFC, JPM, and BAC still saw YoY declines in pre-tax earnings while C was bolstered by its trading gains (without which the bank would have barely been profitable during the quarter).

All of the big banks have been deploying massive amounts of cash into dividends and share repurchases lately which have dented the level of equity cushion. Sure, balance sheets are in much better shape than they were going into 2008. But they have all deteriorated over the past 5 quarters by a decent amount (defined as equity to assets).

Today, each of the banks are trading at roughly:

Citigroup — 0.5x book value

Wells Fargo — 0.72x

Bank of America — 0.8x

JPMorgan — 1.2x

These are pretty stark differences! Some of these banks are more into trading and other services. Wells has net loans equal to about 50% of total assets while JPM and Citi are about 31-32% and BofA at 40%.

JPM and Citi have much larger amounts of trading assets on their balance sheet (i.e. positions trading on their own behalf) at 16-17% of total assets. Wells is more of a traditional lender with lots of residential mortgages. Trading assets at Wells and BofA are in the 4-7% range of total.

Interesting the valuation difference between JPM and Citi… Citi has had arguably the most consistent earnings levels over the past 5 quarters at $4.7-5bn AND they had a huge trading gain in Q1.

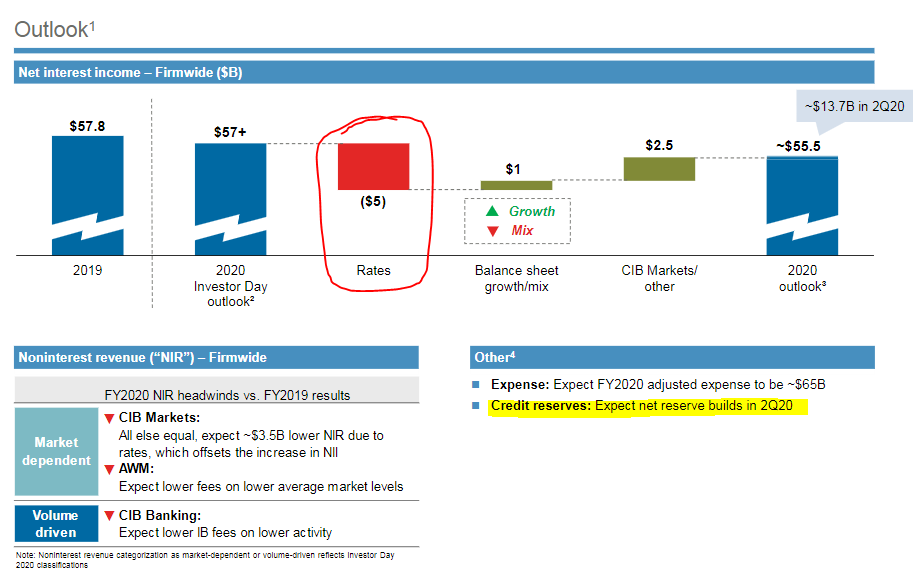

I think this slide tells the current banking story best of all…

From JPM:

A 10%-ish impact from lower rates before considering coronavirus

Further reserve building in Q2 as businesses and consumers continue to be impacted by shutdowns

Hard to tell how deep the loan losses will go from small business and consumer pain…