Case Study: Stub Shares

A look at my 2014 investment in Symmetry Surgical + a few actionable ideas in the "stub" category

Let’s say you find a situation where a company decides to sell a large portion of their business and return those cash proceeds to shareholders.

What happens to the “small portion” of that business?

Those are stub shares.

Every single one of these situations is worth your time.

Not long ago, I wrote a “guide to asset plays,” which briefly touched on stub shares. Here’s what I wrote about them:

…when the majority of a company will be acquired leaving a “stub” business behind. In these cases, shareholders typically receive a large cash distribution and a smaller portion of their holding in the stub business.

These are rare, but always worth a look.

Pure arbitrageurs can’t own them because of the volatile stub value; and unlike the selling pressure in a traditional spin-off, there’s pent-up buying pressure because most investors can’t or won’t put up $1 to get a 20c position. For example, if you wanted a 5% position in the stub, you’d likely have to buy a 20-30% position pre-close.

Let’s look at a case study from an investment I made back in 2014…

Prices are going up on June 1st (for the first time in 8 years)

This is your chance to lock-in today’s price of $20/month or $200/year

After June 1st, prices will jump to $25/month or $250/year

I’m biased, but this is an excellent value for high quality special sits research :)

Case Study: Symmetry Medical

It was summer 2014 and Tecomet announced they would acquire the OEM Solutions business from Symmetry Medical (SMA) for $450m.

After repaying all debt, Symmetry planned to distribute $7.50 per share to investors and the stock was trading around $9.

But they also owned a small distributor of surgical instruments which would be spun off to shareholders at closing at an implied price of $1.77 per share.

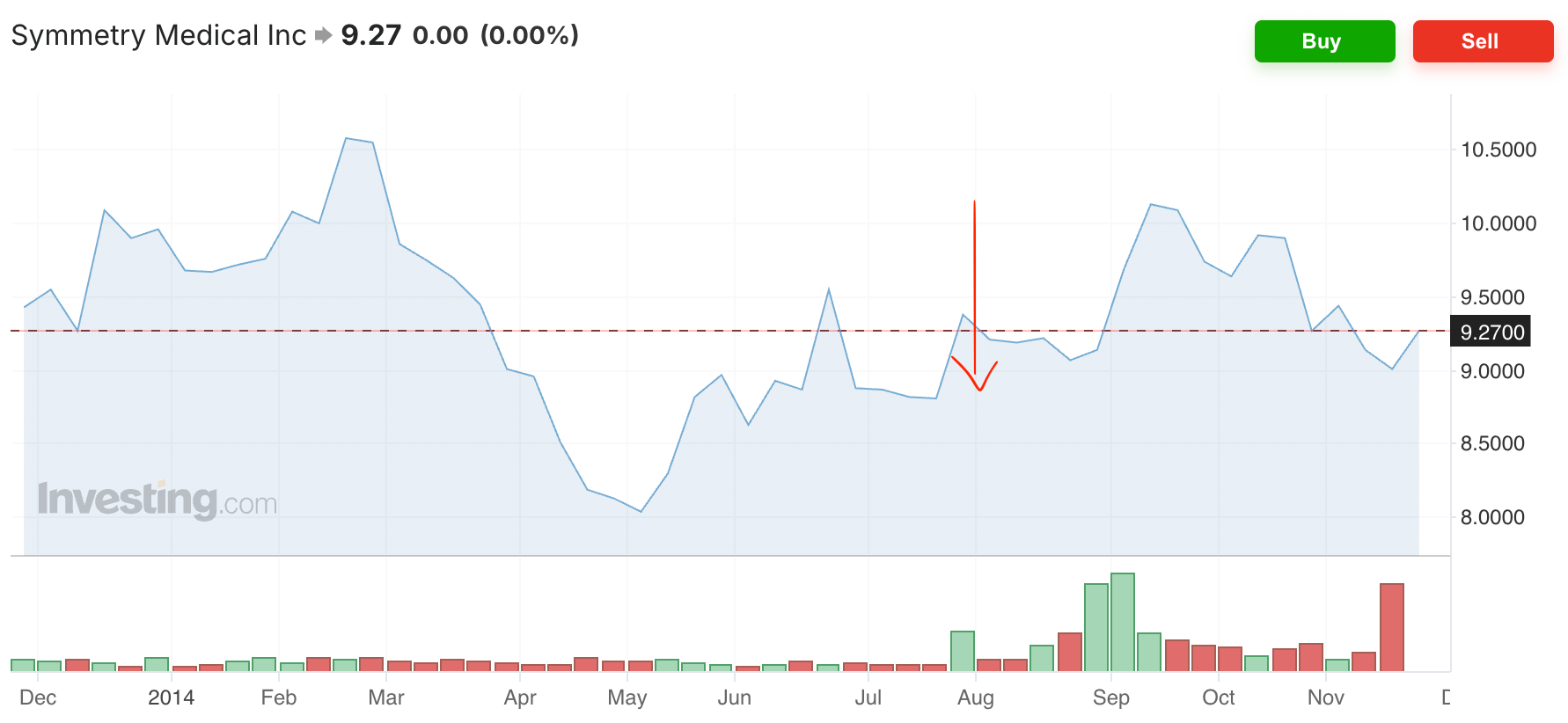

Symmetry Medical (SMA) — the pre-close business

Shares outstanding: 37.6m (10-Q, 3Q14)

Price: $9.27

Market cap: $350m

Cash distribution: $7.50

Stub share price: $1.77

Forget about the fundamentals of the OEM Solutions business or what multiple the combined SMA was trading at pre-close, those details are irrelevant.

Symmetry Surgical (SSRG) — the stub business

Inside SMA was a niche distributor of surgical instruments. They carried 20,000 products sold to thousands of hospital/GPO customers in a tiny corner of the surgical instruments market.

At the time I started looking, SSRG was roughly 20% of the pre-close SMA share price. Meaning: you’d have to put up $1.00 just to get a 20c position.

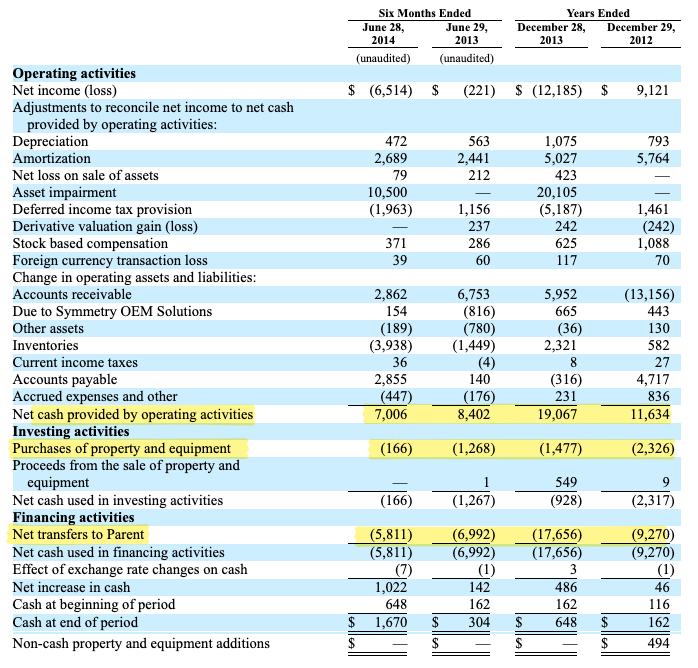

So I opened up the spin documents (in this case an S-4 prospectus) and flipped straight to the standalone cash flows…

This surgical division threw off $17.6m FCF in 2013, $9.3m in 2012, and $6.8m in the first half of 2014. That was $33.7m combined FCF over a 2.5 year stretch with an implied market cap of $68m.

No need to look further, I’m already in…

If only it were that simple…

Next, I looked at the revenue trends.

Here’s a timeline of performance since 2009 when the segment was first disclosed inside SMA:

2009 — $26m segment revenue

2010 — $35m revenue

2011 — $39m revenue (spent $176m on 2 acquisitions in late 2011)

2012 — $107m revenue (+175% from 2011 due to the acquisitions)

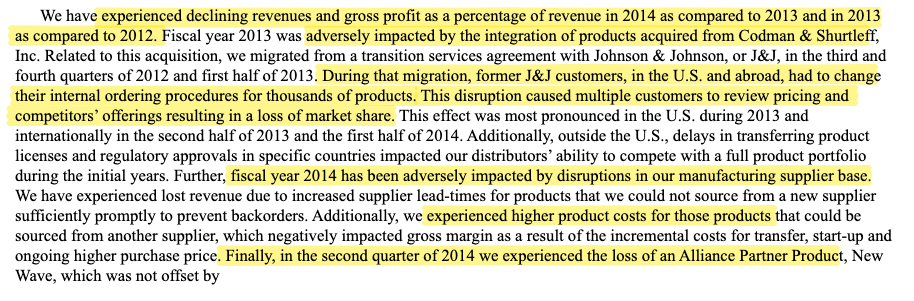

2013 — $89m revenue (-17% from 2012, integration challenges)

2014 — $85m TTM revenue (-8% through 6 months of 2014)

Ouch. Those 2011 acquisitions weren’t looking so good…

Turns out, Symmetry botched the hand-off from J&J which led to price & volume declines in 2013-2014. Adding to the pain, a key product line was acquired by Covidien/Medtronic in mid-2014.

Fortunately, there were some green shoots…

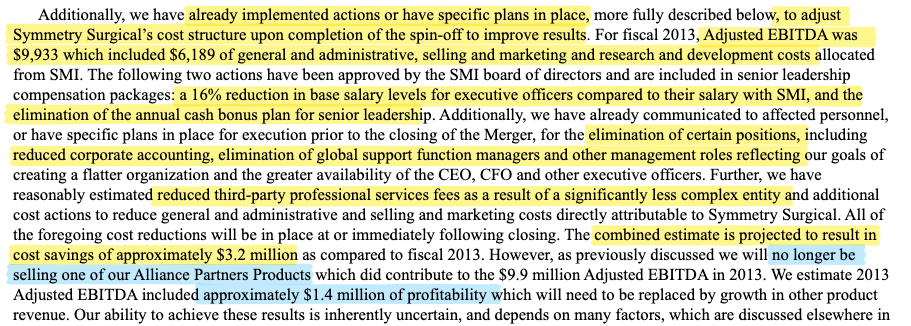

First, management was excited about this business, and the team running pre-close SMA was staying to run the much smaller SSRG. Before joining SMA in early 2011, the CEO previously ran J&J’s DePuy ortho unit which SSRG acquired in late 2011. Hmm…

Second, as is the case in most of these stub situations, the spin-off was well capitalized with no debt and plenty of net working capital ($22m at closing). It was also a highly cash generative business with minimal capex needs.

Last, several cost saving initiatives (including reducing management comp) were already in place… these savings totaled $3.2m and were offset by $1.4m of lost profitability on the lost product line.

So what happened?

The transaction closed in December 2014, with the following characteristics

Share count: 9.6 million (1 SSRG share for every 4 SMA shares)

Share price: $7.08 ($1.77 pre-spin)

Market cap: $68m

Net debt: $0

Trailing EBITDA: $9.9m (6.9x)

Trailing FCF: $10.8m ex-WC (6.3x P/FCF)

Over the next 5 quarters after closing — revenue bottomed (4% growth in 2015 & 2% growth in 1Q16) and FCF totaled $16.4. From a capital allocation standpoint, they made a single $4m acquisition and net cash piled up to $11m.

Shares steadily climbed as progress was made.

End result?

The stub business was acquired 18 months after the spin-off by a healthcare-focused PE firm for $13.10 per share (an 85% premium to the initial spin price). Based on 2016 guidance of $9.5-11m EBITDA, this was an ~11x EBITDA exit multiple.

What made this work & why are stub shares worth your time?

Aside from the business itself and the fundamentals, a few factors contributed to this idea:

Because they stem from a sale + spin backdrop, most stub businesses start with clean balance sheets and plenty of cash to operate/grow

Stub shares are very small relative to the pre-close trading price, so they’re easily overlooked by most investors (or most investors are unwilling to put up the capital required to buy them ahead of closing) — the bigger the “ratio,” the better here

It’s hard (impossible?) to arbitrage these situations since most have only 70-80% of the pre-close share price coming back via cash distribution… there’s no way to arb the stub/spin business

Then you get the traditional post-spin dynamics — a more focused standalone company, right sizing cost structures, pursuing growth plans, gaining more investor attention, etc.

Happy hunting!

Colin

P.S. if you’re looking for more situations in this category, there are 2 timely ideas out there:

Enviri (NVRI) — this one closes on June 1st, so the stub business is just getting started (link to my write-up)

Green Dot (GDOT) — the spin-to-distribution ratio isn’t as wide as I’d like, but it’s still compelling… this stub will create a well-capitalized bank-as-a-service (BaaS) company (link to my write-up)

P.P.S if you enjoyed this write-up, give it a “like” and consider upgrading to become a paid subscriber :)

Have you looked at VISN stub?