Quick Value 11.28.22 ($GPN)

Global Payments - big cap payment processor at 10x earnings (vs. 20x historic average)

Market Performance

Market Stats

Oil prices have been rolling over while oil stocks continue to do well this year (h/t Charlie Bilello from Twitter)

Quick Value

Global Payments ($GPN)

This one was mentioned on a twitter thread as a suggested stock and after pulling up the chart I was surprised to see 5yrs of no movement (a setup I quite like). On top of that, valuations in this entire industry have gotten slammed… hmm?

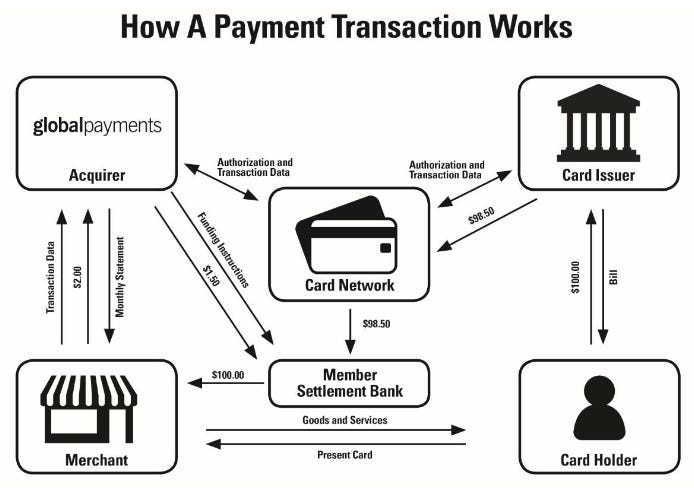

What they do…

This industry confuses the hell out of me to be honest. Visa/Mastercard seem obvious as the credit card networks. A layer beneath that you have these merchant acquirers (i.e. GPN) which help facilitate credit card purchases.

GPN states they are one of the largest merchant acquirers in the small/medium business segment — i.e. customers with credit card sales of $5m or less. They serve 4m merchant customers and 1350 financial institutions.

Why it’s interesting…

1) Industry valuations look cheap — This was a surprise as I’ve always written off this industry as too expensive for my taste. When plugging the group into my table, I see GPN/FIS at 10x earnings, FLT not far behind at ~11x, and FISV at 14x. These aren’t very levered businesses and they all generate good cash flow.

Side note — I haven’t looked into any other competitors (yet) so I don’t have a theory as to why shares are down across the board other than potential weakness in macro/consumer and rising competition.

2) Stocks trading way below long run averages — As we saw above, both GPN/FIS are trading at 10x earnings vs. 5yr averages closer to 20x. Interesting that these businesses historically commanded a premium to the overall market yet now they trade at a very wide discount.

3) Growth — GPN has been an acquisitive company but they’ve done a nice job growing revenue and earnings. Analyst estimates call for that to continue in 2022-2024 (as does management). Back at their 2021 investor day, the goal was 10%+ revenue growth and high teens to low 20% EPS growth through the cycle.

4) Cash flow and capital allocation — Below is a timeline of cash generation dating back to 2013. A few notable events were the $24bn merger with TSYS in 2019 (using equity) and several deals totaling ~$1.9bn in 2021.

M&A has been the top priority with buybacks as a close second. In 2021, GPN did a big levered buyback at ~$200/share in addition to the $1.8bn+ in acquisitions. So far in 2022, they’ve repurchased another $2bn in stock. Share count is down ~10% since the TSYS merger and 5% so far in 2022.

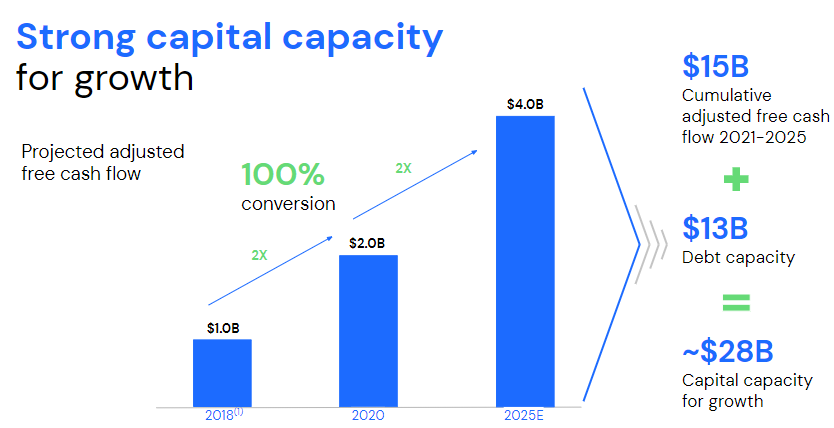

Last on the cash flow… I thought this chart from the 2021 investor day was interesting… GPN today is a ~$28bn market cap. This chart shows $28bn of FCF + borrowing capacity available for capital allocation. That’s 100% of the current market cap through 2025! They’ve already spent a big piece of this in 2021 and YTD 2022 but the point remains: GPN is likely to deploy at least half it’s market cap from today through 2025…

I’ll need to add the other payment processors to my list to truly understand what’s going on in the industry… but at first glance, this looks like a cheap stock…

As a small company, you can't "sign up" directly with VISA, Mastercard etc. You have to sign up with someone like GlobalPayments, who themselves have the relationship with visa etc. So Global Payments recharge you the Visa fee, plus they add on their charge.

You might want to check out Repay Holdings Corp (RPAY). Insiders bought large numbers of shares.