Quick Value #191 - John Wiley & Sons ($WLY)

10.30.23 - 12x earnings; new management buying stock; asset sales on the block

Today’s post covers an interesting turnaround situation. Really (really) bad capital allocation cratered this stock…

Old management out, new management in — It’s pretty obvious the outgoing CEO got this company into their current mess; and the interim CEO just dropped >$500k on open market purchases.

Valuation below history & peers — I believe this mainly ties into #1 above. Bad capital allocation led to the current trading multiple. Not great for long-time shareholders but anyone looking anew won’t pay for their past sins.

Asset sale catalyst — Alright, the real catalyst is #1 with management leaving, but they’re also selling businesses with $315m in book value and >$300m annualized sales, >13% of enterprise value.

Halloween and horror movies are a favorite of mine… with that, here’s a spooky special promo with a secret reference to a horror movie I like!

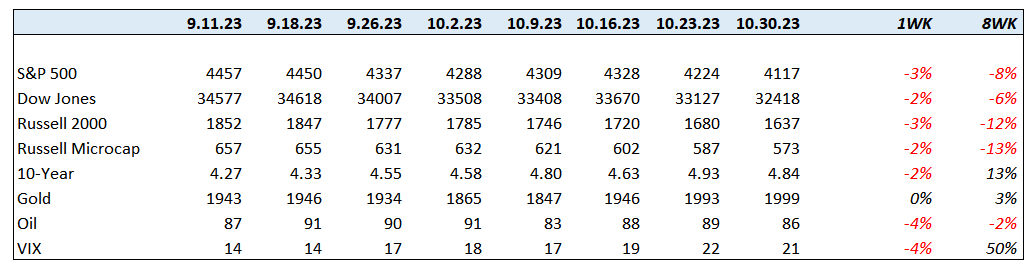

Market Performance

Quick Value

John Wiley & Sons ($WLY)

This stock popped onto my radar after noticing a large insider purchase (>$500k) by the “Interim CEO,” which naturally caught my attention.

It didn’t take long to realize this one was worth a closer look.

What they do…

Wiley is a 200 year old company founded on publishing but later expanded into academic and research journals. Today, more than 80% of revenue comes from digital products and 50% is recurring in nature.

There are 3 segments:

Research — Publish over 1900 research journals (like American Cancer Society, American Heart Association, etc.). Revenue model mostly centers on recurring subscriptions.

Academic — Includes book publishing (both commercial and education end markets) and university services, which offers backend services to colleges. Still a heavy mix of digital products in this segment (>65%) but revenue is not recurring.

Talent — Corporate training and personality/team assessments. Think of this as online courses for big companies to help uplevel talent.

Why it’s interesting…

1) Old management out, new management on the way

The former CEO for the past 6 years abruptly resigned (was fired?) leaving a board member to take the interim CEO position where he then purchased >$500k worth of stock. There wasn’t much color around the change so I’m reading it as frustration around performance.

About that performance — this stock has underperformed the market since 1989 (!!!) and produced negative total returns over the last 10 years. That is impressively terrible.

What’s interesting is that the fundamentals aren’t that bad!

Some of you might disagree since earnings haven’t grown in more than a few years and FY24 will be down significantly; but here’s what I like about it…

The business is remarkably stable (and typically investors are willing to pay more for less volatility)

Minimal COVID impact — no spike in working capital, no supernormal profits, just steady

Lots of cash generation with the preferred use of that cash as dividends (4.7% yield) and to a lesser extent buybacks

I need to highlight just how bad the outgoing CEO was for this company… Brian Napack took the job in 2018 and subsequently made $800m in acquisitions over 6 years, totaling >70% of all FCF generated during that period ($1.1bn). Most of those acquisitions were done at 5-10x revenue for money-losing technology assets. Now, interest rates are resetting and those deals are contributing zero to the bottom line. Ouch.

Fortunately for new prospectors, this guy is out and the share price has been hammered to reflect these moves!

2) Cheap valuation and earnings growth (in a few years)

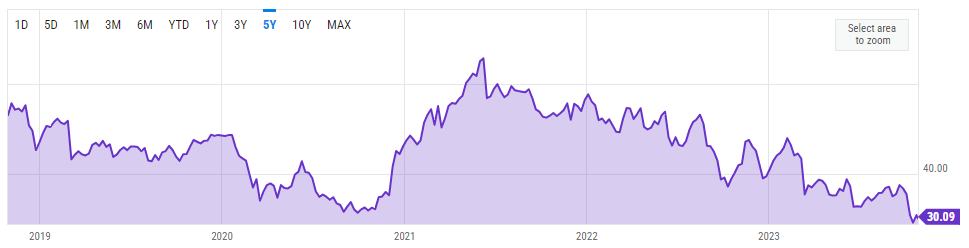

Two things here: 1) earnings are expected to fall 35% YoY in FY24 (April 2024); and 2) valuation on those lower earnings are still 20-30% below median historic levels. That’s a double whammy and a big reason why the share price has been cut in half since 2021.

But we’ve already established this is a historically stable business; so what if earnings recover in FY25-26?

Fortunately, we’ve been given a few tidbits to help bridge that gap: 1) higher rates are causing interest expense to jump by ~$20m annualized; and 2) a recent acquisition (from 2021) is falling from $23m EBITDA in FY23 to a loss in FY24 (which management believes is temporary).

These assumptions would need to be vetted further but assuming asset sales (outlined in #3 below) and a recovery to $10m EBITDA at the Hindawi business = ~$40m additional pre-tax income or $0.55/share after tax. Those 2 items alone would add 25% growth to the FY24 EPS guide.

At a 15x P/E (closer to 5yr median as opposed to 10yr median) = $42/share vs. today’s $30/share.

Again, still plenty to unpack but that’s a starting point. It also ignores any organic growth or capital allocation.

3) Asset sales to the rescue?

There is $315m of “already impaired” book value sitting in discontinued operations as of the latest quarter.

And these businesses chipped in $84m of unprofitable sales in Q1. Interesting that earnings took a nosedive from $14m profit in 1Q22 to $3m loss in 1Q23.

Maybe it’s a lofty assumption given the market’s renewed focus on profitability and higher rates but I’m assuming they’ll get at least book value ($315m) for these combined businesses.

If all of those proceeds went to debt repayment, then interest expense would fall by >$25m or ~$0.35/share after tax. This doesn’t count transaction costs or taxes; I’m probably wrongly assuming they’re selling below tax basis and incurring losses.

Summing it up…

So we have a long-time underperforming stock, trading at a cheap multiple (relative to history), with a stable business, assets being sold, and a change in management.

It’s also interesting that private equity is interested in the space… competitors McGraw Hill and, more recently, Houghton Mifflin, were acquired by PE. Wiley is family controlled so it’s mostly just confirmation of potential value.

FY24 looks like it will be a tough year unless/until those businesses are sold. Absent that, FCF will likely cover the dividend (~$80m) and a bit extra… that means capital deployment will be constrained for a while. That said, FY24 also looks like a trough in earnings; and if that’s the case, then this could be an interesting one to follow…