Quick Value #212 - Consensus Cloud Solutions (CCSI)

Levered microcap software trading at 3.5x earnings; buying back debt and equity

Today we’re covering:

Former 2021 spin-off of a legacy software business (eFax)

Trades at 3.5x GAAP earnings with stable FCF (2024 will be higher than 2023)

Announced debt buyback program at prices below par but levered 3.5x (net)

Sign up for the full newsletter below. (Assuming you enjoy all-cap value ideas + special sits.) We’ve been providing consistent weekly idea generation for nearly 6 years with no plans of slowing down!

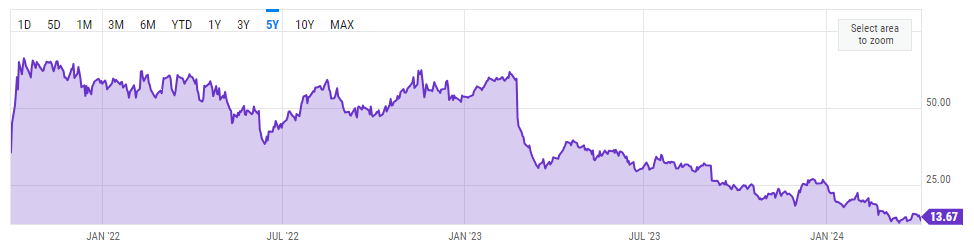

Market Performance

Quick Value

Consensus Cloud Solutions ($CCSI)

This company was formerly part of J2 Global which split into Ziff Davis (ZD) and Consensus Cloud in October 2021. The stock hung around $50-60 per share until Feb 2023 when they reported some accounting issues and weak guidance. It’s been downhill since then, but are things really that bad?

What they do…

Consensus Cloud Solutions is a software company with products focused on secure messaging. Products include: online faxing (eFax), electronic signature (jSign), and other digital workflow tools with gimmicky names like Unite, Clarity, and Harmony.

Customers generally fall into 2 buckets:

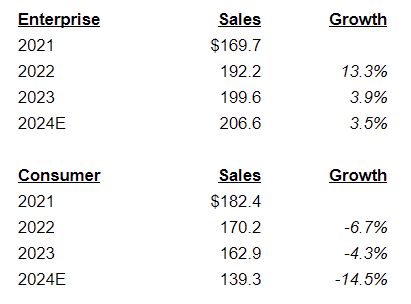

Corporate — Total of ~54k accounts across several industry verticals with healthcare organizations being the largest (~70%).

Consumer — Referred to as “SoHo” (small office / home office). At yearend 2023, there were 831k consumer users.

This is a good diagram highlighting the difference between these customer bases… consumer are self-serve and subscription-based at a low monthly ARPU near $15. The corporate business varies depending on the size of the customer but these are sales-driven with the typical account spending just under $4k per year.

Before you turn your nose at online faxing… it’s a small niche at $2bn+ annually with a stable customer base in regulatory-driven industries like healthcare, financial services, and legal. Monthly churn is less than 2% which is pretty good in software. The industry should see decent growth (at least on the corporate side) with increased volumes of data.

Here are high level KPIs for each customer segment:

Why it’s interesting…

1) Shares are beaten up since the spin-off (from $60 to $14) but is that warranted?

High level fundamentals look fine since the spin-off. Revenue, EBITDA, and FCF are each mostly flat from 2020-2024 based on guidance. At the same time, debt and share count are down. Not something you’d expect with shares down ~80%, right?

Beneath the surface, CCSI has a strong corporate business with total accounts growing from 46k to 54k over the past 8 quarters and churn consistently below 2%. The consumer side of the business (SoHo) is where problems are surfacing… customer attrition took them from 1m subs to 831k over the past 8 quarters and price increases are starting to unwind (lower ARPU).

Certainly looks like a “good” business / “bad” business situation here… although I’m not sure they can or should be separated; just noting that the consolidated picture doesn’t give you the full view of the business.

2024 guidance calls for more of the same — steady growth in corporate (2-5% growth) and accelerating declines in consumer (-16% to -13%). Revenue will be down 3-7% on a consolidated business but EBITDA/FCF up a little bit.

So why are shares down?

The declines in the consumer/SoHo business are accelerating and that’s extra concerning when you have a highly levered business. On the other hand, guidance looks pretty steady with another year of consistent earnings and FCF. But they’ll need to execute in their corporate business to keep things going.

One last comment here — We know that earnings have hung in there but the stock is down some ~80% which means valuation was taken to the woodshed. CCSI is one of the cheapest stocks in the Russell 3000 all-cap index. You’ll have to decide whether 3.5x leverage is too much and whether the core business will grow or decline from here.

2) Capital allocation will drive returns from here.

Management laid out the entire playbook on the last earnings call and that’s what has me intrigued. They’ve acknowledged there aren’t a lot of M&A opportunities at the moment, but they can influence the capital structure with debt/equity repurchases.

CCSI was spun with $805m debt under 2 sets of notes, $305m maturing in 2026 and $500m maturing in 2028. Those bonds are trading at 85-95c on the dollar, so they authorized a $300m debt buyback program. So far they’ve repurchased $62.6m in principal value.

Oh, and they have been ramping up stock buybacks too. They repurchased ~840k shares in 2023 for $23.7m ($28/share, yikes). There is a $100m authorization through Feb 2025 so we’ll have to see if they pick up the pace with shares in the low teens.

So what are shares worth?

There aren’t a lot of companies trading below 4x GAAP net income so it makes you wonder what’s going on here to cause the depressed price.

Since one segment is growing and the other is shrinking, it seems prudent to value those separately. I took a slight haircut to EBITDA margin assuming some added overhead if management were to sell or spin one of them. I used an 8.5x EBITDA multiple for GrowthCo and 3.5x for DeclineCo.

An 8.5x multiple is in-line with OTEX/GEN which are both “legacy” software businesses. The consumer division was a wild guess and I took the revenue down a bit more than guidance. A 3.5x multiple is where secularly challenged businesses like the Yellow Pages are trading.

Maybe the corporate division is worth more than 8.5x too. Regardless, this exercise came out to a meaningfully higher share price. Hmm…

Summing it up…

This situation reminds me a lot of Norton LifeLock (now Gen Digital) when they sold their corporate/enterprise business to Broadcom and became a pure-play consumer business.

CCSI might also have a very valuable corporate/enterprise business (perhaps worth more than the entire enterprise value of the combined company?).

Leverage is just enough to be scary… if the corporate business were to slow (or worse, decline), then the company would quickly be in a pinch. On the other hand, buybacks across the capital structure are a nice catalyst. With $80m annual FCF to deploy, they could retire 10% of shares outstanding ($26m) and $60m principal value of debt ($54m).

This one looks pretty cheap… maybe not a “hold forever” business but enough to recognize it probably shouldn’t be this depressed based on fundamentals. Are the debt/equity repurchases enough of a catalyst to get the stock moving? Hmm…

Thanks for sharing, I like the analysis and have spent time looking at this company. The underlying healthtech business is interesting. A lot of companies and people continue to say that hospitals use efax for a lot of things / underlying HIPAA rules on governmental healthcare efax seems to make that sticky. I wonder if EPIC, Cerner change that long-term but until I see some of that decline I can get behind it.

The consumer business for me is the problem. Docusign has a $10/month plan. Adobe has one. Micrsoft gives you the ability to print to pdf, but not track signatures if some people are still signing up for this business for the PDF options.

Also, I have seen a number of people get long LFMD and point to Worksimpli, which seems like a logical competitor. Personally, I think LFMD is not a good business either, but I don't understand how Worksimpli can be growing so quickly while JSign is churning. LFMD would tell you they are better at placing ads on Instagram, FB and TikTok. I don't see that as a logical answer. It's possible that Worksimpli is taking market share, but it seems like this is a race to the bottom for small business and individual customers to be able to sign PDFs for one month and then cancel and try another one. Is LFMD making up numbers or are they better at marketing? They definitely capitalize all their expenses, but I am only looking at topline. If CCSI just needs two or three digital marketing people, why don't they do that? If that isn't the answer, it seems that there isn't one and you should wait until that turns around.

I would hope there is a PE acquiror that will take this off their hands (at any price) and wouldn't get long until they do and then they can refinance the debt. Just my two cents.

Great results today! bought back 20% of debt over the last 6 months.