Quick Value 2.24.20

Berkshire Hathaway ($BRK) Redux

Market Performance

[Index | % change WoW ]

S&P 500 | 3338 -1.2%

Dow Jones | 28992 -1.4%

Russell 2000 | 1679 -0.5%

Russell Microcap | 619 +0.7%

10-Year | 1.47% -11bps

Gold | 1646 +3.8%

Oil | 53 +1.9%

VIX | 17 +21%

Market Stats

There has been quite a bit of commentary around the strength in top S&P performers so far this year (Microsoft, Apple, Amazon, Google, etc.). The average stock isn’t performing nearly as well as headline market returns indicate… It’s still early in the year but consider YTD and 1-year performance of the following:

S&P 500 — +3.3% / +20%

S&P 500 equal weight — +1.4% / +13%

Russell 2000 — +0.6% / +6.5%

Russell Microcap — -0.5% / +3.3%

Clearly some disconnect here…

Quick Value

Berkshire Hathaway ($BRK) — Shareholder Letter Review

Instead of posting a new idea this week, I thought I would share some notes from Warren Buffett’s 2019 annual letter.

As a quick recap:

Berkshire is a $560bn market cap at $230 per B share.

Yearend 2019 shareholder’s equity was $424bn so call it 1.3x price to book value

Call it $23.5bn in net earnings (see below) so ~23.8x PE.

There is about $103bn in gross debt on the balance sheet.

There is $248bn in market value of equity investments.

There is also $128bn in cash on the balance sheet or roughly 23% of the current market cap.

The Letter

Tidbits from this year’s letter were so-so… Here are some bullet points:

Buffett spent some time complaining about the new GAAP rule forcing companies to record changes in investment securities to flow through the income statement — causing large fluctuations in earnings from year-to-year:

Highlighted Retained Earnings with a story of Lawrence Smith and the discovery of retaining some amount of profits to reinvest back into the business each year… Creates the compounding effect. This felt like a message to investors: “Don’t expect us to pull a 180 and start sending back huge sums of cash to shareholders.”

Market value of the investment portfolio totaled $248bn at 12/31/19 — this excludes the Kraft Heinz equity method investment — Note that Apple alone is ~13% of the current market cap…

Some jabs at corporate boards and the egregious pay earned by some directors.

Share buyback commentary — Buffett noted: “In 2019, the Berkshire price/value equation was modestly favorable at times, and we spent $5 billion in repurchasing about 1% of the company.”

The Annual Report

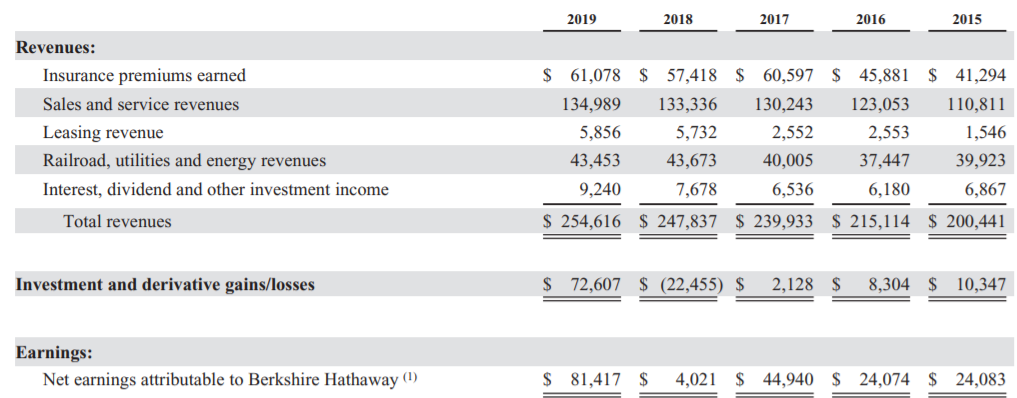

For starters, here’s the 5-year rundown of overall performance at the combined BRK businesses and the underlying earnings for the past 3 years:

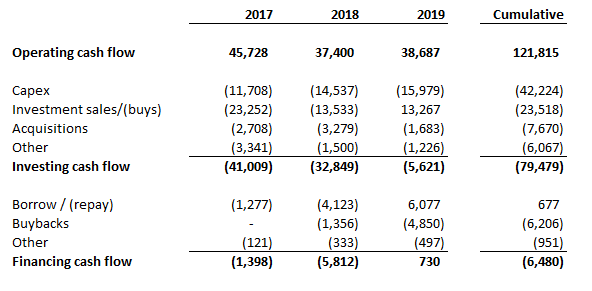

Instead of looking at the income statement, I’m a bigger fan of looking at cash flows and the sources & uses of cash over a longer-term period… Since 2017, Berkshire has:

Generated $122bn in operating cash flow… of that amount, they:

Invested $42bn in new capital assets,

Spent $8bn on acquisitions,

Repurchased $6bn in stock and

Socked away nearly $60bn for a rainy day!

We have $42bn dropped into capex and yet operating cash flow hasn’t budged in 3 years? Rising capital intensity? Buybacks and M&A still add to 10%+ of cash deployment but have they added anything substantial?

So, after capex, Berkshire has about $20-22bn to deploy each year (~3.75% of the current market cap) on top of the $128bn sitting on the balance sheet today.

Nothing new but this points to a company hoarding cash. Berkshire has been stockpiling cash while the stock itself has ridden the fluctuations in the investment portfolio and fundamental changes in operating businesses — cash has grown from $75bn in 2016 to $128bn today and pre-tax earnings in non-insurance businesses have grown from $19.3bn in 2016 to $22.2bn today.

The Two-Column Method

Back in his 2011 Annual Report (page 99 if you’re looking), Buffett outlined his Two-Column Method for valuing Berkshire. This involved taking the value of cash and investments on the balance sheet plus a capitalized value for non-insurance operating earnings. (With the caveat that the insurance businesses needed to operate at breakeven-or-better for this approach to be valid.)

Cash and Investments — Including the Kraft Heinz stake, I get $412bn in cash and investments at yearend 2019. Cash of $128bn, equity investments at $248bn, $19bn in fixed income securities, and $17bn in equity method stakes.

Non-insurance earnings — Pre-tax earnings in operating businesses were $22.2bn in 2019 (+2.6% from 2018) — Buffett has long mentioned a 10x pre-tax earnings multiple as a reasonable price to pay for a good business, so call it $222bn for the non-insurance operating businesses using that multiple.

In total that comes to $634bn or $258 per B share of stock. This would mean the stock (at $230) trades at a roughly 10% discount to intrinsic value. Not crazy cheap but not crazy expensive given the huge pile of cash and investments making up that valuation.

Final Thought

The existing portfolio of businesses continue to slowly grow but most of the value here is sitting on the balance sheet. Consider that a 10% move in $AAPL stock (up or down) would have the same impact to $BRK as 1/3 of their yearly operating earnings!