Quick Value #246 - Boeing Co (BA)

What's the turnaround potential at Boeing?

Today’s idea:

Raised $24bn equity to shore up balance sheet

Shares down >60% from pre-COVID high

Early innings of turnaround effort

Trades at 11x pre-COVID EPS

Quick Value

Boeing Co. (BA)

Boeing has a lot going on lately:

Safety issues with planes

Worker’s striking

Major layoffs

Raising equity

New management

What they do…

Boeing operates 3 segments:

Commercial Airplanes (BCA) — airplanes for commercial passenger and cargo use

Defense, Space & Security (BDS) — military aircraft like fighter jets and helicopters, surveillance systems like unmanned drones, missile systems, satellites, etc.

Global Services (BGS) — parts, service, distribution, supply chain services for commercial and defense customers

Below is a table of revenue by segment — 2 takeaways here: 1) non-airplane segments are a big portion of overall sales (40% pre-2019 and ~60% from 2020-2023); and 2) airplane revenue is still ~half of 2018 level.

Only the Global Services segment was profitable for the past 2 years:

Why it’s interesting…

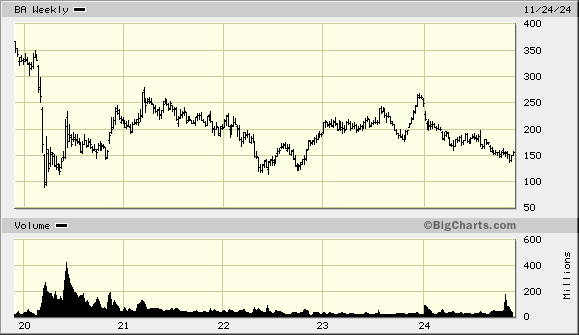

This is all about the turnaround potential. Shares are down >60% from pre-COVID highs (~$440/share down to ~$155). Is it even possible for them to recover? GE faced a similar backdrop not long ago, and they successfully managed through their challenges.

(Much of this is going to be “quick and dirty” math, there are too many factors to cover in a single Quick Value write-up.)

1) What is the earnings potential?

Again, we’re using scratch math to get a sense for potential upside.

Before the 737-MAX grounding in 2019, Boeing did $10.5bn net income on $101bn sales (10% net margin). As far as history goes, that’s the best margin performance they’ve had and quite a bit better than margins at rival Airbus.

If we give the airplane segment credit for a full recovery to $60bn revenue and use 2023 revenue for non-airplane segments ($44bn), then we get $104bn combined revenue in a “full recovery” phase. At 10% net margins = $10.4bn net income. On 748m pro-forma share count, that works out to ~$14/share net income or 11x P/E on the current $155 share price.

Note: I’m going for a ballpark figure here, it ignores several puts and takes — the added debt service compared to 2018 ($2.5bn interest vs. ~$500m); LT growth potential of commercial air travel & deliveries, margin improvement in defense segment, etc.

2) What will the future-state balance sheet look like?

A few critical factors are impacting the balance sheet right now:

Worker strikes and subsequent production ramp up (cash burn)

Production caps on 737-MAX leaving inventory piling up

Recent equity raise (~$24bn)

Boeing burned $10bn cash through 9 months of 2024 and expects another quarter of cash burn in Q4 while 2025 will be a “significant improvement.” Let’s call it $7bn of cash burn through 2025 before returning to cash breakeven in 2026.

Gross debt at Q3 was $58bn and assuming they kept 90% of the equity raise, that’s $32bn or so in cash. Fast forward to 12/31/25 and net debt is up to $38bn when including the $5bn preferred stock as debt. The equity raise adds ~130m shares to get a pro-forma share count of 748m ($116bn market cap).

3) What about the risks?

There are plenty of potential potholes here — nearly all of them well outlined in this WSJ article.

Being able to increase production to more than 50 MAXs and 10 Dreamliners a month would generate more than $10 billion a year, Wall Street analysts estimate, but this is proving increasingly elusive. On Wednesday, Chief Financial Officer Brian West told analysts that Boeing’s operations would burn cash in 2025.

With the equity raise complete, they’ve plugged a short-term cash hole. And they wrapped up the latest worker’s strike. That leaves the safety issues and production caps as the next major challenge — Boeing is currently limited to producing 38 MAXs each month.

On top of that, Boeing is laying off 17,000 employees (10% of workforce). Interestingly, that only gets them back to yearend 2022 headcount of 154,000.

Summing it up…

They’ve chipped away at a few of the major risks but handicapping the regulatory hurdles is a big unknown. Boeing probably has 2.5-3 years of cash runway to execute based on 2024-2025 cash burn. But is the current price cheap enough to justify the upside potential?

Hmm…

Been looking too. Ran too much now. Could see a some asset sales which could accelerate deleveraging . Fcf expectations have always seemed aggressive to me.

Well is it cheap enough in your view