Quick Value 3.27.23 ($TAP)

Molson Coors - major debt reduction = capital allocation inflection point

Opening this up as a free Quick Value this week. A few notes to open things up, I shared on Twitter that I’d be opening up my database of research notes. As I was transitioning files and folders into Notion I had this lofty goal of turning this into a paid product but it’s not good enough for that at the moment. Poke around and leave some feedback.

If you’re not a full subscriber, then hit subscribe below. It’s pretty cheap considering the plentiful idea generation :) here’s the newsletter cadence:

Weekly Quick Value idea generation

Monthly review of holdings / ongoing coverage

Monthly posts with a deeper look at value stocks

Market Performance

Market Stats

Home prices fell in February for the first time since 2012 (per WSJ)…

Quick Value

Molson Coors Beverage Co ($TAP)

I’ve had this stock on my list for years after the big merger. Fortunately I never did anything with it as they’ve essentially been running in place repaying debt. It seems they’re at the tail end of that deleveraging journey and a new capital allocation story may be at hand?

What they do…

Molson is a beer/beverage company which took its initial form in the 2005 merger between Molson and Coors. SABMiller and Molson Coors formed a JV in 2008 to combine production and distribution in the US. When Anheuser Busch acquired SABMiller in 2015 they had to sell the JV to Molson Coors for ~$12bn.

Today, TAP owns a large global portfolio of beer brands at various price points. They’ve been expanding into non-beer products like seltzers, ciders, spirits, etc.

Why it’s interesting…

1) Capital allocation shift

TAP spent years battling a 4.8x levered balance sheet. Net debt went from $11.5bn to ~$6.1bn from 2016-2022. As you’d imagine, it consumed 100% of capital deployment during that period.

Management is aiming for 2.5x leverage which, assuming no growth in EBITDA, would be $5bn vs. the current ~$6bn. Annual FCF is $1bn so we’re about a year away from revisiting the capital allocation playbook.

It’s interesting how coy management acts when pressed on deploying capital during earnings calls. They spout off a very rehearsed response about running it through their “models” and discussing with the board.

Operating cash flow hasn’t changed a whole heck of a lot and capex has varied slightly with a ramp in 2022 and another ramp to $700m expected in 2023. Guidance calls for $1bn +/- 10% in 2023 so roughly in-line with the past few years.

The dividend was cut during the pandemic and then reinstated in full last year. It runs ~$355m per year, good for a 3.3% yield.

That would leave about $600m available for other uses starting later this year or early next year. And we can already see a token buyback that began in Q4 2022, perhaps hinting at what’s to come. Returning 100% of the $1bn per year to shareholders equates to a 9% shareholder yield at current prices.

2) Valuation relative to stability

Debt is down, cash flow is stable, and price/cash flow is hanging around long-run averages. That seems like a fair amount of improvement.

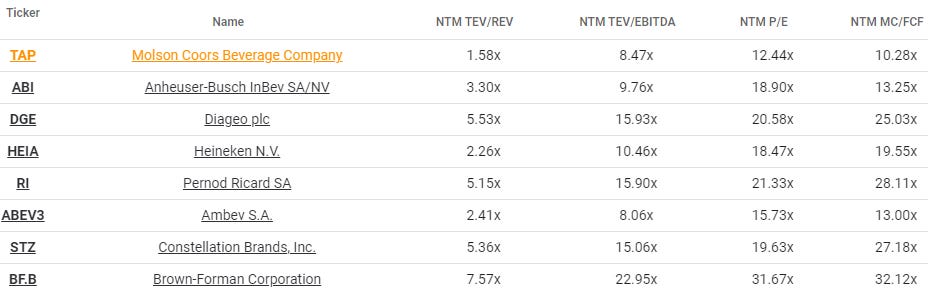

Shares are cheap compared to beer and spirits competitors. Slow growth and high leverage being large contributors to that discount gap.

What’s a fair multiple for this business based on peers? A 10x EBITDA multiple on $2bn annual EBITDA less the $5bn net leverage target = $15bn equity value or $69/share vs. today’s price around $50. That would be 15x FCF. This is a bit simplistic since the fundamentals are quite different from peers — growth, margins, etc. — but it highlights the potential value gap.

A return to growth would be a big help in closing that gap. COVID took a bite out of revenue and supply chain/inflation are still eating at margins into 2022-2023 but the business surpassed pre-pandemic 2019 revenue in 2022 and expects to growth low-single-digits in 2023. We’ll see if they can sustain that and start lifting margins too. Share count is also flat over 7 years which is a positive.

TAP is a great warning for “deleveraging” stories…

Paying down large amounts of debt doesn’t automatically accrue to equity holders and that’s exactly what happened here. Sure, revenue and EBITDA fell a tad from 2017 to 2022, but that $5-6bn debt reduction hast not (yet?) benefitted equity holders.