Quick Value 3.7.22 ($JNJ)

Another reminder to check out the new VDL website www.valuedatalibrary.com :)

Market Performance

Market Stats

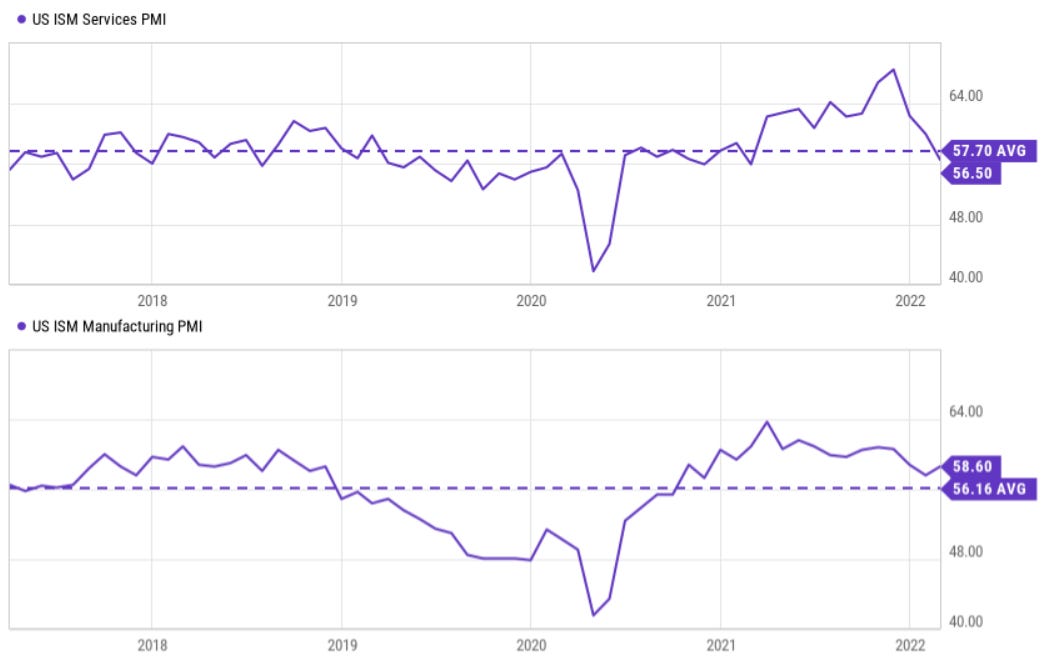

Labor force participation rate continues to climb but still way below pre-pandemic levels.

ISM Purchasing Managers Index levels remain in expansion territory. Services PMI missed expectations by a wide margin and has been contracting lately.

Quick Value

Johnson & Johnson ($JNJ)

I don’t often cover companies this big (JNJ is a $445bn market cap at $170 per share) but I’m a sucker for companies that a) have underperformed the market over long stretches of time; and b) are not falling knives.

JNJ is a respected healthcare company operating under 3 segments —

Consumer health (toiletries, cosmetics, etc.) — ~$14bn annual sales

Pharmaceuticals — $52bn annual sales

Medical devices — $93bn annual sales

In November 2021, JNJ announced they would spin off the consumer health business into a separate public company. The separation is anticipated to take 18-24 months so it could be late 2023 until this takes place.

The consumer business has been spotty in profitability but the real driving force for the separation could be the changing selling dynamics — prescription drugs / devices are typically more of a “B2B” salesforce-driven product; consumer products (more so following COVID) have an e-commerce and retail element to them. These are very different distribution channels.

From a financial standpoint, JNJ generates a lot of cash — >$23bn per year in operating cash flow…

Though they haven’t been able to grow per-share cash flow by much over the past 6 years — from $6.77/sh in 2017 to $8.90/sh in 2021 for a 5.6% CAGR. That includes $53.7bn spent on M&A and $34.6bn spent on share buybacks. The balance sheet also went from a hefty net cash position to a small net debt position during this time period.

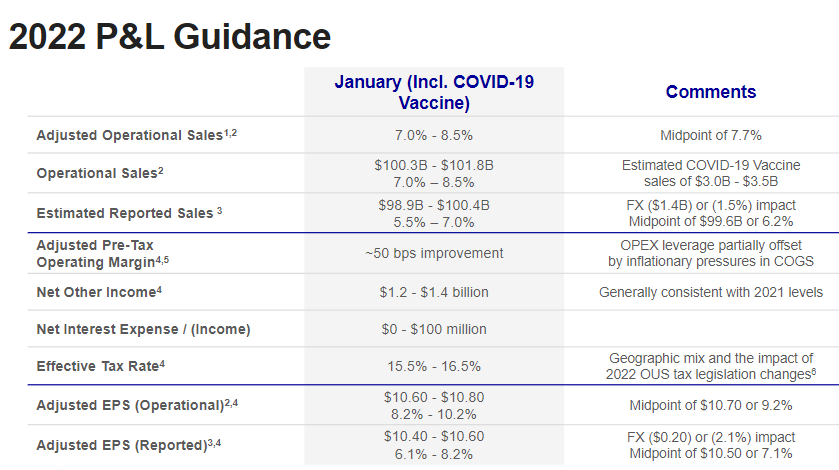

2022 guidance calls for $10.70 in EPS at the midpoint (up from $9.80 in 2021). This would be a ~7% annual growth rate from the $8.18/sh JNJ earned back in 2018 pre-COVID.

At $170/sh, JNJ trades just under 16x midpoint earnings of $10.70. Pretty close to the 5yr average multiple of 16.8x.

Maybe JNJ is looking at other healthcare megacaps like Abbott, Stryker, Medtronic, Eli Lilly, etc. garnering significantly higher multiples. Perhaps without the consumer health business they can make the argument that as a pure-play drugs/devices company they should trade more-line with that group (i.e. 20x earnings or more).