Quick Value 4.13.20

Axalta Coating Systems ($AXTA)

Market Performance

[Index | % change WoW ]

S&P 500 | 2790 +12%

Dow Jones | 23719 +13%

Russell 2000 | 1247 +19%

Russell Microcap | 448 +17%

10-Year | 0.73% +13bps

Gold | 1753 +6%

Oil | 23 -21%

VIX | 42 -11%

What a rally over the past week! My newsfeed was voicing constant frustration and confusion over this rally as it appears so obvious that more economic pain is set to come.

But you know what they say…

Market Stats

…Don’t fight the Fed!

With the stimulus package and massive Fed bond buying programs underway, money supply has rocketed higher (along with the markets). Perhaps no coincidence?

This “liquidity pumping” effort should go on for quite some time from here. Ever after the Federal Reserve balance sheet has jumped from $4.3tn in assets to $6.1tn over the past month.

With earnings season set to kick off this week, it will be fascinating to see the reaction to earnings / virus commentary from individual companies.

Most investors already know that results are going to be bad in 2020 (and Q2 in particular). How bad they could be still remains a question mark. We haven’t seen a big wave of dividend cuts despite climbing yields and there hasn’t been a flurry of bankruptcy filings (outside energy) which may indicate that most companies have had enough cash and borrowing capacity to get through this initial phase of the shutdowns.

Beyond the obviously bad 2020, is how this will all settle out over the next few years. As a country, we’ve “reloaded” our debt levels from the 2008-2009 period.

Paying down debt takes time, and austerity can be painful as we direct spending money toward debt payments. Does that mean money velocity could fall further (which would have a negative impact on inflation and GDP)? Also, how much more stimulus will be needed to land this economic jumbo jet?

It took about 5 years from 2009-2014 for the Fed’s balance sheet to reach ~$4.5tn in assets, where it stood for another 3 years until 2017… after that, 2 years were spent winding down assets to ~$3.8tn at which point the Fed reversed course and added to $4.3tn… then the coronavirus happened and we’re suddenly at $6.1tn..

This is going to take a long time to get back to “normal” (whatever that means)…

Quick Value

Axalta Coating Systems ($AXTA)

This was a hedge fund fan favorite the past few years after Meryl Witmer pitched the idea on the Barron’s roundtable in 2016. Since then, the stock has gone from $28 per share to just shy of $19 today.

Axalta is a chemical producer that was formerly part of DuPont. It was sold to private equity in 2012 and then came public in 2014. The company makes paints and coatings used on cars and trucks in both new production and collision/repair markets.

There are 235m shares x $19 stock price = $4.5bn market cap… Axalta carries $3.8bn in debt but also has $1bn in cash on hand for a $7.3bn enterprise value.

The past few years have been frustrating for Axalta shareholders as there have been numerous potential suitors offering to buy the company at a rumored $9.1bn price tag ($37 per share). Then, just 2 weeks ago, the company announced it was concluding a “strategic review” process without consummating a deal.

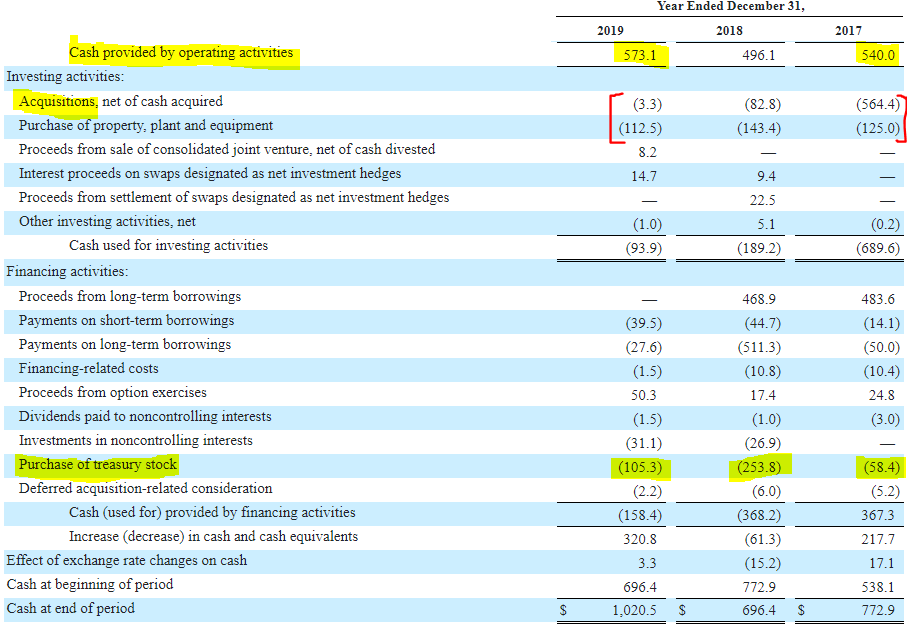

Axalta generates quite a bit of cash flow. More than $400m per year after capital expenditures. Most of this has gone toward a modest share buyback program, paying down debt, and a few acquisitions.

Guidance for 2020 (prior to the virus situation) called for more of the same… Relatively stagnant free cash flow at $450-490m (vs. $460m in FY19) and lower debt levels (which is good with $160m+ in annual interest).

It’s not all bad here…

Clearly there have been suitors for the company. A general rule of thumb in the chemical space has been EBITDA margins over 20% indicate a higher quality / specialty chemical business. This is right where Axalta sits today.

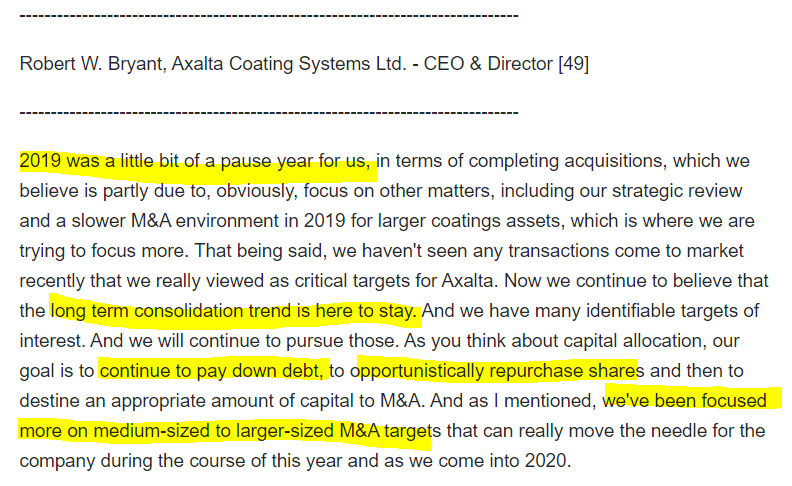

Axalta CEO has also commented that after getting debt levels in check over the past year, the company may look at larger acquisitions going forward…

Axalta last guided to $1.85-2.00 in EPS and $450-490m in free cash flow so you have a stock trading at about 10x earnings / cash flow with leverage at a reasonable level (3x net debt / EBITDA) and now turning its attention to more aggressive acquisitions.

Seems Axalta wants to play the role of consolidator here…

You think it's time for the strategic review process to formally restart (even though it really hasn't ended)?