Quick Value 4.6.20

Williams Sonoma ($WSM)

Market Performance

[Index | % change WoW ]

S&P 500 | 2489 -2%

Dow Jones | 21053 -2.7%

Russell 2000 | 1052 -7.1%

Russell Microcap | 382 -6.8%

10-Year | 0.6% -8bps

Gold | 1648 +1.4%

Oil | 29 +32%

VIX | 47 -29%

Smaller indices are close to retesting their weekly lows while the S&P 500 and Dow have moved a bit higher.

Oil rebounded considerably on hopes of Government purchases and OPEC concessions. VIX is well off highs that topped the 80s. Treasury rates are near lows but this is somewhat deceiving with rates on most corporate bonds moving higher.

Market Stats

Last week saw 6.6m initial jobless claims, nonfarm payrolls dropped 700k, unemployment hit 4.4%, and another $600bn added to the Fed balance sheet which now stands at $5.8tn…

Most stores and restaurants are closed throughout the country as we anxiously await the passing of the virus…

This reminds me of a presentation a few years ago by Howard Schultz, former Starbucks CEO, mentioning how the US is “over-retailed” — our country has 40% more retail space per capita then the next highest (Canada) and 5-6x more per capita then the “typical” country in the UK, Japan, and other parts of Europe.

E-commerce as a portion of retail sales has been growing quickly and as of Q4 2019 represented about 11-12% of the total.

Total retail sales in the US are roughly $6tn per year and includes everything from home furnishings to grocery stores to bars and restaurants.

If about 10% of that amount or $600bn is e-commerce driven, then we have roughly $5.4tn being impacted to some extent by coronavirus store closures.

At least $3.5tn of this is probably safe (or increasing) in the form of pharmacies, drug stores, grocery stores, warehouse club stores, gas stations, etc. It’s possible that remaining $1.9tn is down 50-100% right now due to closures.

Unfortunately, some of these businesses may not come back at all…

It’s a sad and dire thought, but is this the catalyst for the great reset of the US over-retailed environment?

Unclear how or where that spending would go… It could go back into higher savings rates to offset lower expected returns (i.e. low rates)? It could go into higher digital sales, or greater sales with the remaining retailers?

Time will tell…

Quick Value

Williams Sonoma ($WSM)

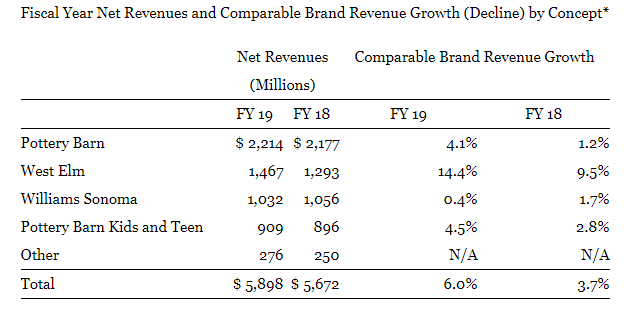

Williams Sonoma operates home furnishing stores under its namesake brand, Pottery Barn, and West Elm. Sales are generated through their 614 stores (45% of revenue) and online (55%). Shares are down from $75+ in February to $38 today. Not immune to the coronavirus impact as most stores are closed.

For starters there are 78m shares outstanding @ $38 makes it a $3bn company. There’s about $300m in debt and $400m in cash so we’ll call it a $2.9bn enterprise value.

Earnings were $4.84 per share in FY19 and free cash flow was $5.40 per share making this a reasonably cheap stock at 8x PE or 7x FCF.

Crate & Barrel is likely the best comparable company but alas it is not publicly traded. Restoration Hardware ($RH) is somewhat comparable (though sales per store are closer to $30m with WSM near $10m) and RH has significantly more debt.

Along with the 50% haircut in share price recently, a few things make it interesting today:

55% of sales come from e-commerce — That’s $3.2bn and grew 10% last year — it’s possible this amount could accelerate in 2020 at the expense of brick and mortar sales

All brands are performing well — Same store sales grew 6% in FY19 and 3.7% in FY18 with each brand growing

Williams Sonoma has possibly the best balance sheet in the industry with minimal debt, plenty of cash on hand, and solid cash flow coming from a high portion of online sales — They should benefit as others weaken during these store closures

B2B and International — Good growth opportunities as management hopes to achieve $2bn+ in sales from the $80bn B2B market (total WSM sales were $5.9bn in FY19) and International is a small and growing division

Shareholder friendly management — The dividend at $1.92 per share is good for a 5% dividend yield and another $200m per year or so is spent on buybacks, good for another 6.5% of the current market cap

Smaller competitors Pier 1, At Home Group ($HOME), and Kirkland’s ($KIRK) are all struggling with debt and may face bankruptcy — a potential positive for Williams Sonoma if those companies’ combined $3bn+ in annual revenue is up for grabs

This business will certainly see some negative impact from store closures and changing consumer behavior. But, they appear better positioned with their strong balance sheet and large online mix.