Quick Value 5.3.21 ($ATH)

Athene merging with Apollo Global to form an insurance / investment powerhouse

Market Performance

Market Stats

There has been much talk about rising inflation in the US lately…

Warren Buffett delivered a clear verdict Saturday on the state of the U.S. economy as it emerges from the pandemic: red hot.

“It’s almost a buying frenzy,” the Berkshire Hathaway Inc. chief executive officer said during the conglomerate’s annual meeting, which was held virtually from Los Angeles. “People have money in their pocket and they’re paying higher prices,” he said.

Buffett attributed the faster-than-expected recovery to swift and decisive rescue measures by the Federal Reserve and U.S. government, which helped kick 85% of the economy into “super high gear,” he said. But as growth roars back and interest rates remain low, many -- including Berkshire -- are raising prices and there is more inflation “than people would have anticipated six months ago,” he said.1

Price indices are on the rise…

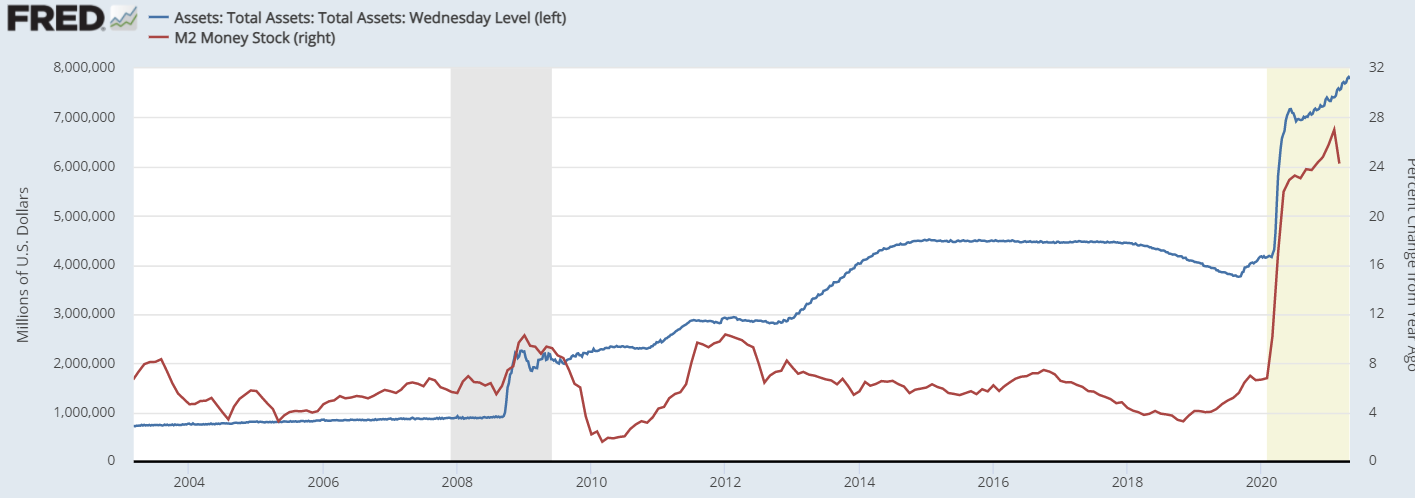

And the Fed continues their asset purchases leaving money supply growing at a 20%+ annual rate…

Quick Value

Athene Holding Ltd ($ATH)

Athene sells annuities, life insurance, and retirement services and is currently working through a merger with its largest shareholder, PE-firm Apollo Global ($APO).

Operating performance has been great since the company was founded in 2009 and came public in a 2016 IPO but the stock price hasn’t reflected this… Book value has grown 16% per year from 2008-2020 and earnings have doubled from $4 to $8 per share since 2016.

Apollo is an alternative asset manager mainly focused on credit investments. Their relationship with Athene is such that they manage the investment portfolio on behalf of Athene (for fees). The combination will bring investment management in-house and create a company with a large stream of fee earnings for investment services and annuity sales.

The merged company should have ~578m shares outstanding and a $55-60 share price = $33bn market cap. Combined EBIT is around $2bn and Apollo earnings jump from $2 per share to $3.40 per share for a 16x earnings multiple.

Life insurance peers like MetLife and Prudential trade at 7-9x earnings while alternative investment companies (i.e. PE firms) trade at 17-20x earnings. So the newly combined Apollo/Athene will sit in a strange place from a comparable standpoint.

In tandem with the merger, Apollo/Athene will be adopting a simpler C-Corp structure (like most public companies) instead of the messy passthrough structure today. Other PE-firms have adopted this approach which widens the potential investor base and allows for index inclusion. For reference, KKR is a $33bn market cap with $350bn in AUM compared to Apollo with $450bn in AUM and a pro-forma $33bn market cap (though credit AUM is typically viewed as less valuable).

They are creating a unique business model focused on credit management for insurers while other PE-firms are seeking ever larger funds for buyouts.

https://www.bloomberg.com/news/articles/2021-05-02/warren-buffett-sees-a-red-hot-economy-with-creeping-inflation