Quick Value 7.11.22 ($EHAB)

Home health spinoff Enhabit trading at ~11x earnings

Market Stats

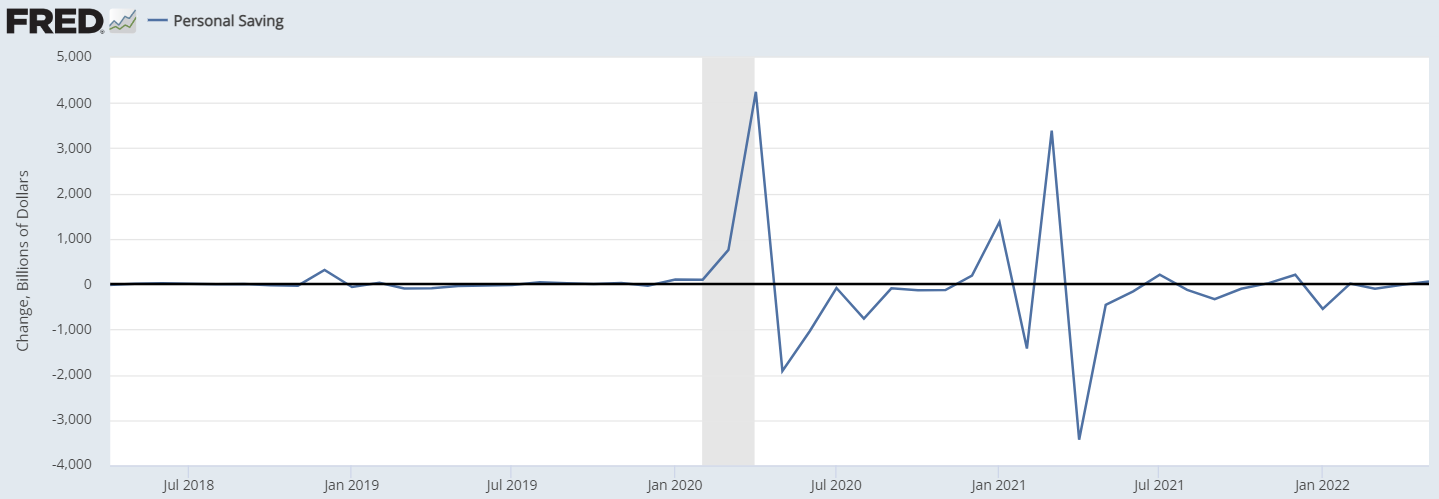

Personal savings have been cautioned as warning of a slowdown in spending… the savings rate (now below 6%) is below long-run averages

…but wages are still growing at a double digit rate; so incomes are still increasing

The change in savings (absolute dollars), isn’t fluctuating that much; it’s just with incomes on the rise, the proportion of savings has fallen (with the remainder being consumer spending)

Quick Value

Enhabit Inc ($EHAB)

Enhabit was a very recent spinoff from Encompass Health ($EHC). Encompass retained their inpatient rehab facilities while Enhabit became a home health and hospice service provider.

Home health is an asset-light business — sending healthcare workers to care for patients in their homes instead of expensive-to-build-and-maintain medical facilities. The downside to that asset light nature is the low barrier to entry. There are 11k home health agencies and 5k+ hospice providers as of 2020… the 4 largest players account for ~22% of Medicare spend and 92% of providers generate <$5m in revenue — i.e. it’s a massively fragmented industry.

This is an acquisition-led growth story — locations have expanded from 160 in 2014 to 351 in 1Q22 with several step-change jumps along the way. Thanks in large part to ~$760m in acquisitions from 2015-2022.

Nearly all revenue is derived from Medicare/Medicaid with short payment periods. There will always be some level of risk with revenue given the Medicare concentration — if reimbursement rates were to reset lower, this would have a huge negative impact on EHAB.

Since there aren’t many assets in the business, the balance sheet is mostly A/R and accrued payroll with a hefty goodwill balance from all the acquisitions. The balance sheet looks to be in reasonable shape with $570m or so in net debt for 3-3.5x leverage depending on where 2022 EBITDA shakes out.

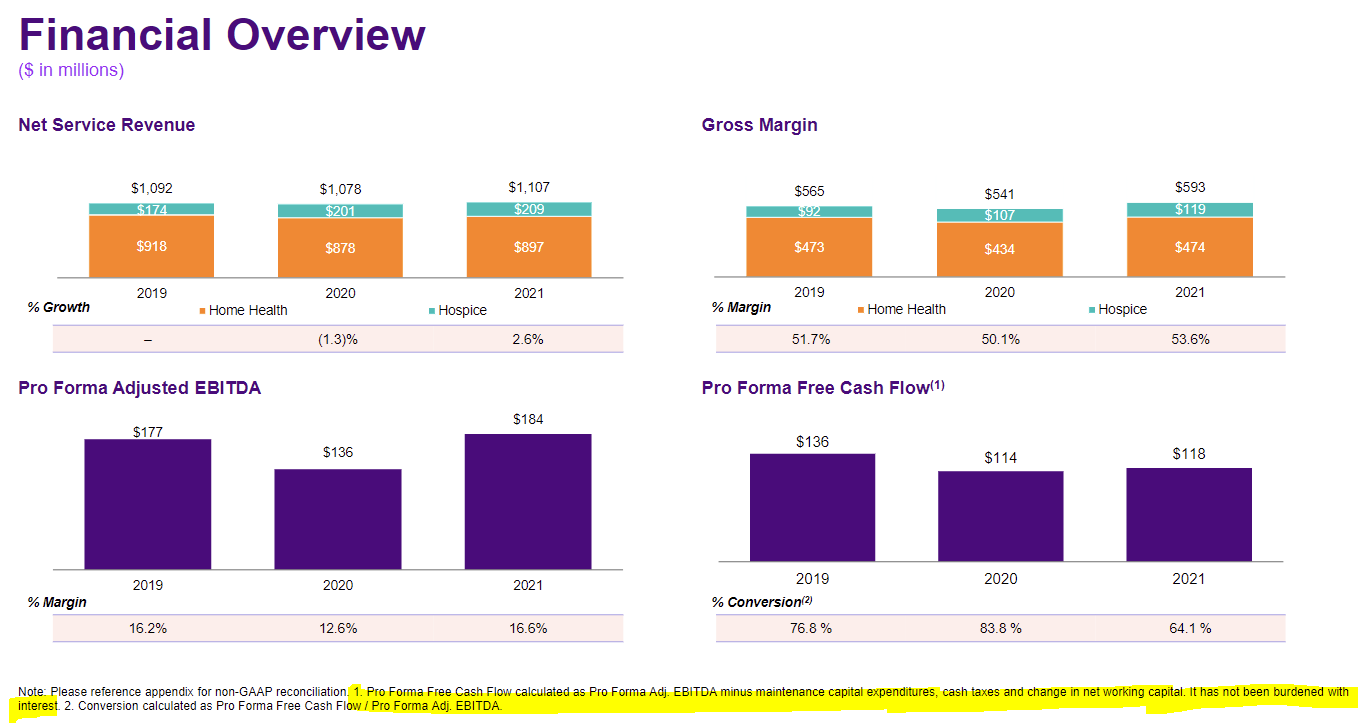

The Financial Overview from the investor day presentation is helpful but also a bit misleading in highlighting free cash flow; it doesn’t include anticipated interest expense and uses Adj. EBITDA instead of operating cash flow as the starting point.

Guidance for the inaugural public year looks reasonable. Revenue is expected to be approximately flat YoY which may be conservative based on Q1 results. EBITDA is stepping down from $184m in 2021 to $165-185m from rising costs and added public company costs. At the current share price, EHAB is trading at 8.3-9.3x EBITDA.

A simple bridge from guidance using midpoints — $175m EBITDA less $19m interest less $30m working capital build, less $7.5m capex, less $22.5m cash taxes = $96m free cash flow or $1.92 per share. With the share price currently <$20, that’s a 10x P/FCF multiple.

And what does EHAB anticipate doing with that cash flow?

Invest for growth! Both organic (new location openings) and inorganic (acquisitions) are on the table here.

This approach is consistent with several competitors: VITAS (part of Chemed Corp $CHE), LHC Group ($LHCG), and Amedisys ($AMED). Competitors have been spending heavily on acquisitions.

The 3 competitors mentioned above trade at much higher multiples of earnings and EBITDA — all of them >20x earnings vs. EHAB at ~10x and all of them >15x EBITDA vs. EHAB at <9x. EHAB is smaller and less capitalized; and other than management quality/competency, is subject to the same industry ricks.

Check out the Form 10 filing for (much) more detail on Enhabit.

Big insider buying in this one. Given the Medicare cut and the valuation disparity vs its peers it might be worth having ehab as one of the legs of a pair trade