Quick Value 7.20.20 (ISBC)

Market Performance

[Index | % change WoW ]

S&P 500 | 3225 +1%

Dow Jones | 26672 +2%

Russell 2000 | 1473 +4%

Russell Microcap | 555 +4%

10-Year | 0.63% -2bps

Gold | 1812 unch

Oil | 41 unch

VIX | 26 -4%

Market Stats

Banks

The big banks have all reported earnings and, as promised, there were significant increases in loan loss provisions — more pain ahead in small business and consumer finances.

Retail Sales

Pretty amazing that total retail sales grew 1.1% in June compared to last year… Retail sales declined as much as 20% YoY as recently as April!

Looking back at the progression of retail sales during the financial crisis… Sales started declining YoY in September 2008 and didn’t get back to positive until November 2009 — over a full year later.

So far in 2020, we’ve seen a YoY decline in March-May with June starting to recover compare to last year…

Maybe the stimulus is finally showing up in spending?

Unemployment

Continuing jobless claims have leveled off and have been declining for the past 6 weeks…

Money

A continued reminder that money supply is still growing >20% compared to last year… It’s going to be difficult to kill the bull move in stocks until this starts to reverse course…

Quick Value

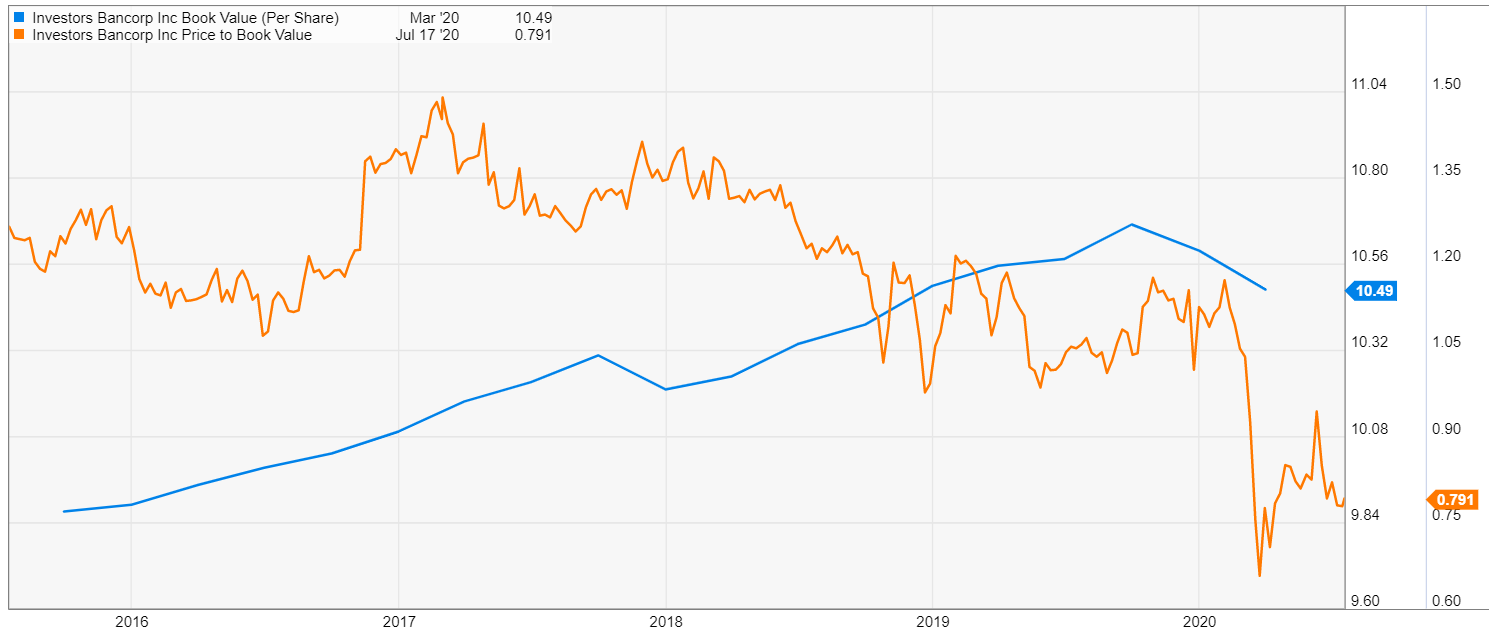

Investors Bancorp (ISBC)

With all the big banks reporting earnings, why not take a look at a financial!

This is a small cap regional bank operating out of Short Hills, NJ — they first came public in 2005 as a “mutual conversion” where the bank is owned by depositors. Then, they completed a second-step conversion in 2014 to convert the remaining ownership from depositors into the public markets. This process raised $2.15bn in fresh capital and left the bank very well capitalized.

Since 2014, ISBC used that cash to:

Repurchase stock — “Since commencing our first share repurchase program in March 2015, we have repurchased 127.1 million shares totaling $1.54 billion at an average price per share of $12.11.”

Initiate a dividend — “Beginning in September of 2012, we began to pay a quarterly cash dividend of $0.02 per share. For the year ended December 31, 2019, our dividend payout ratio per share was approximately 59%. We have recently increased our quarterly dividend to $0.12 per share.”

Loan growth — Total loans grew from $13bn to $21bn — a 10% CAGR over a 6-year period

Shares have fallen and Investors Bank now trades at a hefty discount to book value (as most banks have)…

The current $8.20 share price is a ~22% discount to the $10.50 per share book value at 1Q20.

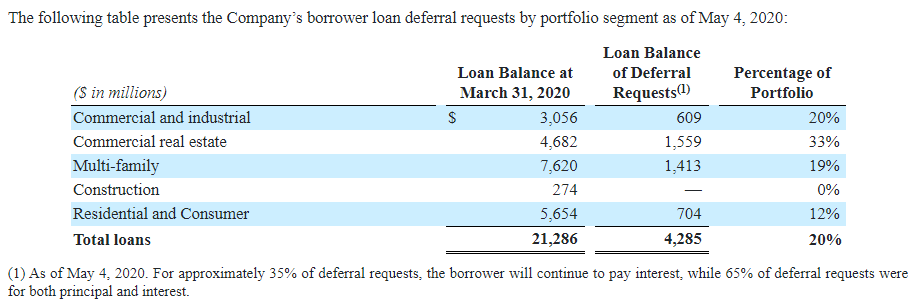

There is a heavy amount of commercial real estate and multi-family loans in the portfolio — a partial explanation for why the stock trades where it does. Borrowers have already requested payment deferrals on 20% of ISBC’s loan portfolio.

Here is the other part of the “explanation” — pre-tax earnings have not grown in years and now look like they’re set to decline given interest rates and COVID…

Since the capital infusion, ISBC has fired the proverbial bullet — spending their massive equity cushion from 16% down to 11% CET1 (which is still quite high compared to other financial institutions)… All without meaningfully impacting ROEs!

Well that doesn’t paint a pretty picture…

But!

Thanks to efficient markets, we’ve seen the multiple of earnings and book value compress to reflect the weak fundamentals and now COVID…

Today, we have a $8.20 stock with 250m shares outstanding = $2bn market cap.

Trailing net income is about $190m / $0.76 per share = 10-11x PE

Book value is $2.6bn / $10.50 per share = 0.78x PB

Despite spending most of the excess cash from the mutual conversion, Investors Bank remains well capitalized with $2.6bn in equity on $26bn in total assets.

Commercial real estate in the Northeast US will obviously be the most impacted portion of the portfolio at 22% of total loans — as seen by the number of deferral requests.

A big chunk (62%) of the loan portfolio is in consumer mortgages and multi-family loans — a potentially less risky area.

The dividend has been a bigger focus in recent years and now nears a 6% yield. While M&A has rounded out capital allocation with a few small acquisitions over the years.

Valuation is mostly in-line with other smaller banks near 10x earnings and a 20-25% discount to book value. What could make this bank more interesting than others are its better positioned loan portfolio, excellent balance sheet, and potential for M&A as either a buyer or a seller…