Quick Value 7.21.22 ($HLN)

Haleon - consumer health/OTC spinoff from GSK

Market Stats

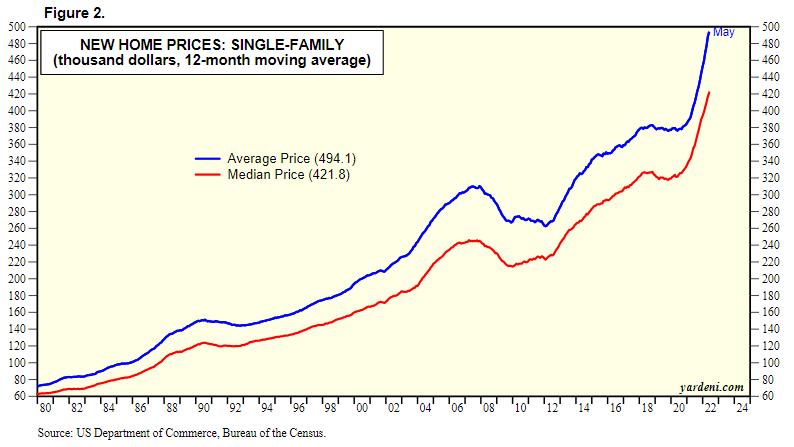

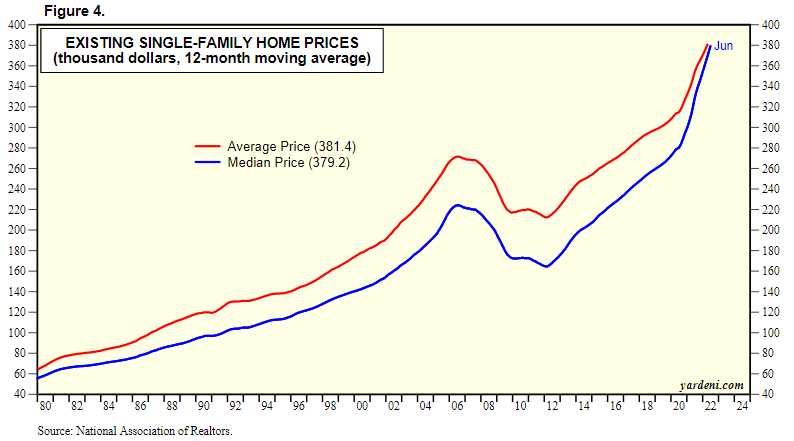

Housing has gotten a lot less affordable lately… close to pre-GFC era levels…

Home prices have skyrocketed (both new and existing homes)… this isn’t exactly new news but putting the charts in perspective can be helpful

Quick Value

Haleon Inc ($HLN)

Another spin-off this week, or demerger as they call them overseas. GSK (formerly GlaxoSmithKline) recently completed this spin-off of its over-the-counter products business. Haleon sells non-prescription products like multivitamins (centrum), digestive relief (tums), toothpaste (sensodyne), and pain relievers (advil).

There aren’t a ton of great comparable companies for this business unless you count the likes of P&G or Kimberly Clark but those product portfolios are quite different. Most of the large OTC drug businesses are tucked inside of major pharma companies. Haleon itself was formed by a GSK/Novartis JV and then a JV with Pfizer.

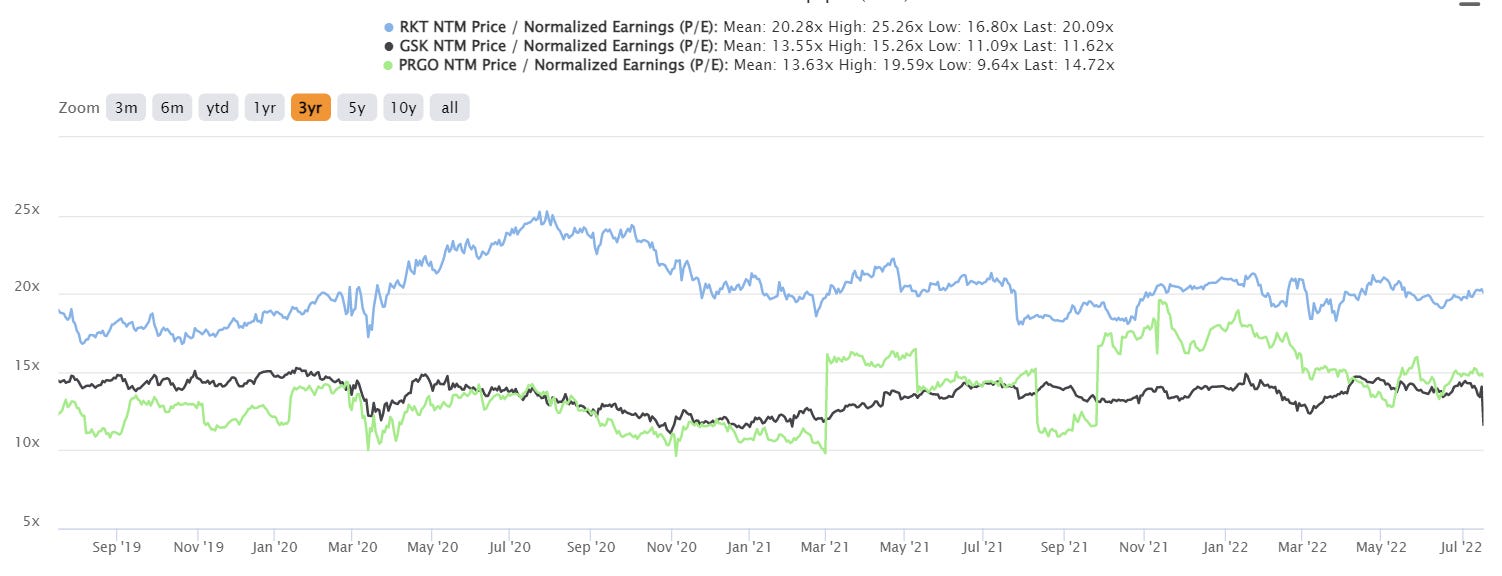

A market is quickly forming for OTC/consumer health businesses though… Perrigo ($PRGO) has completely reshaped its business away from generic drugs to OTC products. Johnson & Johnson ($JNJ) intends to spin off their consumer health/OTC business. And Reckitt Bensicker already has a collection of competing products.

Haleon has major brands with good market positions and plenty of household recognition. It’s a heavy M&A industry with brands changing hands. Products reach maturity and growth slows/declines

At the outset, Haleon will have close to 11bn in total debt for leverage of >4x EBITDA. Management is targeting a 30-50% dividend payout ratio so that will probably limit capital allocation uses strictly for paying down debt to their stated goal of 3x or less.

The spin off is a pretty clever move for GSK given the stock has traded at a pretty low multiple of earnings historically (at least compared to CPG businesses). With P&G, Reckitt, Kimberly Clark, and now even Perrigo trading at 20x+ earnings and 15x EBITDA; Haleon stands a good chance of garnering a high multiple compared to pure pharmaceuticals.

Initial trading shows Haleon at 300 pence or a ~28bn GBP market cap. That would be 20x free cash flow and 15x EBITDA so right near competitors.

These consumer health businesses are likely to be treated as high quality companies with minimal earnings volatility and stable price increases. As the market for these stocks continues to develop, it will be interesting to see if they trend closer to the P&G/KMBs. Note that JNJ trades around 17x earnings / 13x EBITDA and is likely pursuing the consumer health/OTC spinoff for similar reasons to GSK.

Some additional resources on Haleon: