Quick Value 7.25.22 ($TH)

Target Hospitality - lodging services at 5.5x EBITDA with major contract win

Market Stats

Business activity slowing rapidly… PMI indices moving into contracting territory.

S&P 500 has trended back toward its long term average P/E ratio but is still highly dependent on the denominator remaining in tact for the rest of 2022-2023. Current estimates call for ~10% EPS growth in 2022 and ~8% growth in 2023.

Quick Value

Target Hospitality ($TH)

A friend suggested I take a look at this stock and since I’ve closely followed other lodging service providers Civeo ($CVEO) and Dexterra ($DXT.TO), I thought I’d use the opportunity for this week’s Quick Value…

For starters, TH operates in the “accommodations” industry, which can have a variety of meanings. Some companies own and operate permanent lodging facilities (think nicer motel) in remote areas serving oil & gas or mining producers. Others have mobile units that can be picked up and moved to where demand is. (The annual report contains good background information on the industry.)

These businesses get paid a daily rate for lodging and services (much like a hotel) and have minimal capex once the facilities (or mobile units) are built. Thus, they tend to generate good cash flow.

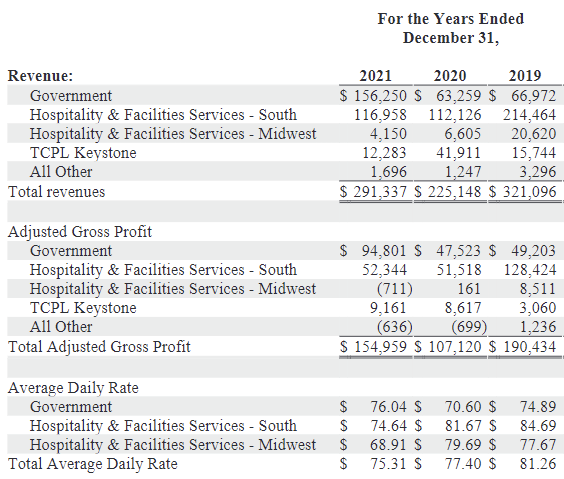

I’d normally be skeptical of a stock going from $10 to $1 and back to $13 but TH recently announced a major contract win that will likely be a game changer for the business. With this change, TH will be a mostly Government services business (73% of pro forma revenue) with the remainder coming from oil/mining customers.

At $12.50/share, TH has a ~$1.3bn market cap and about $350m in net debt for a $1.65bn enterprise value. Here is the revised outlook incorporating the contract:

Based on 2022 guidance, TH is trading at 5.5x EBITDA with oil and gas focused peers trading around 6x and mobile-focused players ($MGRC and $WSC) trading at 9-12x EBITDA. (The peer group outlined in TH investor deck doesn’t seem like a representative sample to me.)

So TH is now mostly a lessor and accommodations service provider to the US Government with a big emphasis on immigration housing and support.

TH came public via SPAC in early 2019. Prior to that, most of the company’s cash flow went to organic investment via capex and several acquisitions. Since then, they’ve been paying down some acquisition debt. With the added EBITDA coming in 2022-2023, there will probably be a lot more flexibility in using cash. Management has talked about acquisitions being a part of that plan.

The question here is whether TH deserves a higher multiple with the shift away from the oil industry. Regardless of industry served, these businesses are operating large and fixed facilities under contracts for a specific purpose (something quite different than a traditional hotel or office building).

The longevity of immigration/humanitarian efforts certainly seems more valuable than oil and gas production (thinking 10 years out here). But the risk of a major contract loss is always a possibility which makes valuation harder!

Any thoughts on the THwww exchange offer?