Quick Value 8.1.22 ($XPO)

XPO trading at 7x EBITDA splitting into LTL and freight brokerage businesses

Market Performance

Market Stats

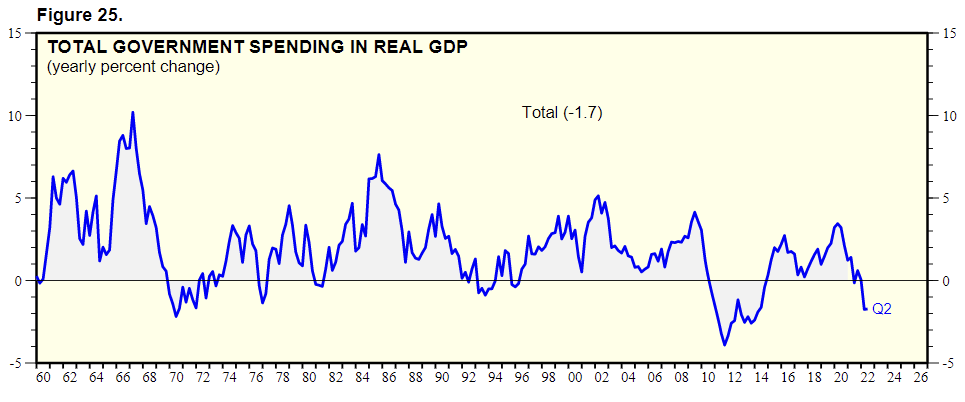

GDP decreased at a 0.9% annual rate in Q2… within that, consumer spending increased 1%, private (business) spending decreased 13.5%, Government spending decreased 1.9%

Government spending has been declining for 3 consecutive quarters

Quick Value

XPO Logistics ($XPO)

Continuing with the spin-off theme…

XPO was a massive logistics roll-up from Brad Jacobs (of United Rentals and Waste Management fame). After the company hit the $17bn+ revenue mark, Jacobs started unwinding various pieces of the business. First he spun off GXO Logistics, the contract warehousing division, in August 2021. Then sold their North American intermodal business and put their European business up for sale. Finally, in March 2022, XPO announced they would split up the LTL and freight brokerage business units.

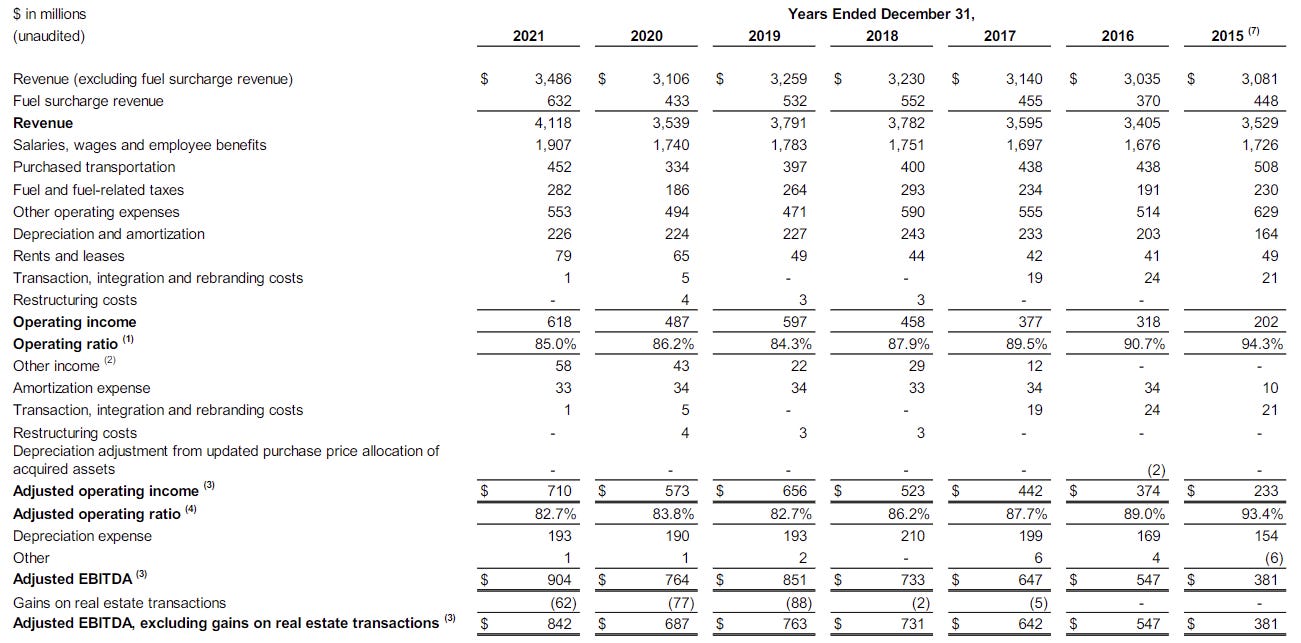

For starters, XPO has 115m shares outstanding and a ~$60 share price = $6.9bn market cap. Net debt is ~$2.6bn as of 1Q22 for a $9.5bn enterprise value. Current guidance calls for 2022 EPS of $5.40 (11x PE) and EBITDA of $1.37bn (6.9x EV/EBITDA).

A breakdown of financial performance by segment:

Freight brokerage is a business that doesn’t require a lot of assets. Just technology and hardworking people. Competitors CH Robinson ($CHRW) and Expeditors International ($EXPD) are big players with 10-12x EBITDA multiples.

It’s a growing industry as the use of brokers becomes more common. They generally clip small margins on the transportation they help to coordinate.

Few assets means they have minimal capex needs and turn a high portion of EBITDA into free cash flow. Hence the higher EBITDA multiples.

The brokerage segment will be the SpinCo but unfortunately XPO hasn’t filed a Form 10 yet with detailed carve out information (maybe should have waited on writing on this one!). Historic financial information is only so helpful as the brokerage and other services line includes European and intermodal businesses along with freight brokerage.

Presentation documents tell us this business was at $4.8bn revenue and $305m EBITDA for 2021.

Less than truckload (LTL) transportation is an interesting market with some unionized players (Yellow and Arc Best) and non-unionized players like Old Dominion and Saia. The union players trade at a substantial discount — less than 4x EBITDA — while Saia and Old Dominion trade at 10-16x EBITDA.

XPO likes to tout the improvement in their LTL business since they acquired it back in 2015 — EBITDA improved from $381m to an estimated $1bn in 2022.

Other divestitures may take a big bite out of the remaining debt at XPO. The intermodal business ($1.2bn revenue) was already sold for $710m (0.6x sales) as of 1Q22 and is reflected in net debt. The European business ($3.1bn revenue) has yet to be sold. A similar multiple could bring in ~$1.9bn or so in proceeds.

With XPO trading at less than 7x EBITDA and pure-play competitors at 10x or more, the break up may make sense…