Quick Value 8.2.21 ($NWL)

Newell Brands -- Consumer brands in turnaround mode trading at ~14x earnings

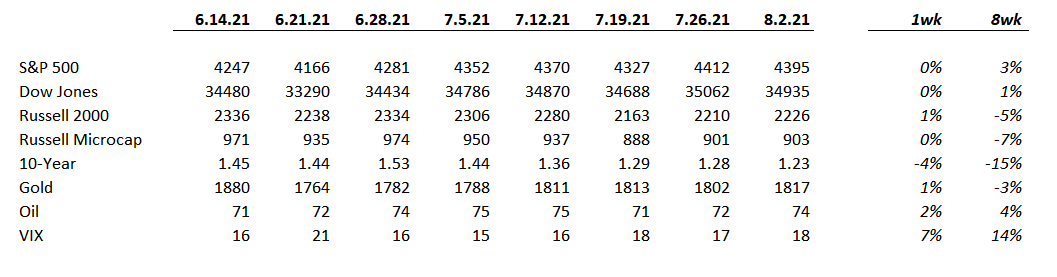

Market Performance

Market Stats

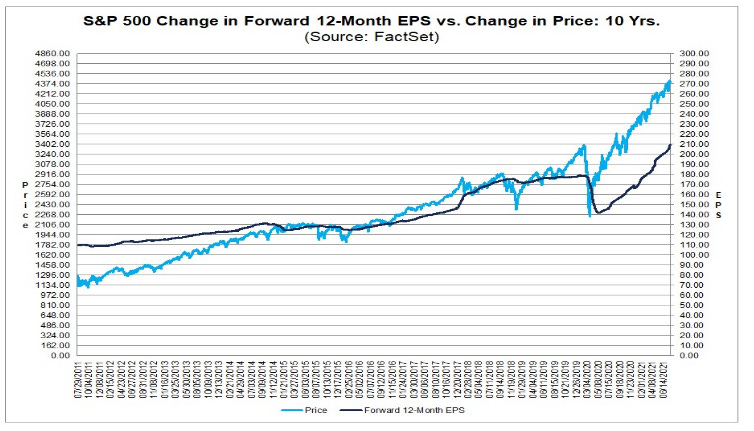

Q2 Earnings — Most companies are crushing earnings estimates… By a near-record 17%!

Stock prices follow earnings… and so far, earnings are way up… And a look at the overall earnings picture for S&P 500 companies.

GDP grew at a 6.5% annual rate in Q2… I think it’s fun to dig into the various components of GDP and see what’s working and what isn’t… household consumption is surging as are nondurable goods like clothes, and gas…

Quick Value

Newell Brands ($NWL)

Newell is a holding company of various consumer and commercial brands… Most are pretty well known like Ball jars, Graco strollers, Yankee Candle, Coleman outdoor products, etc.

To simplify the story… This company was once known as Jarden (a past spin from Ball Corp) and a guy named Martin Franklin built the business up through tons of acquisitions. They were acquired by Newell Rubbermaid in 2016 for $15bn and became Newell Brands. The combined business got ahead itself with too much leverage and declining fundamentals. They went through some restructuring and are still working their way out of a hole.

New CEO Ravi Saligram came into the picture less than 2 years ago. There was a recent WSJ article covering his famed “no asshole” policy announced to employees.

Here are some bullet points on Newell and why it hit my radar to dig deeper:

A quick snapshot of how 2Q21 results went…

After the disastrous combo of Newell / Jarden, the company has focused on getting the balance sheet in order — debt is down from near $12bn in 2016 to $5.5bn in 2Q21 (3.1x leverage) — I love when companies are relentlessly focused on cutting debt

Market cap is $10.5bn at $25 per share — based on 2021 estimates, this works out to 14.4x PE and 10.6x EV/EBITDA — not expensive for a consumer brand company

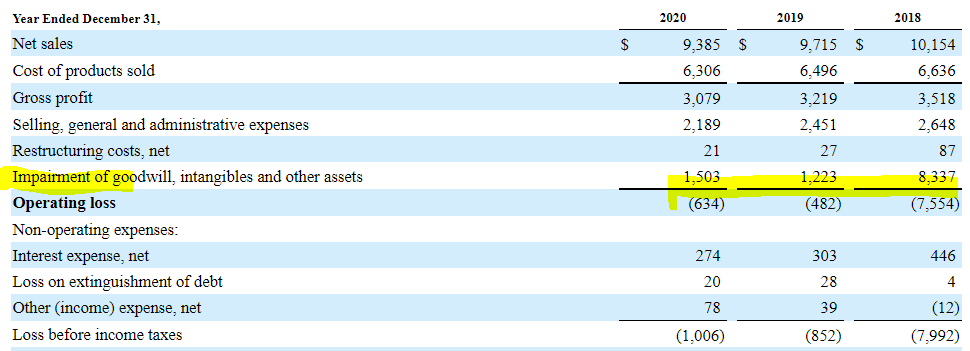

Impairment charges have mostly worked through the system — $11bn from 2018-2020 with zero charges taken through the first half of 2021

Headwinds from inflation pressures and supply chain challenges totaling ~$0.5bn this year! That’s a huge number on $10bn in sales…

Full year 2021 guidance looks good on an absolute basis but implies a tough stretch in the 2nd half of the year

Competitor Spectrum Brands ($SPB) trades at ~14x earnings with slightly higher leverage at 3.4x — pretty much in-line with Newell — while others like Proctor & Gamble and Kimberly Clark trade >18x earnings (though there are some major differences in discretionary vs. staples aspects to those businesses)

New CEO seems focused on getting back to revenue growth — sales set to grow 7-10% in 2021 and when comparing first half results vs. 2019 (2yr stack), sales were still up double-digits…

At a quick glance, Newell looks reasonably priced against Spectrum Brands ($SPB) though I haven’t compared the quality and durability of their brands —both trading in the 14x earnings range.

There still seems to be some work to do on leverage — >3x can be considered high depending on the stability of your cash flows.

Lastly, COVID had a strange effect on this business where it torched results in early 2020 and then provided a huge boost to profits in late 2020. Now they are lapping those strong results with the added problem of inflation/supply chain headwinds. I’m sure investors want to get some clarity around what 2022 looks like before getting excited — but at the same time, the chart shows huge underperformance vs. S&P 500 against nearly every time period… expectations are low for a comeback!