Quick Value 8.3.20 (EME)

Emcor Group (EME)

Market Performance

[Index | % change WoW ]

S&P 500 | 3271 +2%

Dow Jones | 26428 unch

Russell 2000 | 1480 +1%

Russell Microcap | 554 unch

10-Year | 0.54% -5bps

Gold | 1986 +5%

Oil | 40 -2%

VIX | 24 -8%

Market Stats

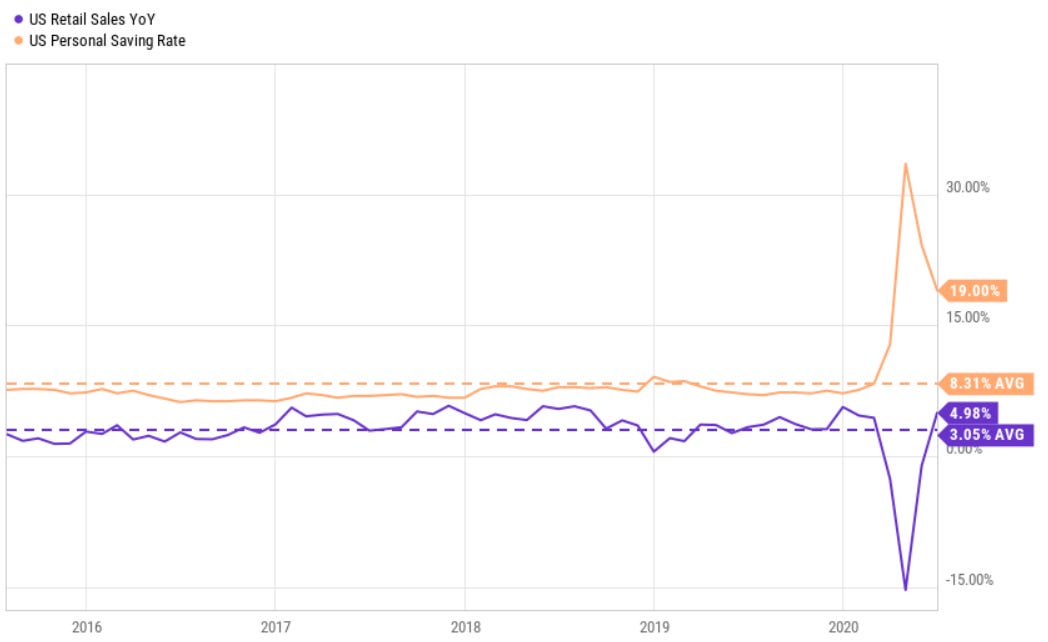

WSJ reported that personal income was down 1.1% in June and highlighted all the troubled individuals in the world — this is a bunch of crock.

Disposable income in June was running at a $17.7tn annualized rate — compared to ~$16.5tn rate in each of November 2019 through March 2020 — the data shows that most individuals are better off right now.

On top of that, thanks to the additional income, we’re also saving more than usual — a $3.3tn annualized rate compared to the ~$1.2-1.3tn level pre-COVID…

The last reading on retail sales also show we’re now (as of June) spending more compared to last year and historic averages.

So… we’re earning more, saving more, and spending more, all at the same time… And a new stimulus bill is set to extend the program that made all of this happen?

Hmm…

Quick Value

Emcor Group (EME)

Another nice little industrial services business… Emcor provides electrical and mechanical services in construction and facilities maintenance.

Think of them as a very large version of your local electrical, HVAC, plumbing company and only focused on business projects (no residential). Everything from building out a brand new factory or chemical plant to regular maintenance services on those same plants.

The newbuild or new construction side of the business is about 60% of sales with the rest coming from mostly recurring maintenance services. Of the $5.6bn in newbuild/construction revenue — nearly 2/3 comes from smaller projects of $10m or less while the larger projects (up to $150m or so) typically run multiyear contracts.

There are 55m shares outstanding x $68.50 stock price = $3.8bn market cap. Net debt is zero (more cash on hand than total debt).

Performance will likely decline in 2020 from COVID but 2019 saw $5.78 in earnings and $550m+ in EBITDA = 12x PE and 6.9x EV/EBITDA.

Emcor has historically been well-run in the sense that they generate good cash flow with minimal debt. In fact, this business has been a long-time cash machine…

Of the $2.25bn in cash generated during the 10-years from 2011 to 2019

$1.5bn (67%) went to acquisitions

$787m (35%) went to share buybacks

$300m (13%) was spent on capital expenditures

$166m toward a small dividend payment

and only a net $126m cumulative increase in borrowings

Emcor heavily favors using cash to do tuck-in acquisitions with buybacks rounding out the remainder of their free cash flow while mostly holding steady on debt.

COVID makes this a difficult business to analyze, especially as some plants are restricting access by third-parties and there is some heavy oil & gas exposure. Overall, this seems to have a good recurring maintenance service segment and cash flow has grown at a 10% annual rate over the past 10 years.

A nice place to hunt for new businesses — where fundamentals have been improving for quite some time but valuation metrics have held steady. In Emcor’s case, while revenue and cash flow have improved over the past 10 years, valuation is either unchanged or lower than it has been in the past!