Quick Value 9.14.20 (FISV)

Fiserv Inc ($FISV)

Market Performance

Another week of downward trend across all indices with most markets practically unchanged over the past 8 weeks / 2 months…

Market Stats

Inflation looks like it’s running high with a few months of bigger than usual gains.

This looks more like a rebound from declining prices in March through May in an attempt to “return to normal.”

The Federal Reserve has an objective of maintaining price stability which they deem to be 2% inflation on an annual basis. As a country, we’re still having a hard time maintaining this target.

Famed investor Stan Druckenmiller was recently on CNBC talking about the risks of both inflation and deflation in the current market environment. Thanks to the $3.5tn stimulus package, Druck warns we might see 5-10% inflation rates over the next few years. Conversely, he also thinks we’re running the risk of deflation as well.

How is this possible?

There are all sorts of factors at play. But one of the most vital in my mind is the fact that we’ve seen this massive increase in the Government balance sheet since coming out of the crisis yet almost no uptick in the rate of spending as measured by money velocity:

So where is all of this going?

The new Modern Monetary Theorists (MMT) makes the argument that this Government spending is creating a surplus on private sector balance sheets and as long as inflation / demand for money remains intact then it creates a net societal benefit. An interesting concept for sure… Time will tell!

Quick Value

Fiserv Inc (FISV)

Fiserv is a Milwaukee-based payments-technology company.

The business had done a good job of growing on its own for years and in 2019 combined with First Data Corp in an all-stock deal issuing ~288m shares for $29bn. First Data had always been pretty cheap but carried high levels of debt from their LBO days.

Fiserv provides electronic payment and account processing services to banks, a mission critical function for processing transactions. While Fist Data is a major player in credit/debit card transaction processing serving some 6m businesses around the world.

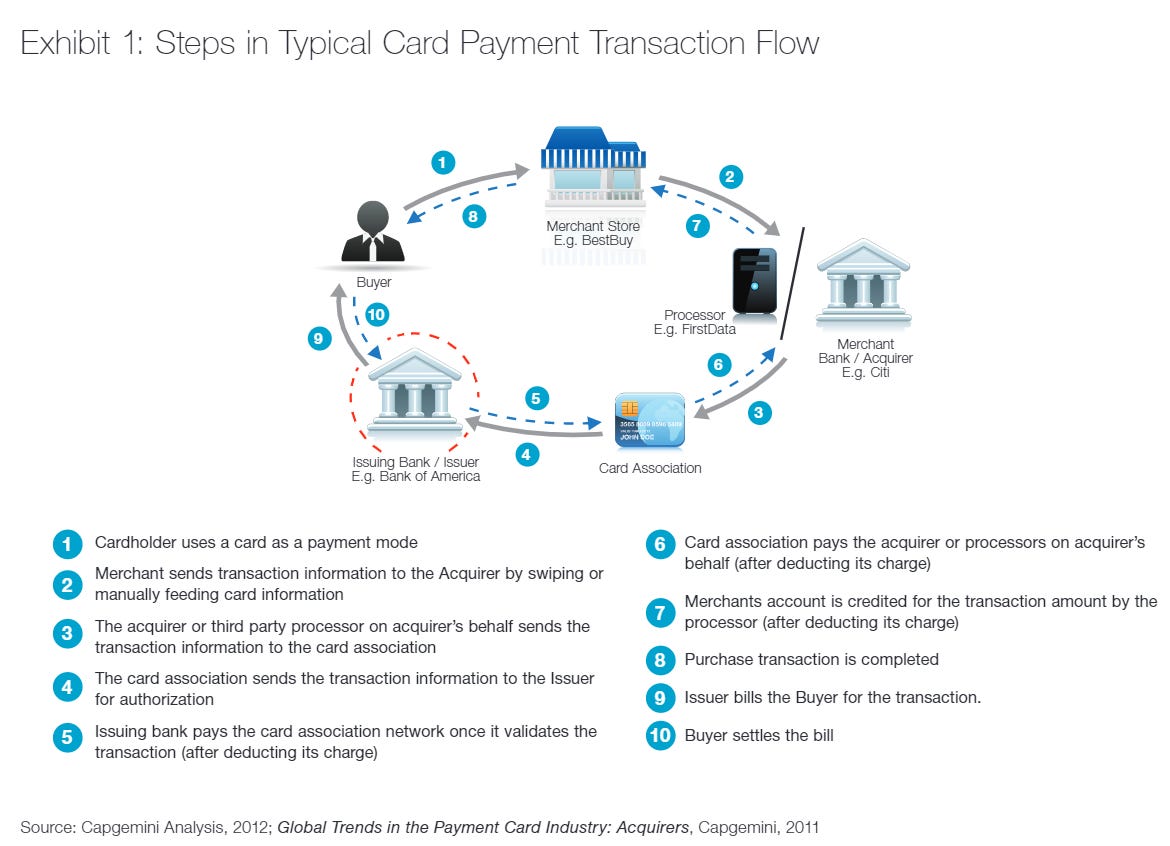

This is a somewhat complicated industry but this visual layout helps to explain where Fiserv (and First Data) fit in the value chain…

After the First Data merger, there are now 670m outstanding shares at a $93 stock price = $62bn market cap. There is $21bn or so in net debt for an enterprise value of $83bn.

When the deal was announced, they called for $3.6bn in annual free cash flow include just shy of $1bn in synergies… This is about $5.40 per share or 17x P/FCF at today’s price. Maybe not outrageous with other merchant processing peers GPN and FIS trading >20x earnings today and all players having solid growth prospects thanks to increasing digital payments.

Prior to the merger, legacy Fiserv had been plowing most of its cash flow into smaller acquisitions and primarily stock buybacks. First Data didn’t have much of an option with their $1.5-2bn in free cash flow other than to repay the massive $16bn debt pile (which has since been inherited by the combined company).

This makes for a somewhat interesting combination…

Both of these businesses are growing organically. First Data didn’t have any capital deployment options other than to repay debt. Fiserv didn’t have enough capital deployment options other than to buyback stock (at lofty prices too).

Following the deal, Fiserv has effectively levered up only modestly — about 3.5x net debt to EBITDA at $6bn in EBITDA — and will likely spend some time getting into a “reasonable” range for leverage. This might be a much better decision on returns compared to buying back stock at 20-25x earnings over time.

There are other nuances to the industry but that’s worth a deeper dive. At a high level, you have a $62bn company doing $3.5bn+ in FCF with modest debt and good sales growth.

Consider, for instance, that AT&T (T) has a similar ratio of debt to FCF — about 6x — yet they are committed to paying about 60% of that 6x in dividends per year… Fiserv is free to quickly repay debt and then find the next arrow in the quiver…

Here are some key metrics touted by the company during the Q2 earnings release: