Quick Value 9.21.20 (EPAC)

Enerpac Tool Group (EPAC)

Market Performance

Forget about those back-to-back weeks of market declines! (At least in small stock land.)

The past 8 weeks (2 months) have been solidly positive for stocks while treasuries, gold, oil, and VIX have been pretty much flat.

Market Stats

Retail sales data showing that spending is continuing as normal. Retail sales were up 2.6% from the same month last year and only a few categories are still showing declines — mainly restaurants, retail stores, and gas stations. Eccomerce (nonstore) continues to shine with 20%+ YoY growth.

Interestingly, these retail sales growth rates are similar to what we experienced for nearly all of 2019…

Don’t forget that consumer spending makes up a disproportionately large piece of economic activity. If these levels continue chug along, then economic growth should follow.

Quick Value

Enerpac Tool Group (EPAC)

This is another small-cap industrial stock formerly known as Actuant (ATU). It was a mini-conglomerate of industrial and energy businesses for quite some time but has whittled down the portfolio and rebranded as Enerpac.

Don’t feel like you’ve missed out in not knowing about this business as it’s gone nowhere for 10 years year now!

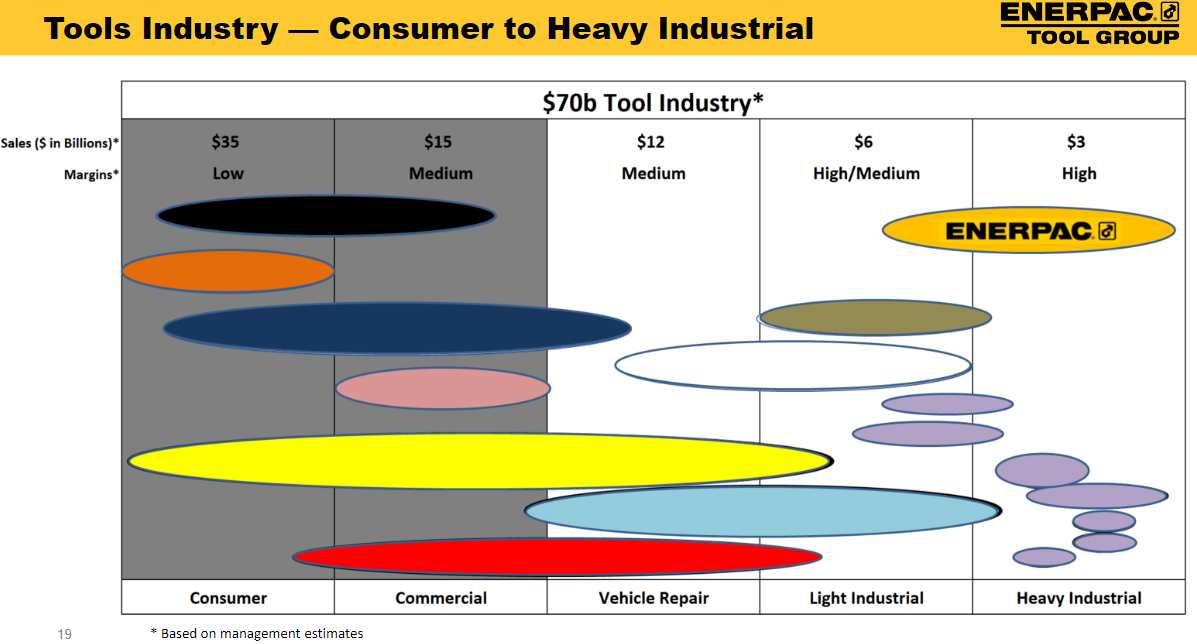

The core industrial tools business is a small part of the larger tools industry and narrowly focused mainly on heavy machinery. Enerpac sells hydraulic tools used in very high pressure circumstances, oftentimes in oil & gas, machining, and infrastructure end-markets.

They’ve since exited their energy and engineered products divisions and used the proceeds to repay debt…

What’s left is a pretty nice little industrial company… With mid-to-high teens operating margins and very little invested capital (about $180m between working capital and equipment).

COVID has had an impact. FY20 results are down significantly with the recently ended fiscal 3rd quarter sales down 38% or so. Orders are starting to rebound somewhat but still look well below past years.

What’s potentially interesting about the business is now that the divestitures have been wrapped up, management feels like they can add about 10% to EBITDA margins — going from 15% to 25% over the next few years. Corporate costs are still extremely high at >$40m despite shedding some $600m in sales over the past few years via divestitures. So some of this margin expansion seems doable.

We already know that industrial activity is starting to rebound via PMI data so this business should track pretty closely with that over time.

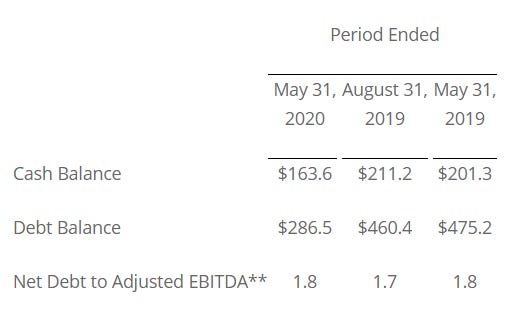

There are 60m shares outstanding x $22 = $1.3bn market cap. Add $123m in net debt for a $1.4bn enterprise value. If they can ultimately achieve the 25% EBITDA margin on $600m or so in sales = $150m / 9x.

That doesn’t seem all that cheap but remember this is a business that requires very little capital leaving most cash flow available for capital returns or acquisitions.

Interestingly, the company has already started buying back a decent amount of stock during the pandemic — $27m in total YTD of which $10m came in the most recent quarter…