Quick Value 9.28.20 (VVV)

Valvoline Inc (VVV)

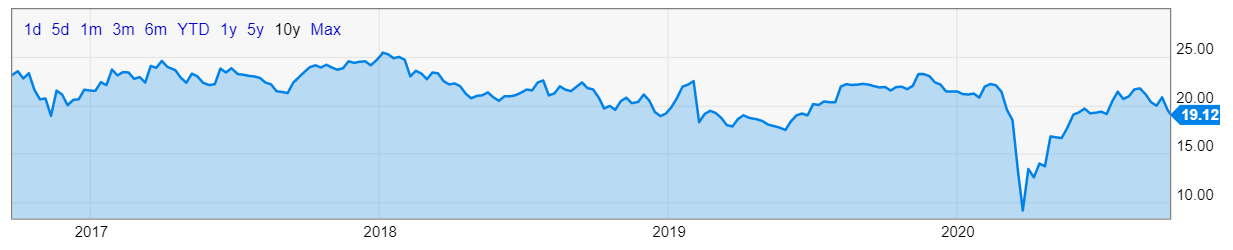

Market Performance

Most asset classes have been pretty stable for 2 months now, mostly bouncing around and settling in “slightly down” over that period.

Small stocks have weakened relative to larger stocks, gold has been weak, and oil prices have been pretty darn stable.

Market Stats

Saw a great thread on Twitter the other day highlighting COVID vs GFC that I’d like to share… It summarized 10 data points and the duration it took to “return to normal” during COVID vs GFC recessionary periods. Spoiler: almost every data point has recovered much faster during the current recession

Manufacturing PMI — 6 months (COVID) vs 10-11 months (GFC)

Retail sales — 6 months (COVID) vs 33 months (GFC)

Yield Curve@TenYearNote2. US retail sales have returned to pre-crisis levels within six months compared to 33 months during the GFC and reached new highs in August12:45 AM · Sep 23, 20201 Repost · 9 Likes

Yield Curve@TenYearNote2. US retail sales have returned to pre-crisis levels within six months compared to 33 months during the GFC and reached new highs in August12:45 AM · Sep 23, 20201 Repost · 9 LikesPersonal income — 0 months (never declined) vs 18 months (GFC)

Yield Curve@TenYearNote3. US personal income has been above pre-crisis levels since April. Took 18 months to return to pre-crisis during GFC. US personal incomes are expected to be above pre-Covid-19 levels in August even as stimulus has ended in July. Savings rate 17.8% now versus 5.9% during the GFC12:45 AM · Sep 23, 20201 Repost · 9 Likes

You can flip through the rest yourself. These first few cover the arguments I’ve been trying to make for a while now in that COVID hasn’t hit consumer finances as hard as you’d imagine. The stimulus response in the CARES Act was profound and plugged the entire consumer “leak” (for now).

Now we have commercial activity rebounding strongly as well. Manufacturing (PMI), home sales and construction, auto sales, etc.

Quick Value

Valvoline Inc (VVV)

I received plenty of great responses to a question posed on Twitter recently but one respondent came back with a vigorous pitch for Valvoline (VVV).

Here are my quick notes on the stock…

Valvoline was spun-off from chemical company Ashland in 2016 and consists of 2 businesses:

Valvoline Instant Oil Change (VIOC) — Chain of Quick Lube stations in the US and Canada.

Products — Sells Valvoline branded engine and automotive products in North America and Internationally.

From a sales and profits standpoint, the Quick Lube business is about 1/3 of sales but closer to 45% of total company operating profits.

Have I mentioned I like stocks that have gone nowhere for years??

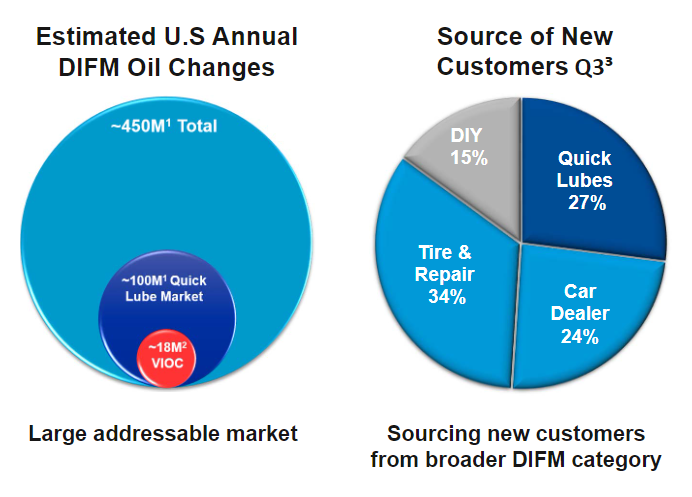

You wouldn’t recognize it from the stock price but the Quick Lube division is performing quite well with solid growth prospects. It’s a small chunk of the overall oil change market and Valvoline is winning customers from multiple sources. Of the 450m oil changes each year, Quick Lubes have about 100m and VIOC with 18m or so.

After a rough period from March to May, sales growth has resumed its healthy pacing… And the company isn’t holding back on opening new locations. Store count (both company owned and franchised) grew from 1242 in FY18 to 1385 in FY19 and 1432 as of 3Q20.

The other businesses here are a bit lumpier with inconsistent performance in sales and EBITDA.

Some numbers…

There are 185m shares outstanding x $19 stock = $3.5bn market cap. Net debt is $1.3bn or so for a $4.8bn enterprise value. Management is calling for $475-485m in FY20 EBITDA or ~10x EV/EBITDA.

Free cash flow has been pretty stable / stagnant around $200-250m the past few years so call it 14-17x P/FCF.

There are mixed levels of performance within the segments here:

Quick Lube has grown from $111m to $214m in EBITDA — 18% CAGR

Core NA and International went from $301m to $264m — negative 3% CAGR

The combination of these likely having the net effect of a stock that’s gone nowhere for a few years…

Over the past 2.75 years, Valvoline has generated $916m in operating cash flow (vs. the current $3.5bn market cap). They also borrowed an additional $818m in debt during that time but most of it sits on the balance sheet as $750m in cash. Of that amount they spent:

$295m on capex (mostly new locations in the Quick Lube segment)

$221m on acquisitions

$385m in share buybacks

$201m in cash dividends

So there you have it… A fast-growing oil change business coupled with a struggling oil products business. While there’s also a possibility these businesses could be separated, it seems management is set on deploying the cash flow from the products businesses back into the growing oil change business (at least for now).

This one definitely seems worth a closer look…