Quick Value 9.8.20 (LBRT)

Liberty Oilfield Services (LBRT)

Market Performance

Continuing with the new format this week…

Markets gave back some gains over the past week but nothing noteworthy over the past month and a half…

Market Stats

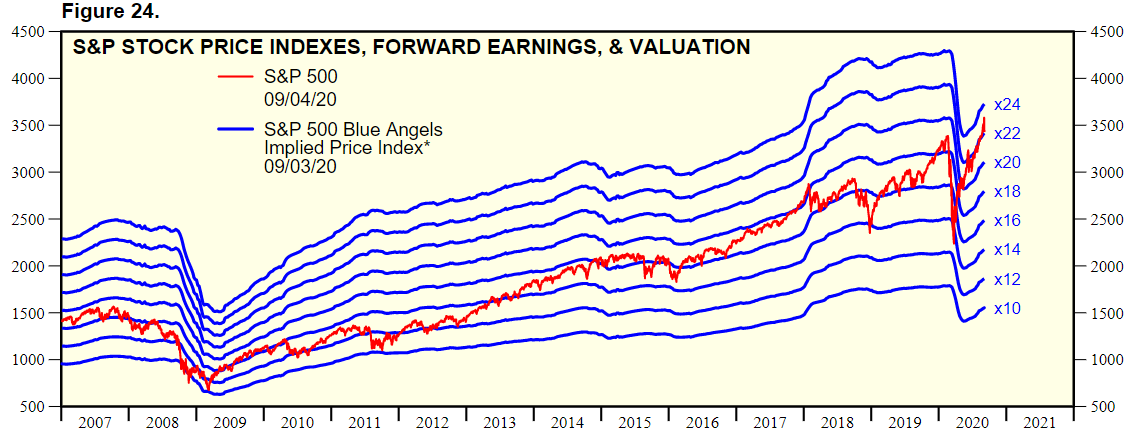

With the S&P 500 at the 3400 level and projected earnings of 166 in 2021 that leaves us with a 20.5x earnings multiple on next year’s projected results…

Not entirely cheap when you look at past averages…

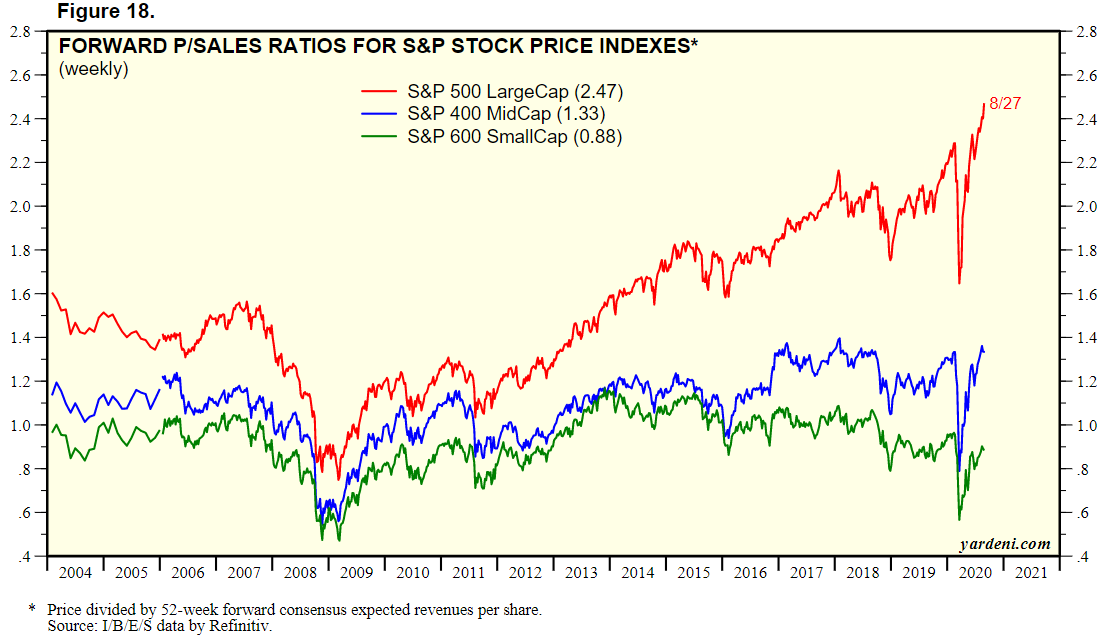

Plenty of press coverage on the divergence between growth vs. value and large vs. small but this price to sales chart visually explains it best…

Business activity continues to pick up pace…

The August jobs report released last week showing another 1.4m jobs added, a 5% increase in hourly wages,

Quick Value

Liberty Oilfield Services (LBRT)

Last week, oilfield services giant, Schlumberger (SLB), announced they will sell their North American fracking business to Liberty Oilfield Services (LBRT) in exchange for a 37% ownership stake in the combined business.

2019 figures aren’t all that useful in oil & gas at this point but the net result is a much larger player in the fracking industry…

…along with one of the better balance sheets in the industry.

This is a pretty fascinating transaction for a business that has historically been a serial acquirer (SLB) to turn around and divest some 10% of its total revenue base. And the oil industry still has a long way to go in returning to the glory days… (if ever)

Liberty Q2 results highlight this pretty well with revenue down 84% to $88m from $542m. This is what a business looks like when customer needs grind to a complete halt.

Most competitors are highly levered and potentially majorly disadvantaged as a result… But is this an industry that has a long-term future? Look at what happened with major coal companies following the wave of bankruptcies, even with clean balance sheets results have been lackluster…

There was never much of a shakeout in US crude production following the oil price collapse in 2015-2016… US oil production actually grew from 2015 to 2020. Perhaps that shakeout is taking place today?

One bright spot for a declining business is the working capital benefits adding to cash generation (even if only temporary). This has given Liberty a chance to produce some good cash flow despite revenue struggles.

An already-solid net cash position plus the combination of Schlumberger’s OneStim division could position Liberty well when or if industry demand starts to turn… Management is confident that Q2 results marked a low point in demand.

Transformational acquisitions have a mixed track record but this could be an interesting time to take a look… (Maybe even Schlumberger following the divestiture!)