Quick Value #263 - Nexstar Media Group (NXST)

Ultra cheap TV broadcaster (5.4x FCF), what's it look like without deregulation/M&A?

Today’s idea:

Largest TV broadcaster with 200 stations in 40 states

Buyback machine (35% repurchased since 2016)

Trading at 5.4x FCF with stable cash generation

Optionality for acquisitions/spectrum

These write-ups are surface scratchers meant to keep your idea generation flowing. For newer subscribers, check out the VDL “home base” for background info, links to key resources, articles, trackers, etc. As always, leave a comment with thoughts or stocks you want to see covered and check out past posts here to get a flavor for recent write-ups.

Quick Value

Nexstar Media Group (NXST)

I’ve seen lots of discussion around the TV broadcasters lately with most of that discussion centering around incoming FCC Brendan Carr and the potential for industry deregulation. I’m looking at NXST purely based on historic fundamentals + organic outlook here.

What they do…

Nexstar is the largest local TV broadcaster in the US with 200 stations in 116 markets across 40 states. Aside from the TV stations, they also own — a 77% stake in broadcast network The CW, a 33% stake in TV Food Network, and websites with 103m monthly visitors.

There are 2 roughly equal-sized revenue streams in this business:

Distribution — Monthly fee income from distributors (cable and satellite cos, streaming aggregators like YouTube TV, etc.) based on total subscribers.

Advertising — Sale of local and national ad space across all platforms (TV, websites, apps, etc.). This revenue stream is seasonal based on political ad spend and major events (Olympics, Super Bowl, etc.).

Station operators don’t breakout their revenue exposure between linear (i.e. cable bundles) and streaming (i.e. carriage on platforms like YouTube TV). The former is a secular decliner and the latter is growing. These station operators only produce a small portion of content for their affiliated network (FOX, CBS, ABC, NBC, CW) so it’s unclear how these business models will transition to a fully streaming world.

This “linear” exposure is a key reason for low industry multiples. So far, the revenue declines haven’t popped up at Nexstar.

Why it’s interesting…

A purely quantitative look at the fundamentals would lead you to believe this is a good business. Revenue is growing, FCF is stable, debt and leverage are declining, share count is down 35% since 2016, etc.

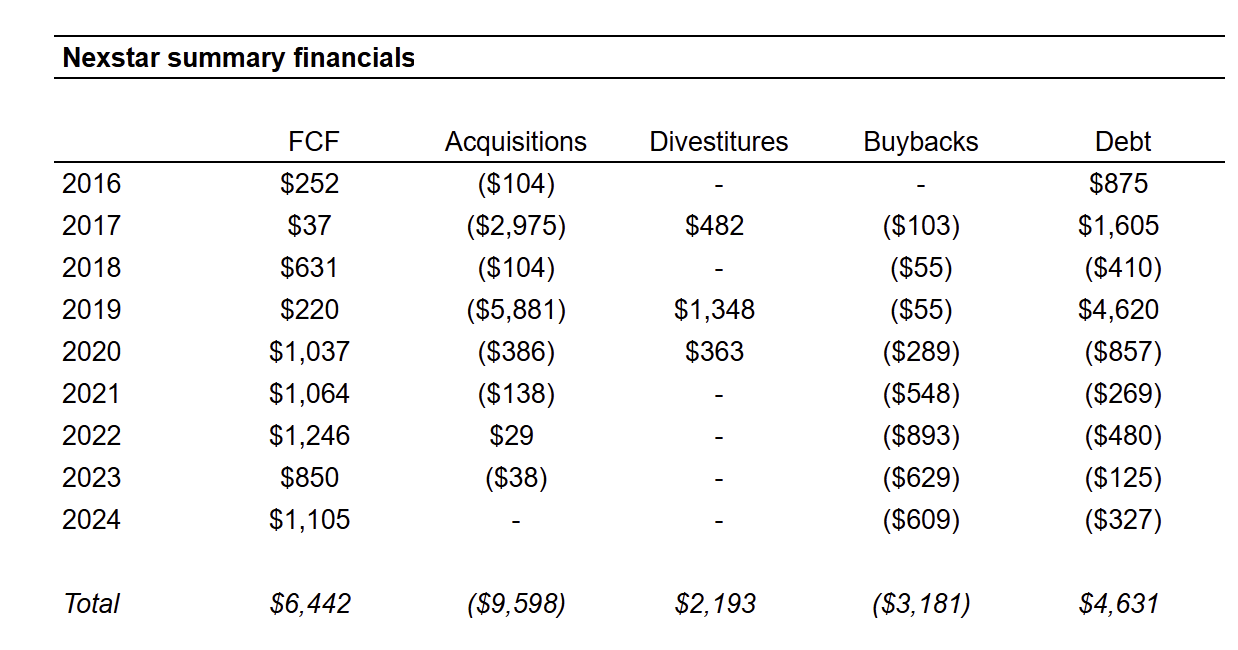

This business generates a ton of very stable cash flow with low capex requirements. FCF:

There are FCC limitations on station ownership (hence the upside optionality from deregulation) so we can see acquisitions tapering off heavily after 2 large acquisitions in 2017 (Media General) and 2019 (Tribune).

Total FCF is stable around $1bn per year following those large acquisitions (2020-2024). Without an ability to do M&A, that cash is getting funneled into buybacks ($670m per year) and debt paydown ($300m per year). With $1bn average FCF at 30.5m shares = $33 per share.

With the substantial exposure to linear TV and cord-cutting, these businesses are perceived as secular decliners and priced as such with low single digit FCF multiples:

Cable TV subscribers are declining ~4-6% per year. Currently 66.1m subs down from a 2010 peak of 105m subs. Virtual subs (again, YTV) are ~19m so the combination of linear + streaming is still way below peak. In theory, at some point that should stabilize once streaming overtakes total subscriber count.

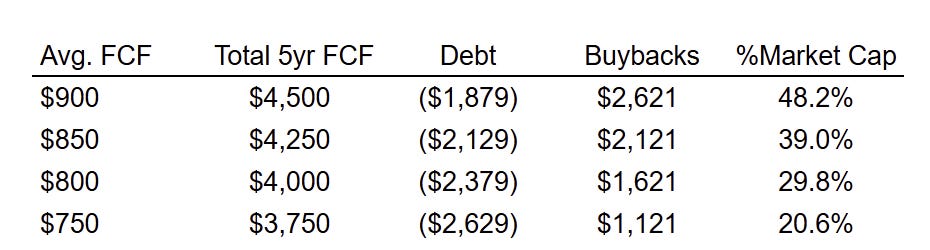

As a thought exercise, say the next 5 years average a lower level of FCF to account for business declines. Assuming they reduce leverage to 5x debt/FCF along the way, how much room would that leave for buybacks? Anywhere from 20-50% of the current market using pretty conservative FCF estimates.

There are some other assets here too… as a “hedge” of sorts, Nexstar owns 77% of the 5th largest affiliate, The CW, along with Paramount and Warner Bros. They also have an ownership stake in The Food Network which is owned and managed by Warner Bros. There’s a cable network NewsNation and all of their website properties too.

Summing it up…

Management is banking on some deregulation to give them capital allocation whitespace for more M&A. The cost savings would be significant to run additional stations off of a single fixed cost base. Without that, what do you have here? Probably some intense revenue and FCF pressure in 5-6 years (that fixed cost base works the other way too).

There are 30.5m shares outstanding x $178 = $5.4bn market cap. Net debt is $6.4bn for a $11.8bn enterprise value. That works out to ~5.4x average P/FCF and 11.8x EV/FCF.

Let’s assume the next 5 years operate at $850m avg. FCF and they repurchase 35% of shares (down to 19.8m) = $43/share. At a similar 6x multiple (lower leverage) = $258. Works out to a ~10% IRR. Pretty draconian maybe.

M&A would be a nice catalyst and maybe you’re getting compensated for that optionality right now? Without acquisitions, it’s pretty challenging to know what this business looks like in 5-6 years. Also, I could see them pausing/slowing buybacks to build cash for M&A until that picture clears.

Welcome any thoughts on organic outlook for this or peers!

Resources:

Do you have an idea of how the landscape looks if deregulation plays out? Downside protection seems pretty decent from what you wrote, wondering how the upside looks like.

"Let’s assume the next 5 years operate at $850bn avg. FCF..." It should mean 850 million, shouldn't it? Great post regardless, thanks a lot!