Quick Value 9.11.23 ($VLTO)

Veralto Corp - Spin from Danaher with high quality potential

Today’s Quick Value looks at the upcoming spin-off of Veralto Corp (VLTO) by Danaher (DHR)… this one is coming fast by end of September so I wanted to get a sense for fair value in case we see an initial mispricing…

Subscribe below for access to all posts (it’s inexpensive idea generation!). And as always, feedback or new ideas are welcomed in the comments. Thanks for reading!

Market Performance

Market Stats

Job growth has been slowing to pre-pandemic levels. This WSJ article highlights slower pace of hiring going on…

Quick Value

Veralto Corp ($VLTO)

Danaher (DHR) [covered previously in Feb 2023] announced in September 2022 they’d spin off their “Environmental & Applied Solutions” business (which they describe as a “leader in water quality and product identification”).

That spin will begin trading later in September so we have all the necessary info to evaluate it:

What they do…

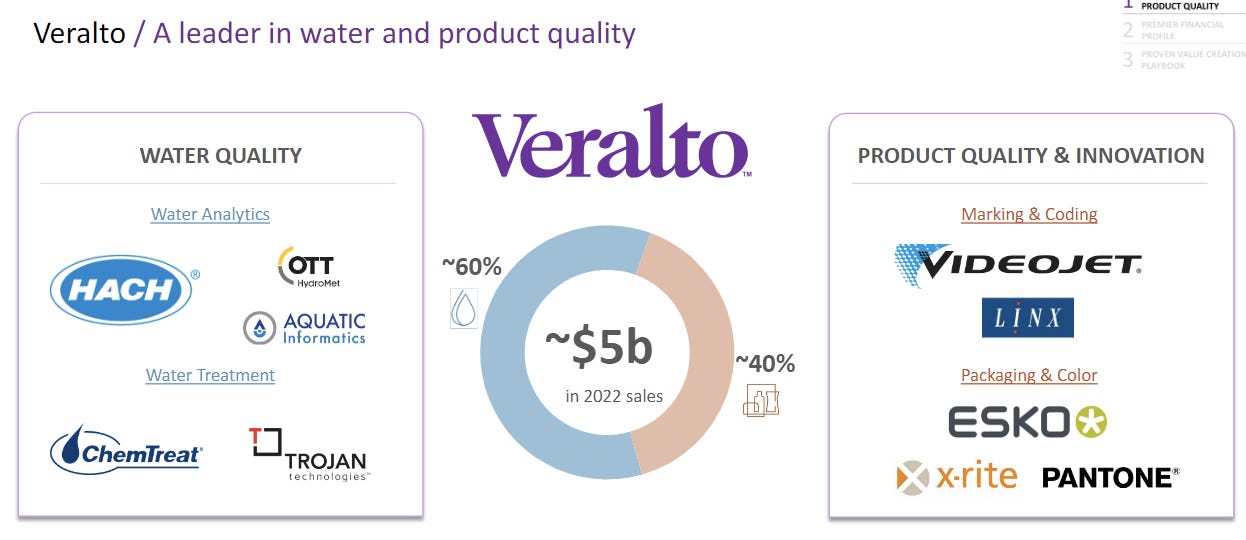

Veralto operates 2 segments:

Water quality (WQ) — Described as “water analytics” and “water treatment” — WQ generates revenue from selling instruments (which can be large lab-based equipment or small handhelds) along with consumables (testing kits, reagents, etc.), services (maintenance/inspection), and accompanying software. The customer base includes: water utilities of all sizes (small municipalities to large public companies) and industrial customers.

Product quality & innovation (PQI) — There are a handful of brands/businesses in this segment… the largest is Videojet which is a coding printer for packaged goods (think expiration dates on your yogurt). Other businesses include packaging/label design software and a color management library (Pantone) which is pretty much ubiquitous in the graphic design field. Again, revenue is derived from an installed base + consumables with services and software tacked on. The offerings in this segment include printers, chemicals, inks, spare parts, etc.

Both of these businesses have similar business models with an installed base and recurring sales of consumables (razor / razor blade model). The products and services are targeting opex of their customers and likely represent very very small pieces of overall operating budgets. Recurring revenue is 57% according to the investor presentation (I wonder how that compares to other “installed base” business models?).

Why it’s interesting…

1) Consistent growth

Veralto looks like an absolute machine both on organic growth and acquired growth. Revenue grew 9.5% annually from $770m in 2002 to $4.9bn in 2022 with operating profit growing a slightly faster 11% annually.

They’ve done 80 acquisitions within Danaher (mostly tuck-ins) and expanded margins/ROIC over the years…

Here we can see the breakout between organic growth and acquired growth annually since 2013… it’s an impressive picture with each segment growing organically nearly ever year.

Long-term guidance calls for mid-single-digit organic revenue growth across both segments.

2) Excellent fundamentals

After reviewing the documents, there wasn’t any single variable that made this standout as a good business. It was a grab bag of factors that lead me to believe this is a high quality company, here are some of them:

Recurring revenue is pretty high (57% of sales)

Business targets small portion of opex vs. capex at customer budget (i.e. mission critical)

EBITDA and EBIT margins well over 20% with close to 100% FCF conversion

Asset light business with <1% capex/sales

Consistently positive organic growth with successful M&A (but not overly reliant on growth via M&A)

Used the Danaher Business System (DBS) to improve ROIC/margins on nearly 80 acquisitions since 2002

3) Renewed capital allocation

More than anything, the cash flow statement jumped out to me as both a bright spot and an opportunity post-spin.

Operating cash flow from 2020-1H23 totaled $3.22bn and capex was a measly $145m… they spent $236m on acquisitions (<8% of op cash flow) and distributed $2.9bn back to parent Danaher… that tells me they’ve kept a lid on reinvestment and used this segment as a cash machine for investing in other businesses at the parent level.

Here’s what management had to say about capital allocation during their investor presentation:

Moving on to capital allocation. Jennifer earlier talked about our plans to leverage capital allocation to benefit our shareholders. Let me just expand on that a little bit because our -- because we believe our capital allocation optionality is a key lever for us to create long-term value. Our bias is to compound the earnings through high ROIC organic growth opportunities aligned with the great secular trends that you just heard. And then strategic acquisitions that drive long-term value accretion. Within our framework, we'll also maintain some flexibility to return cash to shareholders, potentially will be a modest dividend and having an ability to flex on share buybacks.

They didn’t dig deep into the M&A opportunity on the call but my sense is that organic growth will be priority #1 but that path will have a limited capacity for reinvestment dollars. Management sounds excited about opening up acquisitions compared to the small sums deployed over the past 3.5 years…

Summing it up…

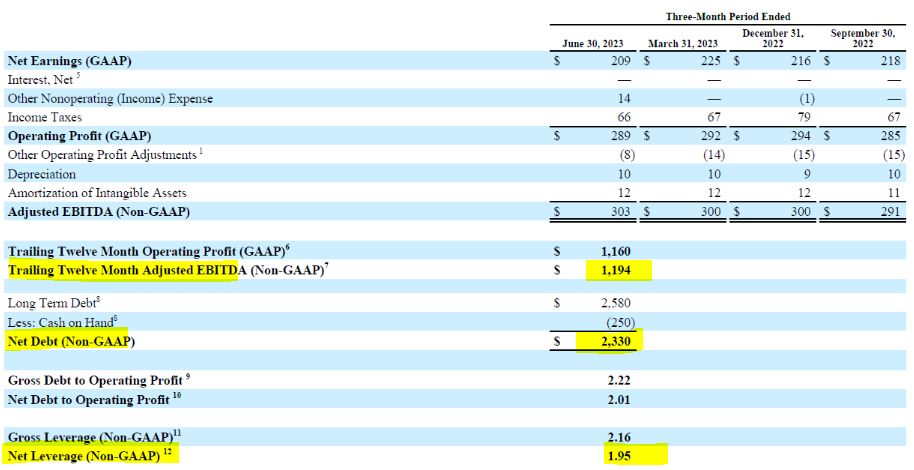

Veralto will be spun with a 1:3 ratio so there will be ~250m shares outstanding post-spin. Net debt will be $2.33bn for net leverage of ~2x on trailing EBITDA of $1.2bn.

Danaher is currently trading at >21x forward EBITDA so it’s possible both Danaher (RemainCo) and Veralto (SpinCo) maintain that same multiple. There isn’t a perfect comparable to this company but it’s possible several of the industrial conglomerates out there have competing divisions tucked within them… A peer group might consist of the following:

Those are some expensive companies albeit with equally good fundamentals. If we value Veralto at 20x EBITDA that would equate to $29/share (pre-spin share count of 750m) which is right around 10% of the pre-spin Danaher market value. Maybe there will be an opportunity as shareholders sell down the smaller piece? Hmm…