Quick Value #312 - Nomad Foods (NOMD)

Beaten down stock in a beaten down industry + management change

Today’s post:

Cheapest stock in a severely beaten down industry (30-50% declines on average)

Shares trading at 5.7x earnings and 6.5x EBITDA with 3.6x leverage

New CEO started Jan 2026 = management change situation

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: 1) company background; 2) why the idea is interesting; and 3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

04/06/26 — Upcoming spin-off at Middleby ($)

03/23/26 — A look at GameStop fundamentals

03/16/26 — Green Dot upcoming sale + spin ($)

03/09/26 — CBIZ growth to value transition

03/02/26 — Ziff Davis sum of the parts ($)

Quick Value

Nomad Foods (NOMD)

Ticker: NOMD

Price: $10

Shares: 142.1m

Market cap: $1.4bn

Valuation: 5.7x P/E

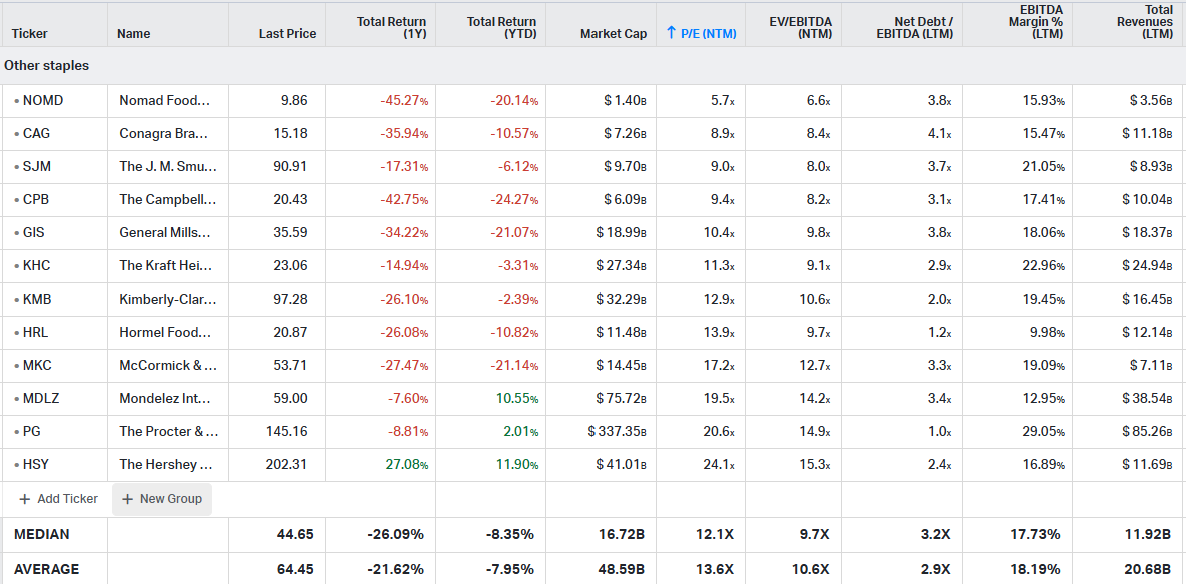

Theme: management change (+ beaten down)Staples and CPG brands are getting clobbered lately with most stocks down 30-50% over the past year:

Instead of working A-Z, I figured I’d just start with the cheapest name on the list… here are my notes…

Background

Starting with some history:

2006 — Unilever sold European frozen food brands Birds Eye and Iglo to private equity firm Permira for €1.7bn.

2014 — Nomad was founded as a SPAC in 2014 by Noam Gottesman and Martin Franklin (Jarden founder and had a few other successful SPACs), they still own ~15% of the company today.

2015 — Nomad acquires Iglo Group for €2.6bn from Permira at an 8.5x EBITDA multiple.

2016-2021 — Sales grew (in part from €1.2bn spent on acquisitions) from €1.9bn to €2.6bn and shares steadily climbed from ~$10 to $30+ at peak before finishing 2021 around $25.

2022-2025 — Pandemic-era volumes declining, revenue growth entirely from price increases, cracks in CPG industry. Shares from $25 to $12.

2026 — Disappointing guidance during 4Q25 earnings call. New CEO kicking off turnaround (inning #1 here).

All sales come from frozen food categories and are concentrated in the Western European region. These are dominant brands with #1 or #2 positions in most markets and product lines.

Some notes about the European frozen food industry:

Categories and markets Nomad competes in valued at ~€26bn (per annual report) = 11-12% market share

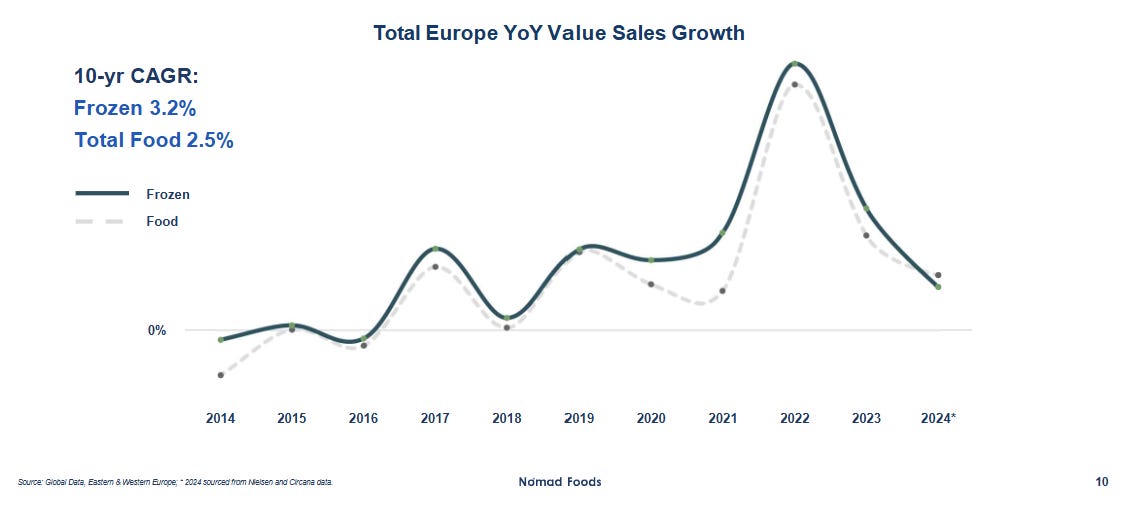

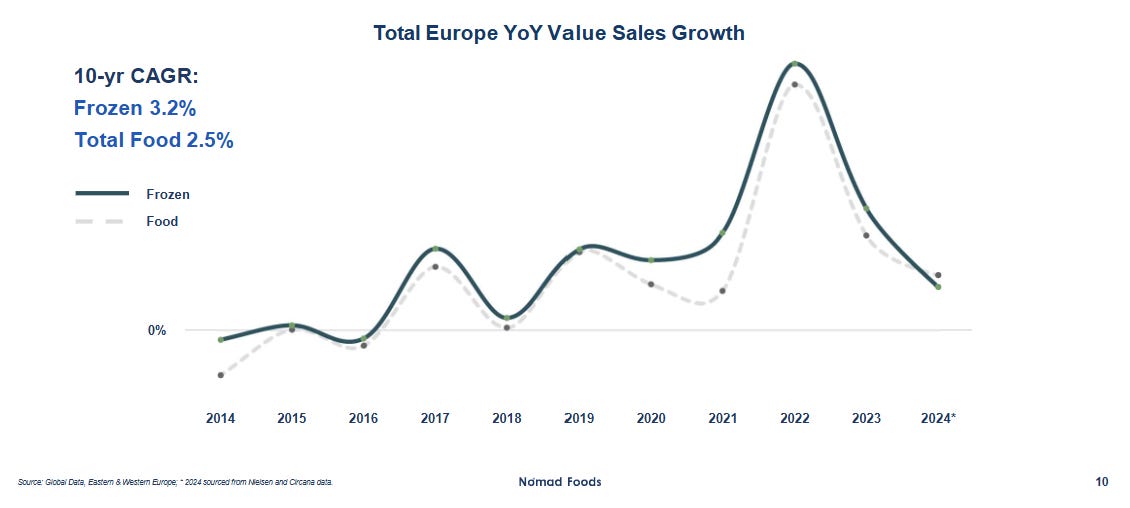

The pandemic saw significant pull-forward in demand and a “normalization” period is still ongoing

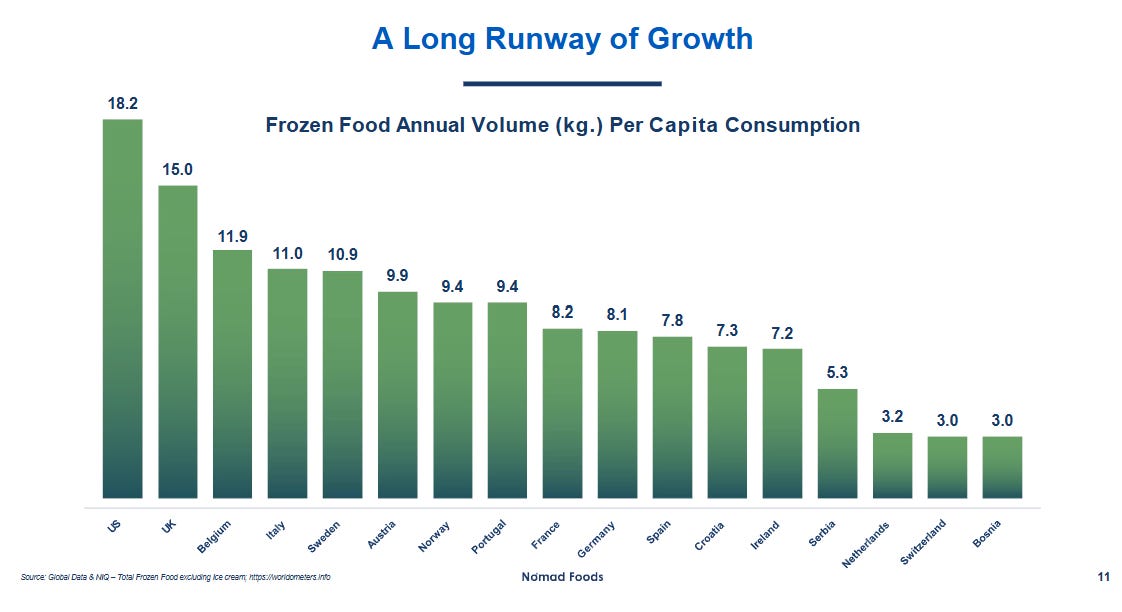

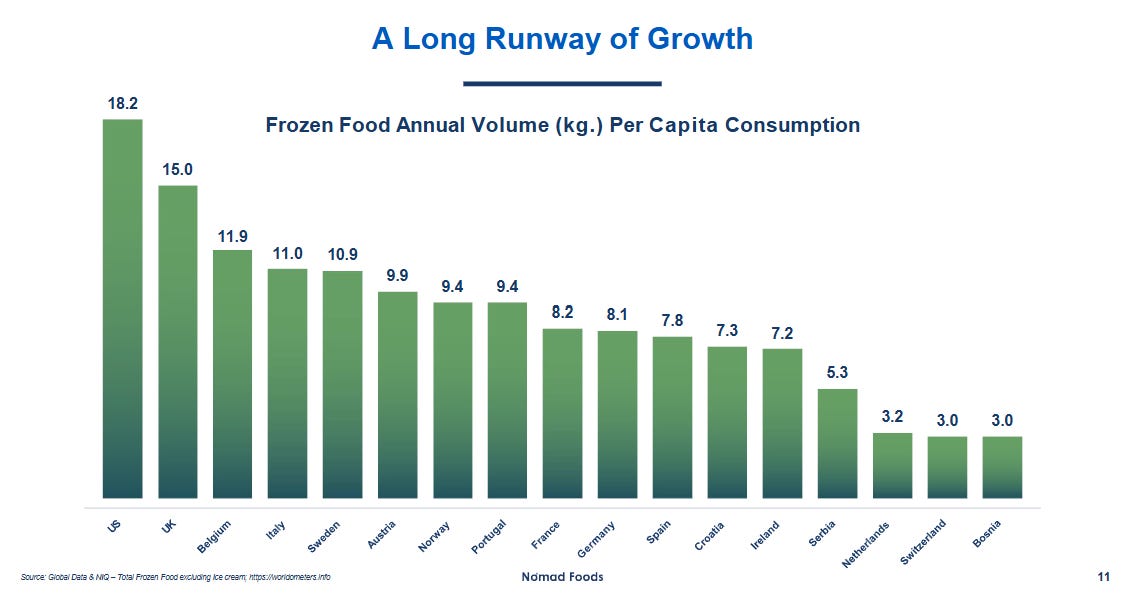

Category sales trends (2014-2024) European consumption of frozen foods is still far behind US levels on a per-capita basis… management views this as a secular growth tailwind

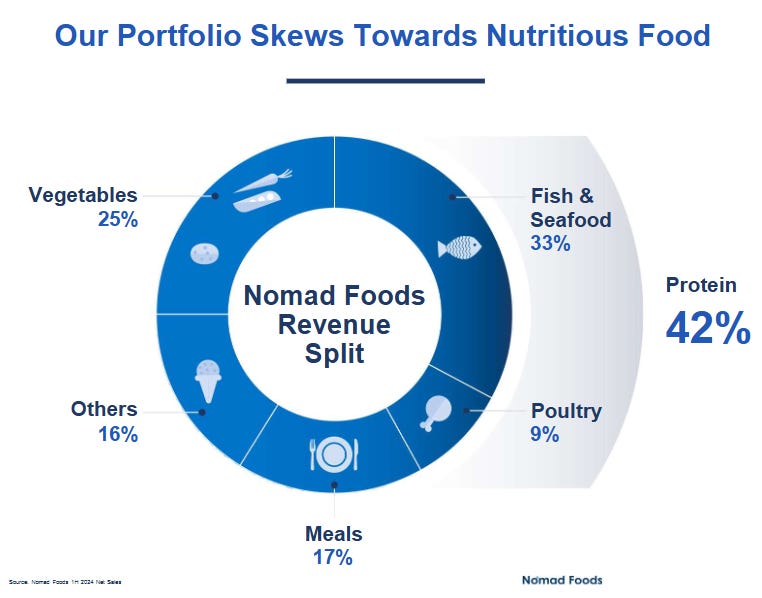

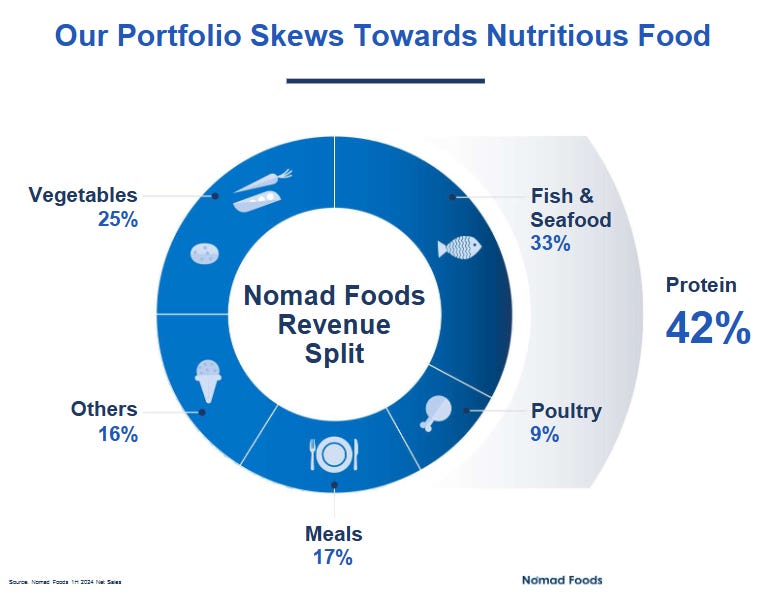

Per capita frozen food consumption by country Again, the product portfolio is entirely frozen foods sold in Europe. The sales mix skews toward protein with a heavy mix of fish & seafood (33% of sales) and vegetables (25%)

Product sales mix Nomad noted they had 50%+ market share in “core” product lines (70% of revenue) during their 2020 investor day… as of 4Q25, that position fell to 39% (though still the #1 brand in most markets)

Why it’s interesting…

I wouldn’t characterize Nomad as a special situation, but it does have certain elements. The 2 things that get me excited here: (1) it’s the cheapest stock in an industry getting hammered lately; and (2) it’s a management change story with a relatively new external-hire as CEO.

1) New Management

Let’s start with the management setup since it’s easier and more interesting…

From my “guide to management changes” article (link below), I laid out a checklist of things I look for in a new CEO: