Quick Value #307 - CBIZ Inc (CBZ)

Beaten down stock transitioning from EPS growth story trading at 20-30x earnings to value stock at 7-8x earnings

Today’s post:

Shares down 42% YTD and ~70% off 2025 highs

Recently completed Marcum acquisition ~doubled size of company

2026 guidance implies 16% FCF yield with management hungry for buybacks

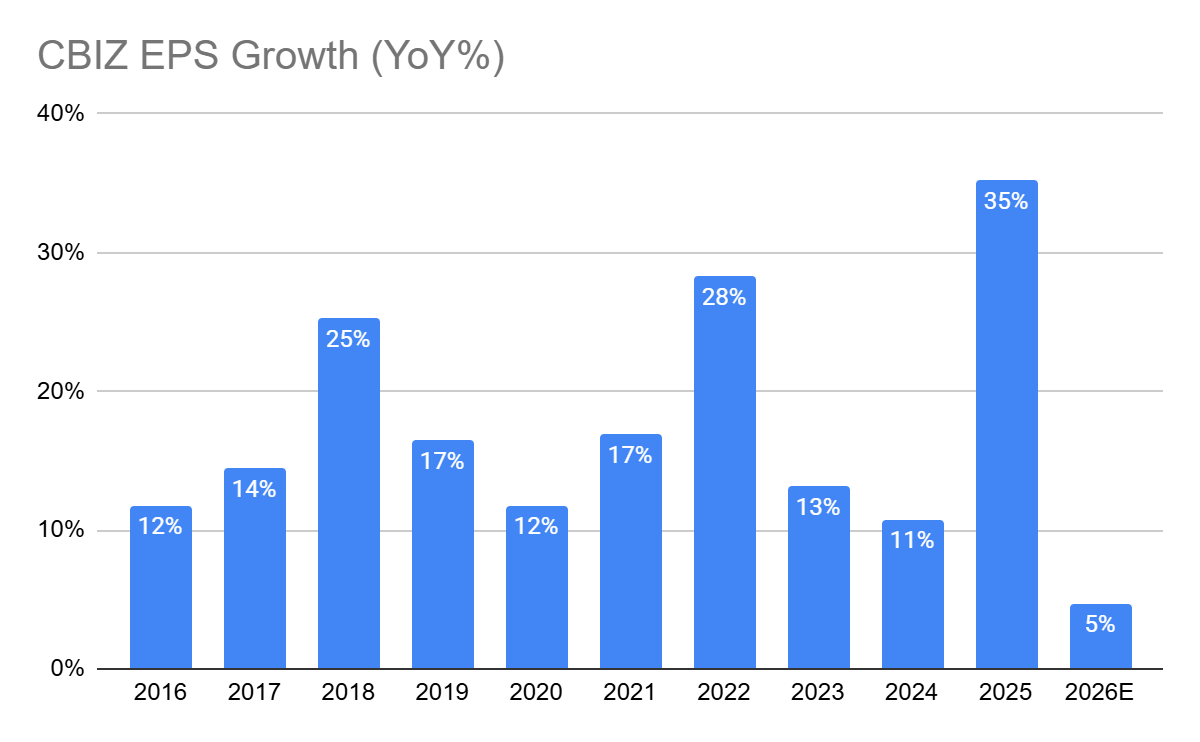

After years of consistent EPS growth (17% CAGR from 2016-2024), now seeing 4-7% EPS growth in 2026

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: 1) company background; 2) why the idea is interesting; and 3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

03/02/26 — Ziff Davis sum of the parts ($)

02/09/26 — Wholesale changes in the VDL portfolio ($)

02/02/26 — A look at Allison Transmission’s recent acquisition

01/26/26 — Multi-pronged special sit Teleflex ($)

01/19/26 — A look at the KBR upcoming spin-off

01/12/26 — Supremex is super cheap and inflecting ($)

01/06/26 — Shares of Cinemark look beaten down

Quick Value

CBIZ Inc (CBZ)

Ticker: CBZ

Price: $29

Shares: 62m

Market cap: $1.8bn

Valuation: 6.5x FCF (2026 guide)

Theme: Beaten downShares are getting pummeled lately as the stock transitions from a growth story (20-30x P/E) to a value story (7-8x P/E). Let’s take a look to see if this knife is worth catching…

Background

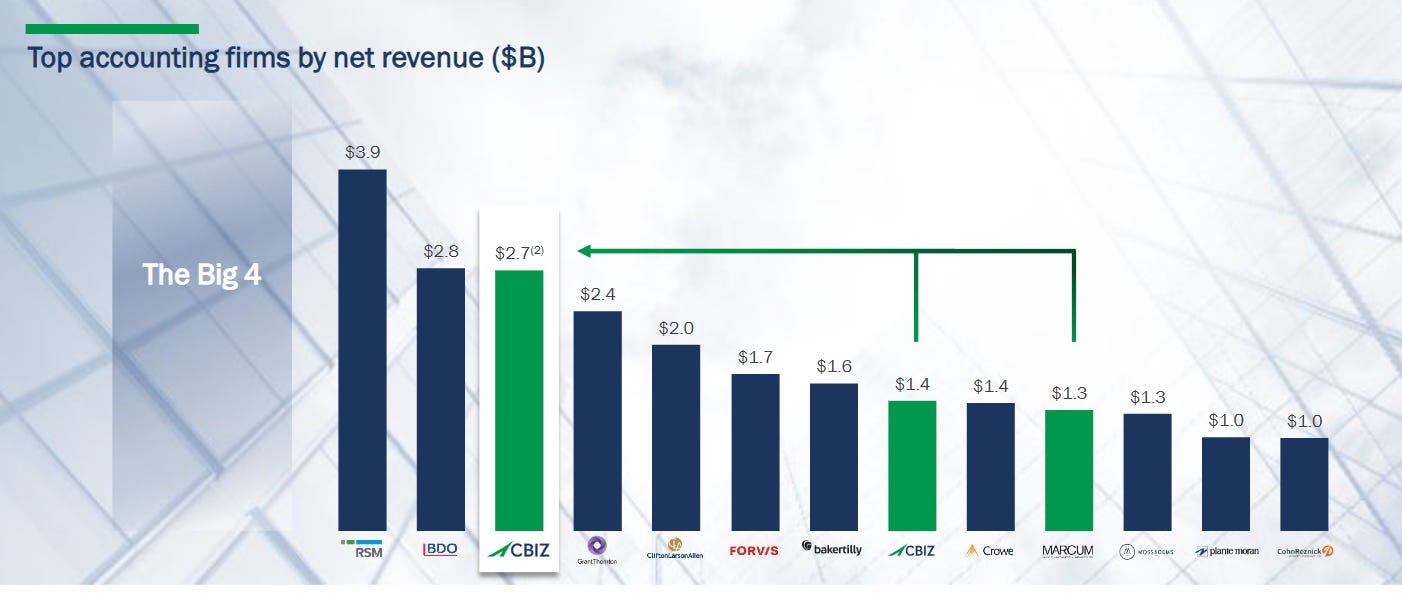

CBIZ is the 7th largest accounting firm in the U.S. providing services like audit, tax, and advisory work.

Historically, CBIZ has been an active acquirer of smaller firms, completing more than 120 acquisitions since 2008.

In 2024, they closed a substantial merger with 13th-ranked Marcum to become the 7th largest accounting provider at ~$2.8bn annual revenue.

This acquisition roughly doubled the revenue base and added substantial debt to the balance sheet (the acquisition was 50% cash and 50% stock issued to Marcum).

Today, there are 3 segments:

Financial Services (83% of revenue) — Accounting, tax, transaction services, advisory, and consulting.

Benefits & Insurance Services (15%) — Employee benefits consulting, insurance brokerage, payroll, and HR services.

National Practices (2%) — Managed IT services for a single client dating back to 1999 (runs on 5-year contract renewals set to expire Dec 31, 2028).

Revenue is mostly fee-based in the core accounting segment (Financial Services) while Benefits & Insurance is commission-based (brokerage) and fee-based (consulting, payroll, etc.). The majority of revenue is recurring (more than 75%).

Why it’s interesting…

This name definitely checks the box for beaten down. Shares have round-tripped over five years from $30 (2021) to $90 (2025) and back below $30 as of this writing (the stock is down 42% YTD).

But why are shares getting killed?

At first, I thought it was purely an “AI disruption” stock. Eventually, Claude will manage your books and do your taxes, right? I believe this is partially a contributor, but the story is more nuanced than that.

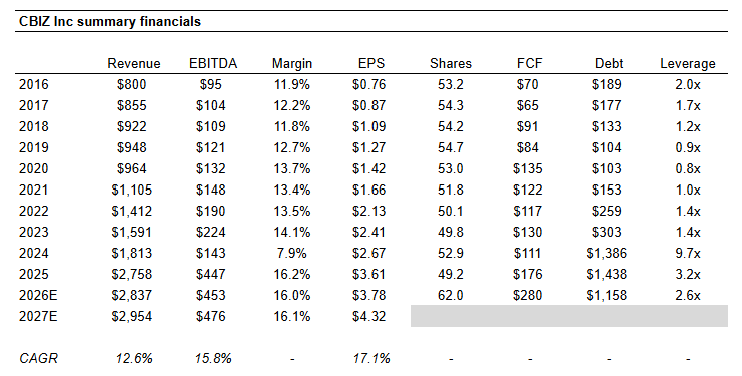

From 2016-2024, earnings per share grew at a 17% annual rate from $0.76 (FY16) to $2.67 (FY24). In fact, each year saw at least 10% YoY growth in earnings. Pretty impressive even considering most of it was acquisition related. In addition to the 17% EPS CAGR, the share count remained flat and leverage stuck below 2x throughout that period. Sign me up!

Then the Marcum acquisition closed in late 2024 which doubled the size of the company, pushed leverage way above norms, added dilution, and flipped the story from “tuck in acquisitions” to “organic growth + buybacks.”

It was a growth stock and now it’s a value stock.

Left for dead.

Looking at the fundamentals, you can see the consistent growth + margin expansion playing out. Share issuance was minimal and leverage consistently between 1-2x. The Marcum acquisition closed ~Nov 2024 with results fully embedded in 2025 and 2026E figures:

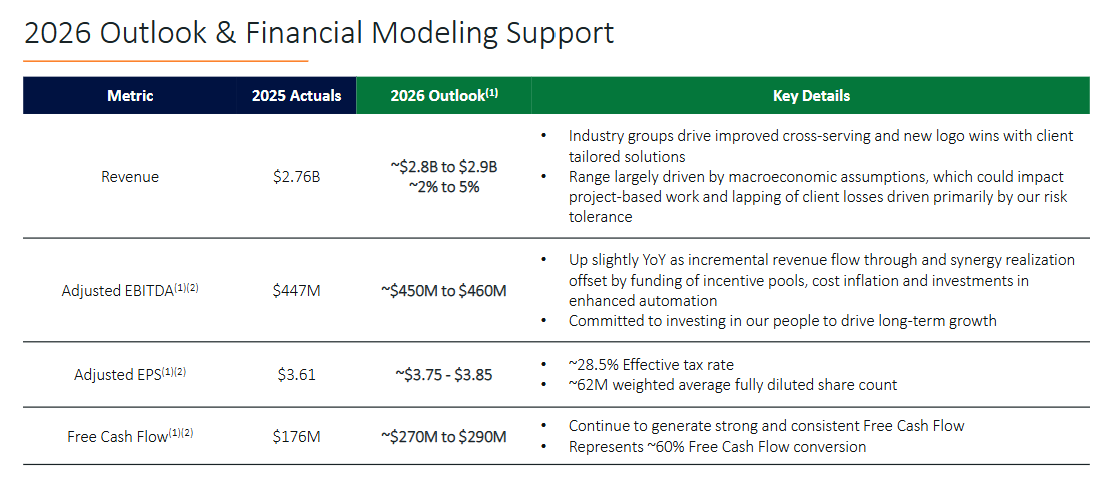

2026 guidance calls for modest revenue growth (2-5%) and earnings growth (4-7%). Both of which are way below long-run growth rates; although historic performance included plenty of inorganic growth.

Unpacking this outlook a bit further…

Revenue growth does not include any acquisitions, and with leverage >3x, plus a desire for more buybacks, it seems unlikely CBIZ will pursue any acquisitions in 2026. EBITDA growth comes from revenue growth and merger synergies offset by higher planned wages and incentive comp.

To recap: growth is slowing and leverage is 1-2x higher than “normal” levels.

So where does the company go from here?

We have some Soros-level reflexivity kicking in here…

Management was already excited by the prospects of share repurchases (they spent $160m in 2025 at an average share price of $66).

Shares are now down 56% from the average buyback price in 2025 and management is signaling they’re willing to extend their 2-2.5x leverage target in favor of buybacks. Here are their comments from the 3Q25 earnings call:

Given the opportunity we've had to allocate capital to share repurchases in 2025, the timing for achieving this range may shift to 2027. At our current valuation, we believe share repurchases are accretive.

The stock is trading at 6.5x FCF and 7.7x low end EPS guide. Way below long-run average multiples. Could we see a flurry of buyback activity here?

At this price, they could easily engineer 15% EPS growth in 2026.

Low end guide of $3.75 per share equates to $233m net income at a share count guide of 62m. If they can get shares down to 56m = $4.15 EPS (15% higher than the $3.61 put up in 2025).

That growth would require a 6m share buyback. At $30, they’ll need to spend $180m. At $33, they’ll need to spend $200m. Those levels still allow for a 0.25x reduction in leverage too.

Hmm…

What about the AI risks?

Things are moving fast and it’s hard to handicap what will happen to these consulting businesses (see RGP for an example of the downside scenario).

CBIZ clients are mostly medium-sized businesses needing professional guidance. Thinking of my own $30m company (perhaps a reasonable proxy for a CBIZ customer?) and with our complexity, there’s little (if any) chance I’d bring this work in house even with the advances in AI.

On the other hand, lower skill “people services” are getting killed right now. Again, look at the fundamentals for RGP to get a sense of what’s happening. The risks probably vary by service line (data entry + low level advisory as most vulnerable while compliance, payroll, audit/tax as least vulnerable).

What could shares be worth?

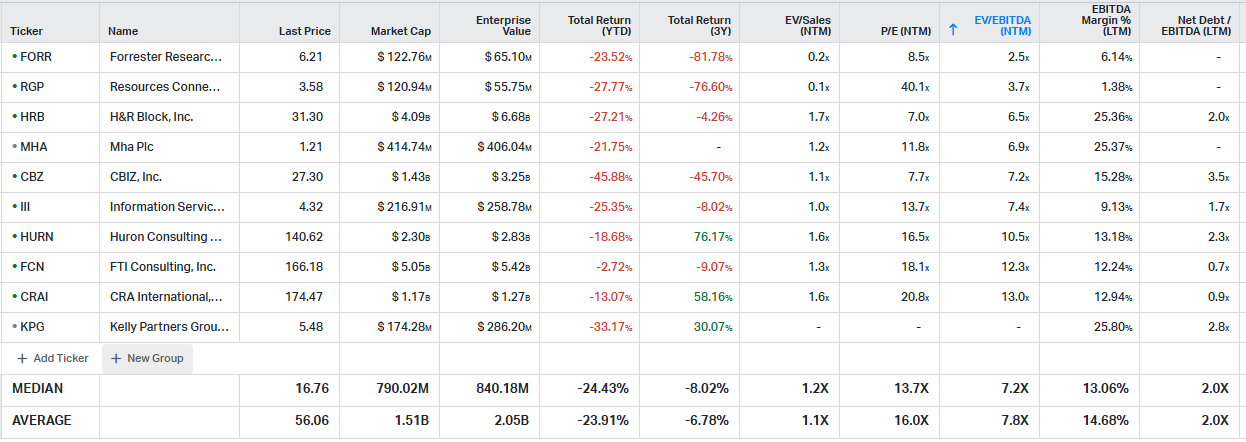

Peers are trading at a wide range of multiples from 7-14x earnings and 6-8x EBITDA.

From ~2017 through mid-2025, CBIZ was consistently trading between 17-20x earnings, which is a far cry from the current 7-8x earnings multiple. Here are some scenarios:

Downside: HRB is trading at 6-7x earnings. If CBIZ sees margin compression / declining earnings ($3.50), then at 6x earnings = $21 per share or 28% downside. Obviously this could get a lot cheaper in a fear-driven sell-off.

Upside: British competitor MHA trades at 11.8x earnings. At 11.8x my EPS estimate of $4.15 = $49 per share or 69% upside. Again, upside could be a lot more if we (ever) see a return to normal trading ranges.

This is nearly 2.5x risk/reward at the current price ($29). Hmm…

Summing it up…

There’s a clear dislocation in shares today and perhaps it comes down to whether you believe that dislocation is a result of: (1) AI threat to this business model; or (2) the fundamentals and shifting story.

I spend a lot of time in the “main street” SMB world ($2-30m revenue businesses) and believe the risks from (1) are low for the foreseeable future.

This leaves us with the fundamentals which seems like a plausible reason for a massive sell-off. If investors were expecting a low-leverage 15%+ EPS grower and now have a high-leverage slow-grower, that will cause some turnover!

Fortunately, the recurring revenue + cash flow profile is so strong that deleveraging could/should be relatively fast. But it sounds like management has a preference for more buybacks and pushing out the deleverage target.

I may take a position here with a 2-4 quarter time horizon to see if management can bring this back to a 15-20% EPS growth story. I’ll need more time/evidence to determine the AI risk potential.

P.S. a sizeable insider buy would be an excellent “tell” for this name, but we haven’t seen much/any useful insider activity so far in 2026

Disclosure: I don’t own shares of CBZ today, but will likely start a position within the next week.

Resources:

Is your table correct? It shows shares outstanding going from 49.2M in 2025 to 62M in 2026? This seems to contradict the story of share buybacks?

"Shares are now down 56% from the average buyback price in 2025 and management is signaling they’re willing to extend their 2-2.5x leverage target in favor of buybacks. Here are their comments from the 3Q25 earnings call:"