Quick Value #322 - FuboTV (FUBO)

Messy transaction / ownership structure plus a sudden management change

Today’s post:

Recently closed merger between Fubo and Hulu Live vMVPD platforms

Shares trading at 4.2x 2028 EBITDA target with good visibility

Abrupt CEO change brings in former head of Disney+

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: (1) company background; (2) why the idea is interesting; and (3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

06/29/26 — Somnigroup’s vertical integration acquisition spree

06/23/26 — Guide to GoodCo / BadCo situations (a look at Tripadvisor) ($)

06/15/26 — Campbell’s is another beaten down staple

Quick Value

FuboTV Inc (FUBO)

Ticker: FUBO

Price: $10

Shares: 110m

Market cap: $1.1bn

Valuation: 4.2x 2028 EBITDA target ($300m)

Theme: M&A

It’s easy to assume that every stock owns 100% of their core operating business, but this isn’t always the case (“non-controlling interest” is easily one of the most confusing and overlooked corners of the balance sheet).

A few quirky ownership situations hit my watchlist recently (FUBO, MKTW, HGTY, etc.) and some of them might be actionable…

TL;DR:

Fubo + Hulu combination gives this business much needed scale as a distributor and leaves Disney with 70% ownership

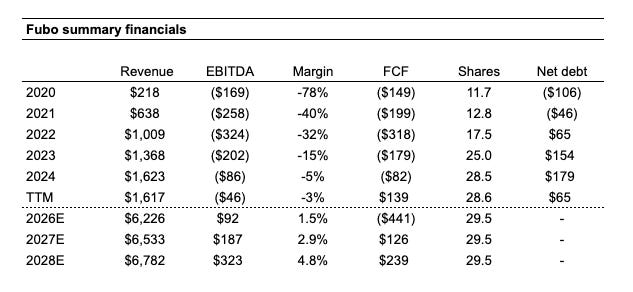

Original $550m 2028 EBITDA target was reset to $300m after programming cost synergies proved slower than expected.

More than half of expected EBITDA improvement is tied to a contractual wholesale arrangement (i.e. high visibility to earnings growth).

At $10 per share, market value is ~$1.1 billion and enterprise value is ~$1.25 billion = 4.2× the 2028 EBITDA target (it’s cheap).

Background

Fubo is a sports-focused virtual Pay TV distributor (vMVPD).

Some history:

2015-2019 — Company was founded as a low cost streaming option for soccer matches; with backing from major content networks they expanded to compete with cable and other vMVPDs (Sling TV, etc.). Revenue grew to $133m in 2019 with $172m in operating losses.

2020-2021 — Completed reverse merger and public offering (~$180m raised) in October 2020, shares jumped from $10 to $50+ and the content networks sold their stakes. Revenue grew to $638m in 2021 and operating losses expanded to $328m. Shares ended 2021 at a split-adjusted $186 (from $120).

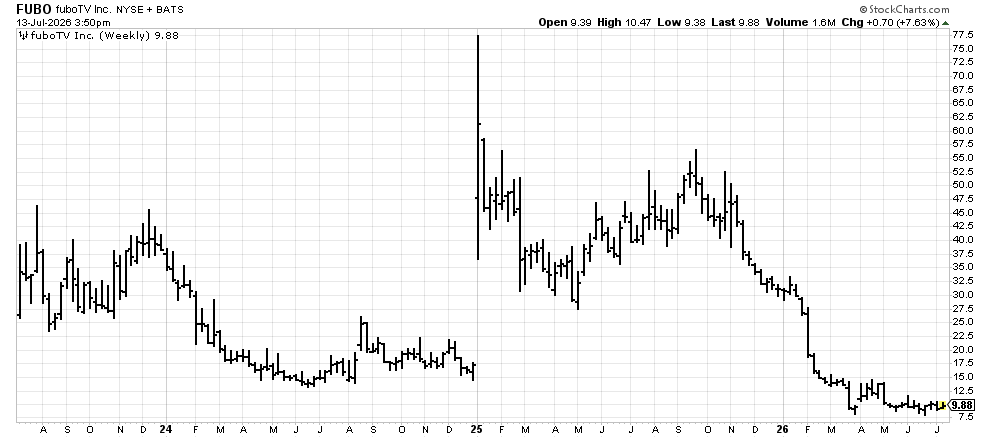

2022-2024 — Revenue grew from $638m in 2021 to $1.6bn in 2024 and subscriber revenues covered programming costs for the first time in company history. Disney, Fox, and Warner launched a competing product called Venu Sports and Fubo responded with an antitrust lawsuit. Shares went from $186 to $17 (down 90%) as losses mounted.

2025 — Announced a “merger” with Disney’s Hulu + Live TV service (i.e. their vMVPD offering, not the streaming app) in January 2025 and settlement of the Venu Sports lawsuit. Deal closed in October 2025. Shares went from $17 to $31.

2026 — Completed 1-for-12 reverse split. Reset long-term (2028) financial targets tied to the merger. Replaced CEO with Disney+ streaming executive. Shares down 70% YTD (from $31 to $9).

So let’s get this straight…

Several major content networks including Disney, AMC, Comcast, Viacom, and Discovery owned 45%+ of Fubo at the time of the IPO in 2020.

Because they had this equity/ownership, they were incentivized to see Fubo do well, and perhaps that influenced negotiations for content carriage deals.

Shares skyrocketed after the IPO and they all sold for a quick gain (Disney reported a $186m gain on their sale).

With no equity/ownership incentive, carriage negotiations got a bit more “real.”

Fubo struggled to generate consistent gross margins and adding to the pain, those content networks banded together to launch a competing service called Venu Sports in 2024, to which Fubo quickly countered with an antitrust lawsuit.

Hmm…

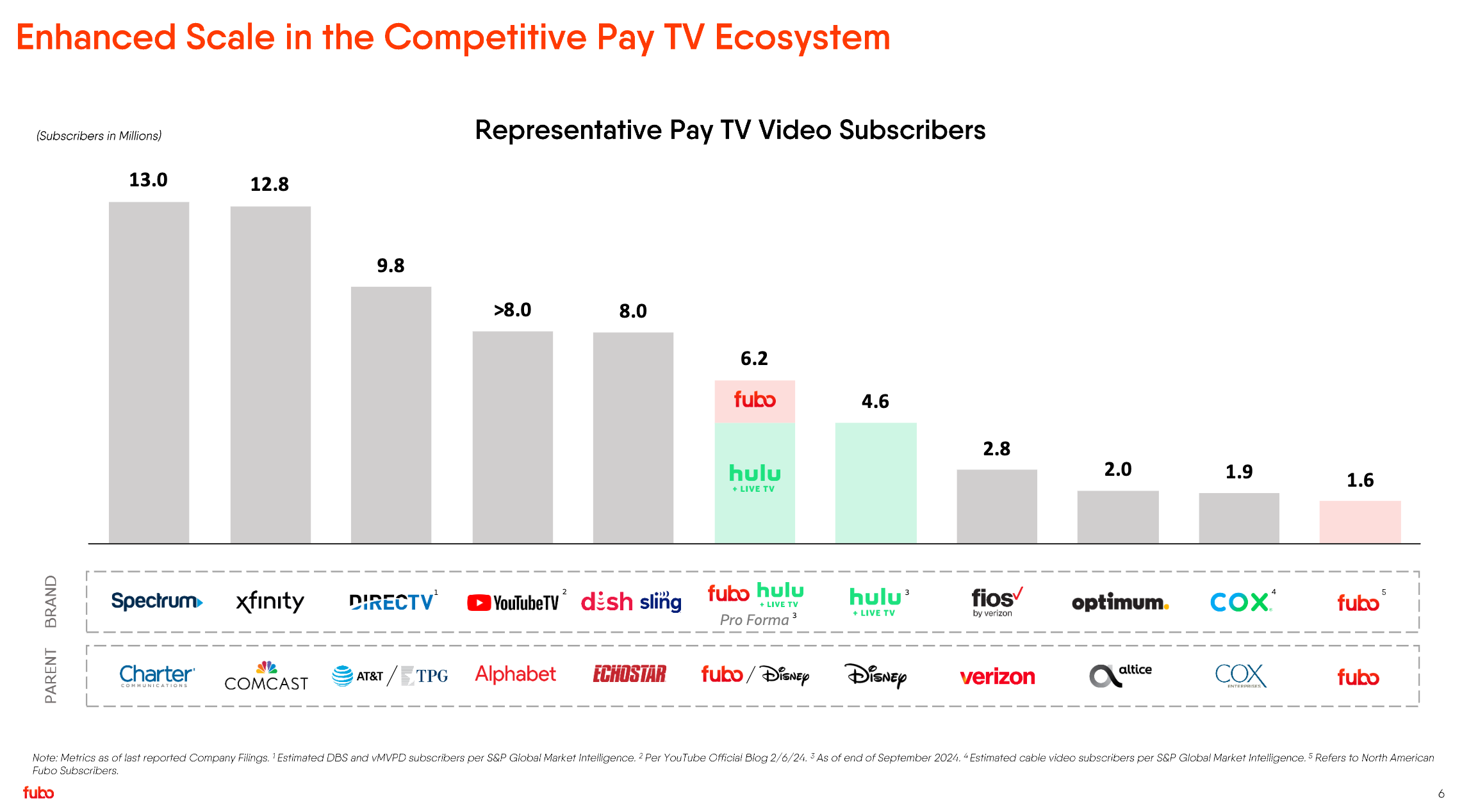

The Pay TV and vMVPD industry

Fubo is a virtual multichannel video programming distributor, or vMVPD as they’re known. Unlike a cable company with an installation process and set top boxes, these are virtual distributors. They pay content providers to carry their channels and wrap them in an online interface.

YouTubeTV is the largest player with 9-10m subscribers (up from an estimated 8m in the chart below).1

Most vMVPD offerings are priced attractively compared to cable packages, especially when considering additional fees for DVR, boxes, etc.

Historically, total vMVPD subscribers are growing while cable subscribers are declining with the overall industry / subscriber count declining.

Why it’s interesting…

This is a fascinating corporate version of “stockholm syndrome.”

Fubo was growing quickly and took capital from industry peers (friends) who then cashed out and became enemies through content costs and competing offerings. Now, the biggest “frenemy” (Disney) is a 70% owner as part of a settled lawsuit.

A few things make it compelling here:

The lawsuit settlement & carriage cost reset make this a viable business model and gives the company better visibility into future earnings.

The Hulu / Fubo transaction structure was very complicated. It’s likely most investors don’t understand the math, and data providers aren’t feeding the right capital structure information.

Shares were clobbered after resetting initial Hulu merger targets in early 2026.

In July 2026, they announced that co-founder and CEO David Gandler was being replaced immediately by Alisa Bowen, the former head of Disney+ / streaming at Disney.

Let’s start by looking at the fundamentals…

Some notes:

Leading up to (and shortly after) the IPO, revenue was on a solid growth trajectory at a 65% CAGR

They spent boatloads on marketing and content which helped grow the subscriber base from ~550k in 2020 to ~1.6m by the end of 2025, but cumulative losses were more than $1bn during this stretch

Fubo issued debt ($380m) and equity ($880m) to cover those operating losses

Growth tapered off in 2025 and margins started improving (the cash inflow was tied to the lawsuit settlement)

What about this lawsuit?

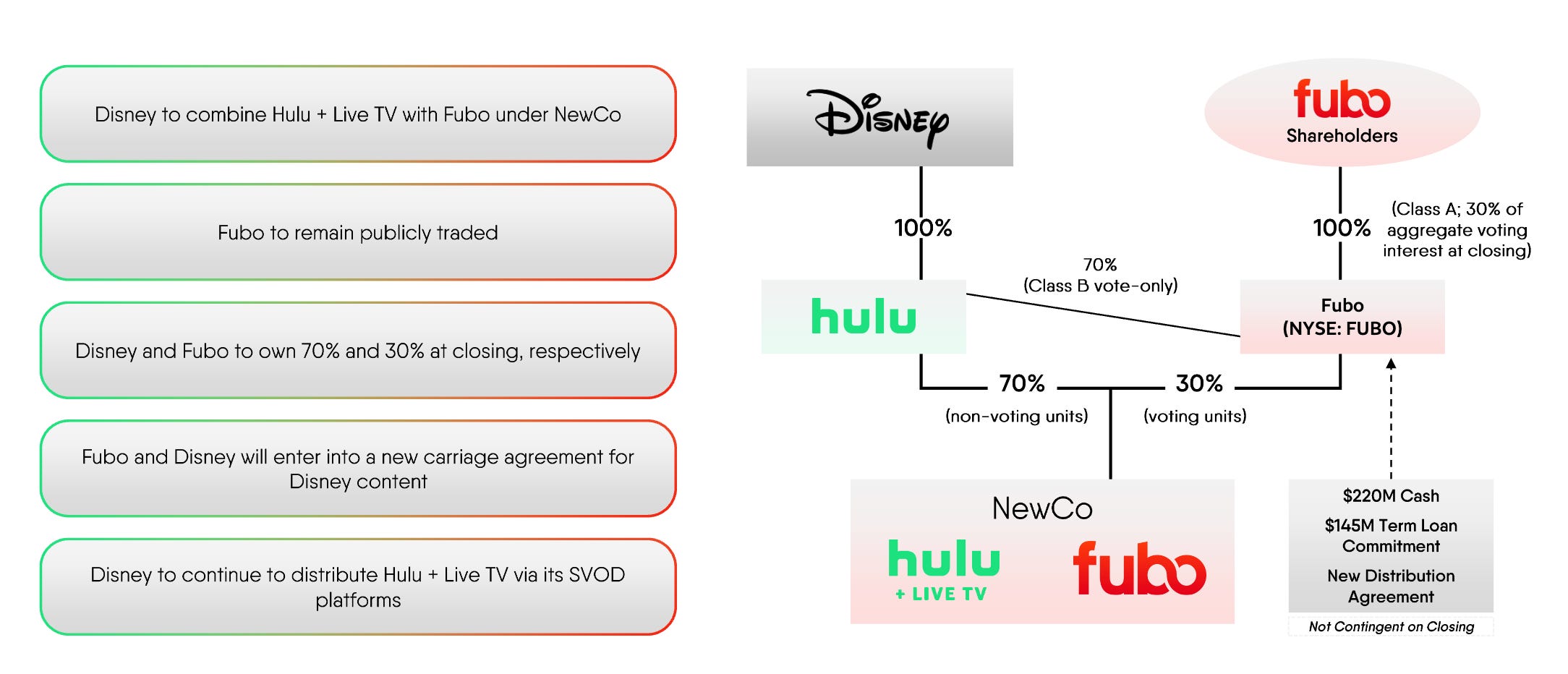

In January 2025, Fubo announced a settlement with Disney, Fox, and Warner Bros which resulted in: (1) a $220m cash payment to Fubo; (2) a $145m term loan from Disney; and (3) the combination of Disney’s Hulu Live business with Fubo to create NewCo.

The cash settlement provided a nice balance sheet recap, but more importantly was the “commercial services agreement” with Disney which reimburses NewCo for 95% of Hulu Live’s carriage expenses in 2025-2026 and escalates to a 99% reimbursement by 2028.

This commercial services agreement will significantly improve Fubo’s unit economics going forward. Here’s what management had to say on the 2Q26 earnings call about it (emphasis added):

This contractual step-up provides strong visibility into our expected earnings profile and adjusted EBITDA expansion. Furthermore, the company captures advertising revenue from both the Fubo and Hulu + Live TV businesses. Together, these elements reinforce our expectations regarding the long-term earnings power of our combined entity.

the largest component of the adjusted EBITDA improvement will come from the contractual increase in the wholesale fee from 95% to 99%

What about the Hulu merger?

As a reminder, this was a combination of 2 vMVPD platforms and does not include the Hulu streaming service/app.

Operationally, Fubo and Hulu Live will operate as 2 separate brands and platforms. Fubo pitches itself as being sports-focused and Hulu Live is more of a generic competitor to YouTube TV. Any synergies between these brands are expected to come on the backend (marketing, admin, programming cost negotiations, etc.).

After closing, Disney owns 70% of Fubo via Class B voting shares and 70% of the economics via NewCo.

It was an up-C transaction, so technically Disney owns 70% of the operating subsidiary and the stake is recorded as a non-controlling interest on the balance sheet (i.e. it’s messy).

What’s the pro forma picture of Hulu + Fubo?

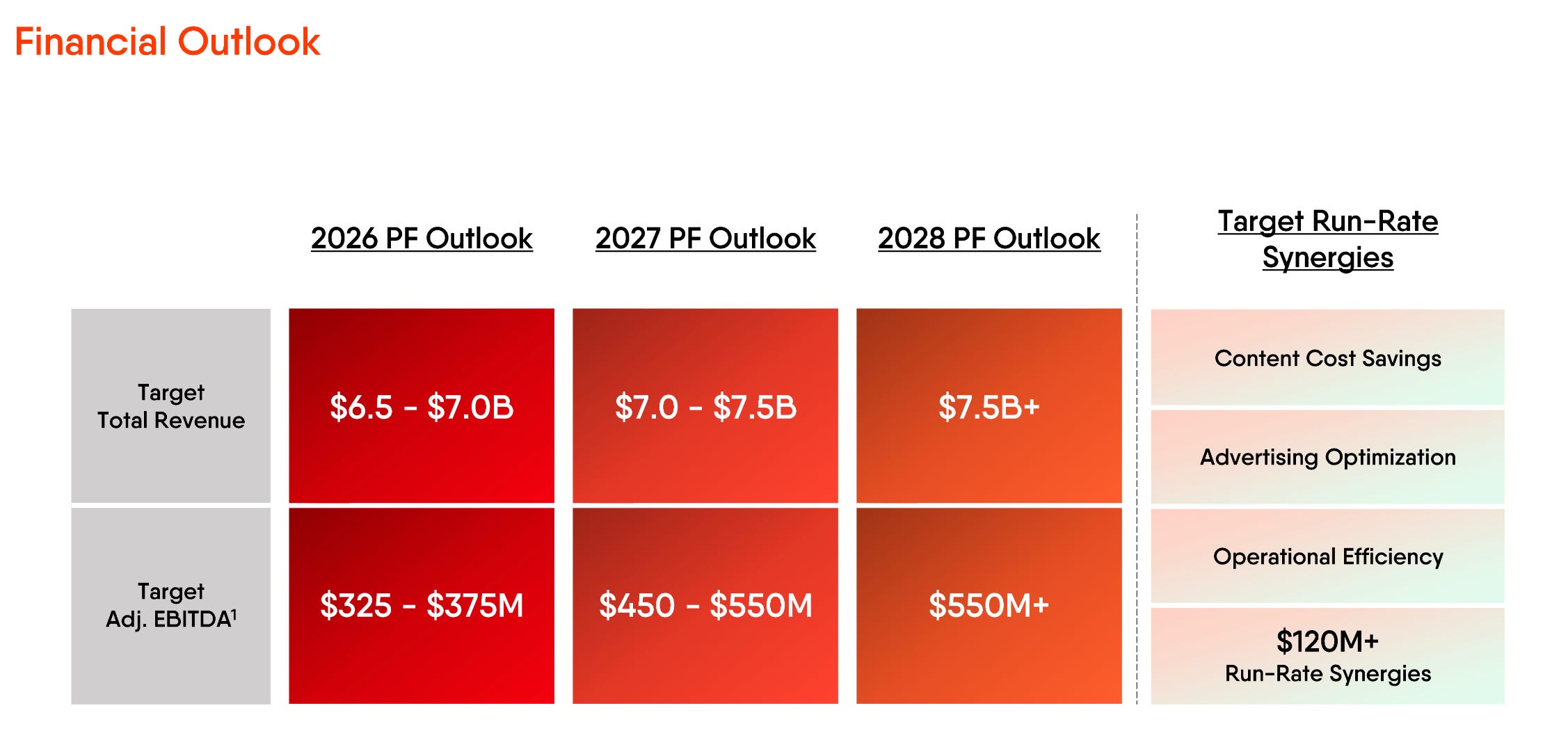

At the time of the deal announcement, Fubo was touting $550m EBITDA by 2028, in part from better programming costs (makes sense, distribution is a scale game).

Shortly after the deal closed (February 2026), management foreshadowed a major reset in these long-term targets… Turns out, Fubo and Hulu Live have separate programming contracts and content providers weren’t willing to negotiate them collectively:

Translation: it’s going to take much longer for programming cost synergies to bear fruit because these are multi-year deals.

A few months later in April 2026, management laid out new (much lower) financial targets in a shareholder letter:

Fiscal 2026 Pro Forma Adjusted EBITDA guidance of $80-$100 million

Fiscal 2028 Adjusted EBITDA target of at least $300 million

Positive Free Cash Flow expected in Fiscal 2027 and Fiscal 2028 under current operating plan

I believe this financial “reset” is a major reason behind the YTD stock performance AND the recent CEO turnover.

The good news is more than half of the incremental EBITDA from 2026 to 2028 comes from the Disney/Hulu commercial services agreement which is contractual. So you have good visibility into the potentially “kitchen sink” $300m 2028 target (unless the wheels fall off elsewhere in the business).

What could shares be worth?

There are 29.4m Class A shares (publicly traded Fubo) and 79m Class B shares held by Hulu = ~110m shares outstanding (assuming some modest dilution from here). At $10 = $1.1bn market cap. Net debt is roughly $150m at 2Q26 for a $1.25bn enterprise value.

Note: The Class B shares are vote-only, but each one is paired with NewCo LLC units that can be exchanged into Class A shares. I’m using ~110m shares when valuing 100% of the consolidated business. If you use this share count and add the $1.84bn non-controlling interest to EV, then you’re double-counting Disney’s 70% economic ownership.

Comps…

It would be an understatement to say the media landscape is undergoing significant change. Media players trade all over the place depending on their business models:

Let’s assume the 5-7x EBITDA range is the right comp set for this business:

Upside — Giving them full credit for the $300m EBITDA target at a 7x multiple = $2.1bn enterprise value. I’ll assume net debt remains at $150m (i.e. 2026 outflows and 2027 inflows offset each other) = $18 per share or 80% upside.

Downside — Taking the 2027 EBITDA estimate ($187m) at 5x = $935m EV. In this scenario, I’ll assume heavy cash burn leaving net debt equal to gross debt ($375m). That works out to a $560m equity value or $5 per share (50% downside).

This works out to a 1.6x upside/downside ratio.

At that level of EBITDA, cash flow is likely substantial. Capex is running $12-15m annually, interest ~$12m annually, and cash taxes should be minimal with NOLs and depreciation. Back of the napkin math gets me to $240m or so in FCF or $2+ per share.

Not bad on a $10 stock.

Summing it up…

At this point, we’ve hammered home the reasons this stock is getting absolutely annihilated over the past few years.

It’s turning into a bit of a special situation now, with a complicated backstory, complex transaction, and a forced management change by Disney.

Not only is this a beaten down stock (although a bit of a falling knife) it’s also a management change story with an external hire and the first non-founder leader.

Some open questions for me, which could be interpreted as the potential risks in this situation:

Was the 2028 guidance reset deep enough?

What happens after the Hulu carriage deal expires? Will this lead to another EBITDA reset in 2030/beyond?

What is Disney’s plan here? Is there a possibility for a takeunder?

Can this business be successful running 2 separate vMVPD brands long-term? Or will they need to consolidate into a single brand eventually (likely Hulu)?

I’m planning to sit with this one for a while. Why?

The transaction structure is complicated and I don’t think investors will give them full credit until that becomes clearer or gets resolved.

Also, Disney is clearly in the driver’s seat (see the CEO change as a reference) which could mean they build some success and then you get taken out prematurely below fair value.

It’s an interesting “optionality” bet where this could be a 2-3 bagger if things play out. Will need to do some more work here. Thoughts or comments welcomed.

Disclosure: no position in Fubo.

Resources: