Quick Value #318 - Campbell's (CPB)

Beaten down CPG stock at 10-11x earnings and ~7% dividend yield

Today’s post:

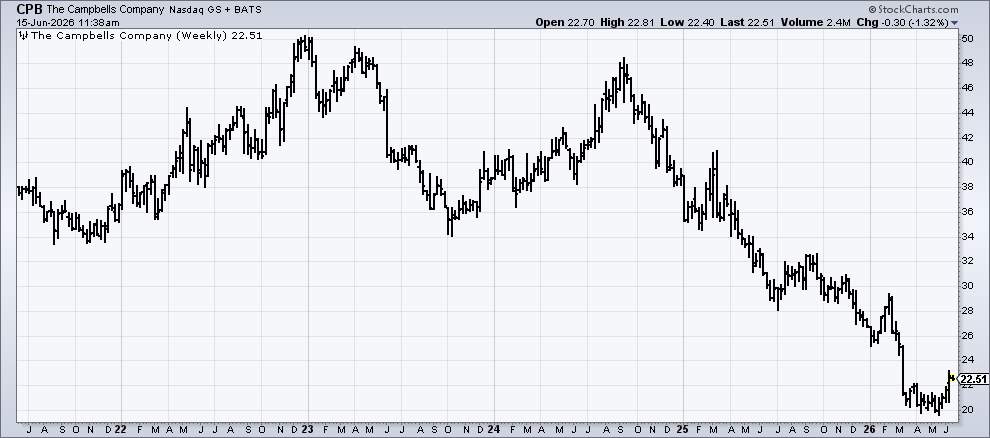

Shares down 20% YTD and 30% over 1-year (beaten down category)

Valuation reset from historic 15-16x P/E to current 10-11x P/E

Navigating high leverage (4x) from recent acquisition

Cash flow constrained from high dividend (7% yield)

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: (1) company background; (2) why the idea is interesting; and (3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

06/01/26 — All-stock cabinet merger MasterBrand

05/31/26 — A case study of a stub business investment

05/26/26 — My 4 favorite special sits right now ($)

05/18/26 — Former compounder Zoetis looks beaten down

05/11/26 — Sale + spin at Enviri ($)

Quick Value

The Campbell’s Company (CPB)

Ticker: CPB

Price: $23

Shares: 301m

Market cap: $6.9bn

Valuation: 11.5x FY27 EPS ($2.00)

Theme: beaten down

Let’s continue on the review path of beaten down staples & CPG stocks. Previous write-ups:

Background

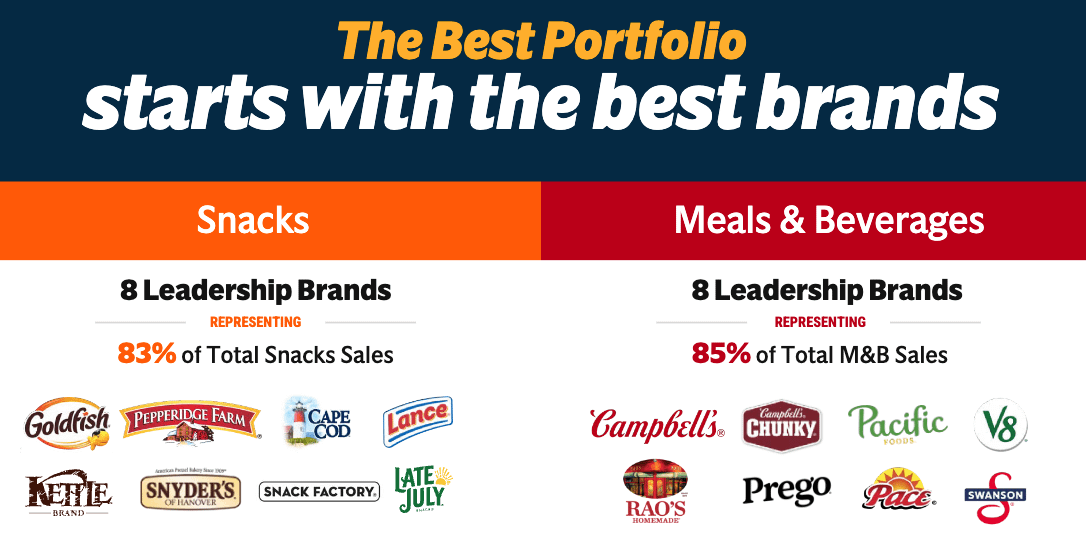

Campbell’s is a packaged foods business with 2 segments:

Meals & beverages ($6bn FY25 sales) — soups, simple meals, and beverages sold in retail & foodservice settings

Snacks ($4.2bn FY25 sales) — cookies, crackers, bakery and frozen products

Let’s add some historical context here:

2016-2018 — Period of modest revenue decline, low leverage, and modest buybacks. Culminated in 2018 acquisition of Snyder’s-Lance for ~$6bn. It was a rich valuation (20x EBITDA before synergies), brought a host of snack brands (Snyders, Kettle, Pop-Secret, etc.), and reduced soup exposure from ~35% to 27%. Shares fell from ~$50 to $35.

2019-2020 — Hired Mark Clouse (former head of Pinnacle Foods) as CEO. Divested $3bn in various brands/businesses and repaid $3.7bn acquisition debt to delever from ~5x to ~3x. Shares from $35 to $47.

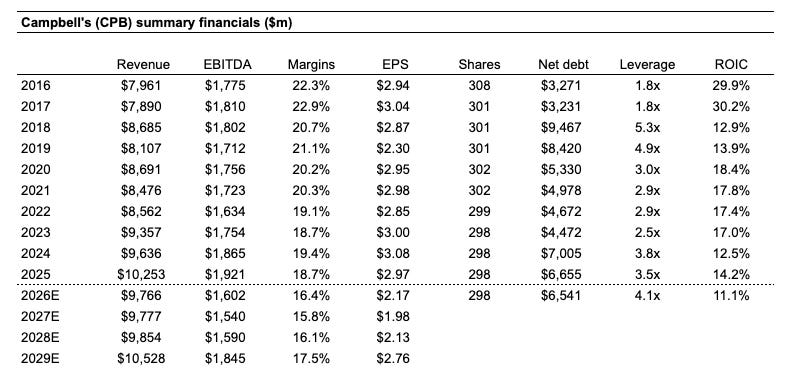

2021-2024 — Post-pandemic rebound. Falling volumes but huge price increases took revenue from $8.5bn to $9.6bn and EPS from $2.98 to $3.08. Acquired Sovos Brands (Rao’s) in 2023 for $2.7bn (20x EBITDA) which re-levered the company. Shares from $47 to $39.

2025-2026 — Mick Beekhuizen named CEO (former CFO and head of Meals & Beverage division). Tariffs, inflation, and industry volumes killing fundamentals. EPS from $3.08 to a guided $2.15-2.25 in 2026 (down 23-26% YoY). Shares from $39 to $23.

Why it’s interesting…

I would categorize this stock in the beaten down category.

CPB was trading as high as $50 as recently as late 2024. At $23, shares are down >50% on the back of an earnings dive + valuation reset. Shares are nearing a 7% dividend yield and 10x earnings today.

The beaten down category is an excellent hunting ground for new ideas, but it’s rarely a good reason to buy a stock by itself.

Maybe there’s something at CPB which could make it compelling?

A quick review of the fundamentals

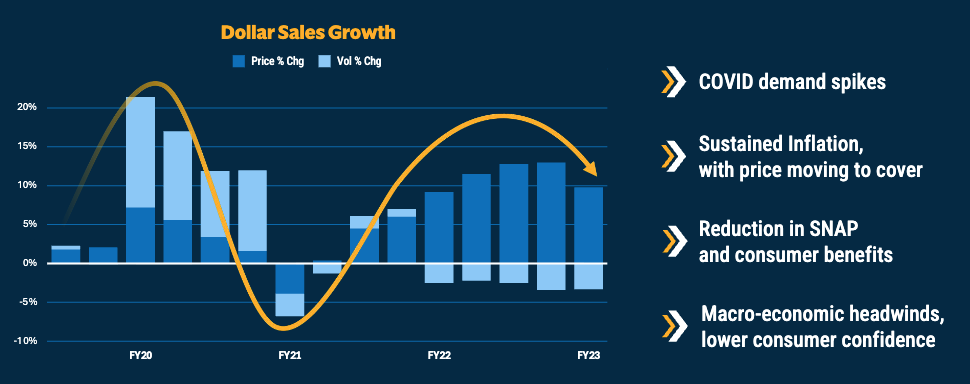

Like other CPG companies: price and volume have been erratic since the pandemic.

Many companies took significant price hikes coming out of the pandemic, essentially pulling forward several years of price increases in a short window. This is fueling a rapid trade down to cheaper generic and private label brands. CPB is “investing” in beefed up marketing spend as a result.

Then you have tariff and inflation eating into historically very high margins (>20% pre-covid EBITDA margins).

There’s your industry backdrop for basically every CPG stock right now.

All of this is leading to EBITDA margins 400-600bps lower than “normal” (history) and increased pressure on cash flow at a time where leverage is high. Ouch.

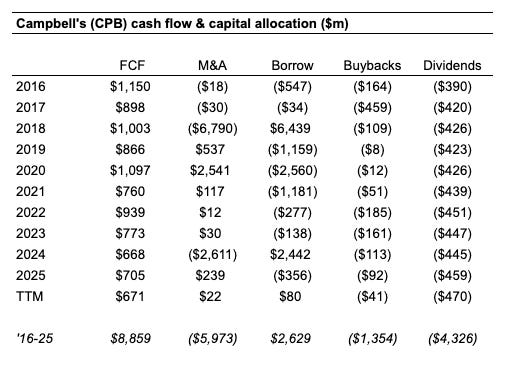

Adding to the fun, CPB has been a terrible capital allocator — zero change in EPS from 2016-2025 despite a net $6bn investment in M&A, before collapsing to an expected $2.15-2.25 in 2026. Ouch. Gotta love that dividend though!

In 2025, CPB produced a combined $944m from FCF ($705m) and divestitures ($239m) while spending $907m on repaying debt ($356m), buybacks ($92m), and dividends ($459m).

Barring any major divestitures or portfolio shake-up, this is probably what a normal year will look like for a while…

So where do things go from here?

We are a little over a year into a new CEO (Mick Beekhuizen) who was dealt a levered business with revenue and margin headwinds.

Capital allocation is squarely focused on delevering right now with buybacks and M&A “off the table.”

Management is focused on maintaining an investment grade balance sheet, keeping the dividend flat, wringing out working capital, and only the highest priority capex projects.

There’s a good chance we’ll see further divestitures from here… CEO commentary from the 3Q26 earnings call:

…there is a tail of SKUs in certain brands. It's not a lot of sales. However, we believe that the reduction of that tail could actually allow for further simplification and as a result, improve the overall operations and improve our overall network.

How bad is the leverage situation?

As of 3Q26 (5/31/26), net debt is $6.6bn with $1.64bn trailing EBITDA (3Q26 earnings presentation) = 4x leverage. They want to get to the “low 3s.”

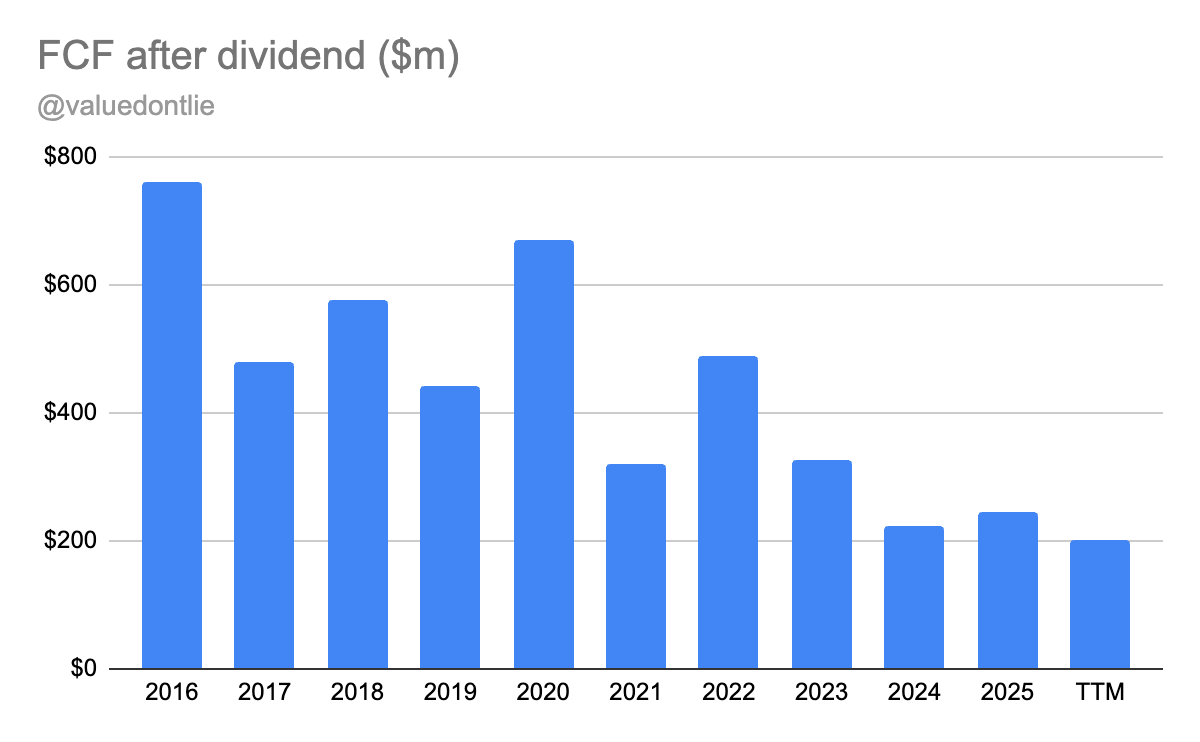

There is roughly $200m of FCF after the dividend available for repaying that $6.6bn debt; translation: it’s going to take quite some time without a rebound here… This is what a constrained business looks like.

Let’s assume the business stabilizes at $1.6bn annual EBITDA:

At $200m annual debt repay = 6.6 years to hit 3.3x leverage.

At $300m annual debt repay = 4.4 years to hit 3.3x leverage

What’s the outlook and what are shares worth?

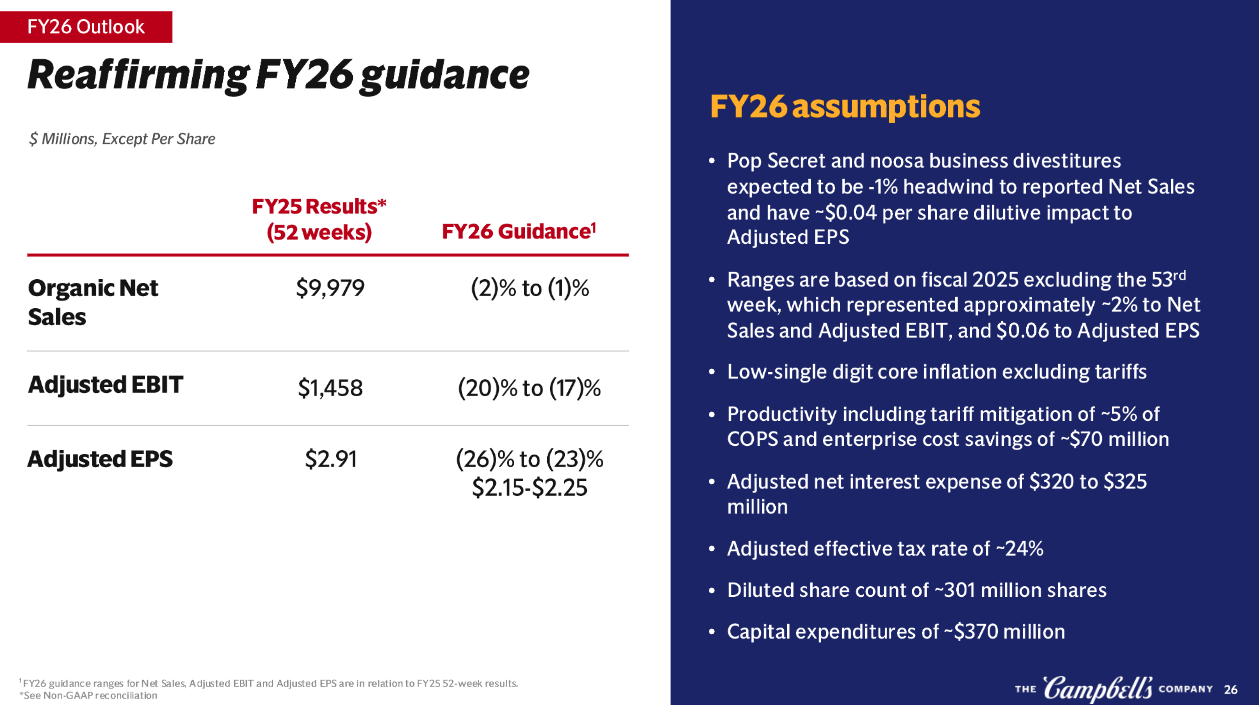

CPB has a 7/31 yearend and expects 2026 revenue to fall 1-2% and EPS to fall 23-26%:

On the bright side, it looks like earnings are stabilizing on a quarterly basis.

After 2 consecutive quarters of $0.50 EPS, run-rate EPS looks closer to $2 than $2.15-2.25, which is where sell-side estimates are sitting for FY27 (ending 7/31/27).

Perhaps this could be a bottom?

At $23, this puts shares at ~11.5x FY27 earnings.

From a valuation standpoint, peers are trading at 10-20x earnings with a cluster at 10-12x and another cluster at 15-16x. Leverage is the key factor separating these 2 groups and CPB is at the higher end of the leverage range.

Upside — Earnings recover to $2.25-2.30 per share and the stock trades back to its 5-year median P/E of 14.5x = $33 per share (+44% upside).

Downside — Earnings continue to fall ($1.95) and the dividend is reduced to repay debt. At 8x earnings = $16 per share (-30% downside).

These are fast-and-loose calculations, but it’s a modest 1.5x upside/downside ratio here with an extremely difficult dividend situation to handicap (I believe they need to reduce it in order to hit leverage goals within 2-3 years).

An interesting, albeit super boring, scenario could be a very slow debt repay timeframe of 5-10 years at $200m per year based on current cash flows.

Let’s say that amount “accrues” to equity holders each year = $0.60-0.70/share. Tack that onto a 7% dividend yield and the slow-and-steady deleverage path maybe nets a 10%+ IRR over a decade. Bonus if earnings stabilize, then turn a corner a few years in.

Summing it up…

These are solid brands in durable product categories which will absolutely be around 10+ years from now with zero doubt.

The question is whether shares are cheap enough to bridge a gap between today’s financial strain to a more “flexible” tomorrow. Meaning: a company with low enough leverage to deploy capital in whatever means desired.

My take — Shares aren’t cheap enough yet. Sure, these are durable brands; but the headwinds are still around and there’s no hard catalyst to get things going. I see a few paths here:

Super boring 10%ish IRR deleveraging story (assuming earnings stabilize)

Dividend reduced or eliminated to speed up deleveraging which kills the stock price (I’d get interested after this event)

Dramatic portfolio simplification / divestiture announcement (again, I’d get interested with this announcement)

Until then, I’ll keep this one on the watchlist.

Let me know your thoughts.

Disclosure: no position in CPB

Resources:

I have followed this for quite some time. I thought it was a buy at $29. Stopped out at 26.50….. still on my watch list. 😁