Quick Value #313 - Magnum Ice Cream (MICC)

Ice cream spin-off 5 months in: what's the story and what's it worth?

Today’s post:

Recently spun off ice cream segment from Unilever

Shares flat since Dec 2025 spin and down 25% from Feb 2026 peak

Stock is trading at 13x NTM earnings and 8x EBITDA with 2.4x leverage

Turnaround plan targeting major growth in EBITDA & FCF over 2-3 years

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: 1) company background; 2) why the idea is interesting; and 3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

04/21/26 — Guide to analyzing “asset plays”

04/13/26 — Beaten down CPG stock Nomad Foods ($)

04/06/26 — Upcoming spin-off at Middleby ($)

03/23/26 — A look at GameStop fundamentals

03/16/26 — Green Dot upcoming sale + spin ($)

03/09/26 — CBIZ growth to value transition

03/02/26 — Ziff Davis sum of the parts ($)

Quick Value

Magnum Ice Cream Company (MICC)

Ticker: MICC

Price: $15

Shares: 615.6m

Market cap: $9.25bn

Valuation: 13x P/E

Theme: spin-offContinuing my review of beaten down staples & CPG stocks, today I’m looking at recently spun-off Magnum Ice Cream Company (MICC).

Note: the company released Q1 results in the midst of my writing and (naturally) the stock was up big… I have not yet incorporated those results into this.

Back in Dec 2025 (at the time of the spin), I took a very brief look and didn’t like the combination of increasing costs/investments and no short-term guidance.

Background

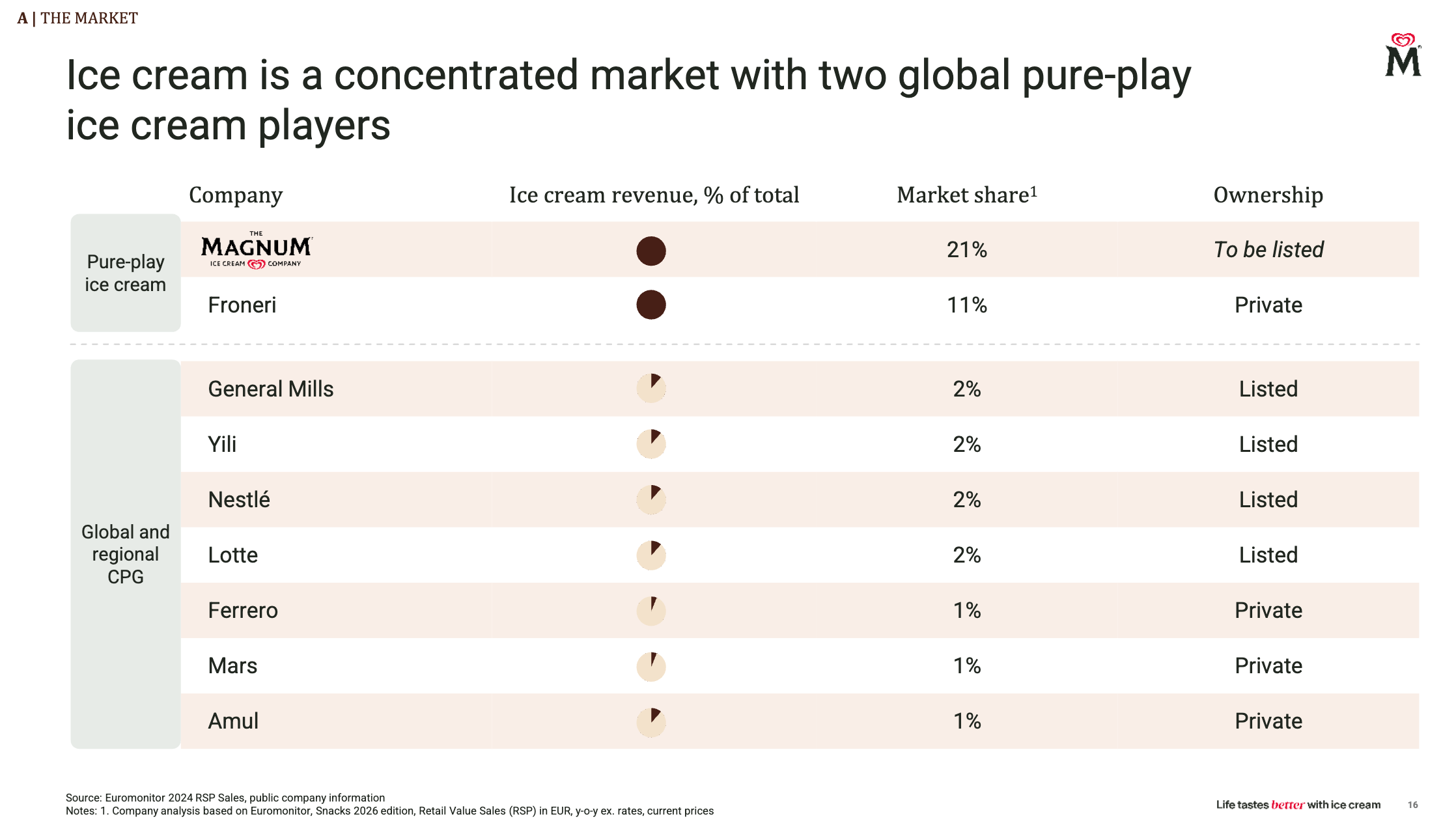

Magnum is the recent (Dec 2025) spin-off of Unilever’s ice cream division with brands like Magnum, Ben & Jerry’s, Klondike, Yasso, Breyer’s, and Popsicle. It’s the global industry leader with 21% market share and the only pure-play publicly-traded ice cream company.

Unilever originally announced the spin March 2024 and pitched it as having a “very different operating model” compared to their other businesses.

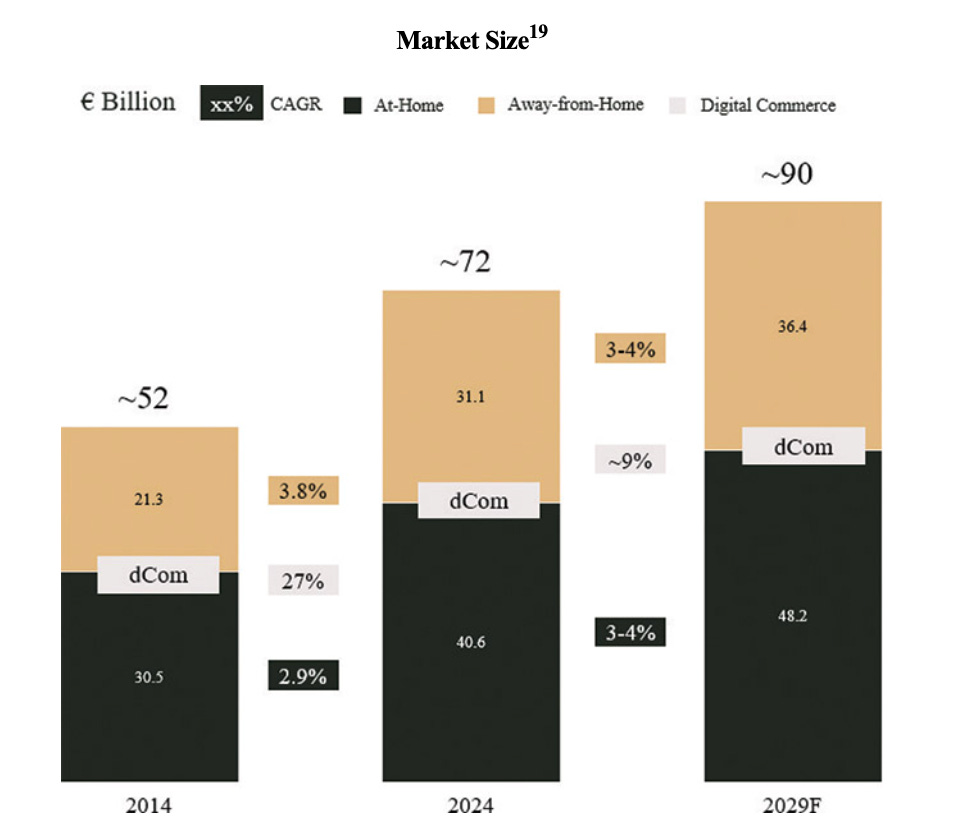

Ice cream is a €75bn segment within the €475bn global snacking industry and growing 3-4% annually.

MICC is the largest player with about 21% global retail market share and four of the five largest global ice cream brands. Froneri is the #2 player with 11% market share as a privately-held 50-50 joint venture with Nestle. And the rest of the industry is tucked inside larger CPG businesses (Häagen-Dazs owned by General Mills, etc.).

There are 2 markets within the ice cream industry: (1) at-home (think: buying a pint at the grocery store); and (2) away-from-home (buying from a vending machine at the mall).

The away-from-home business seems like the crown jewel here and may have a legit moat to it…

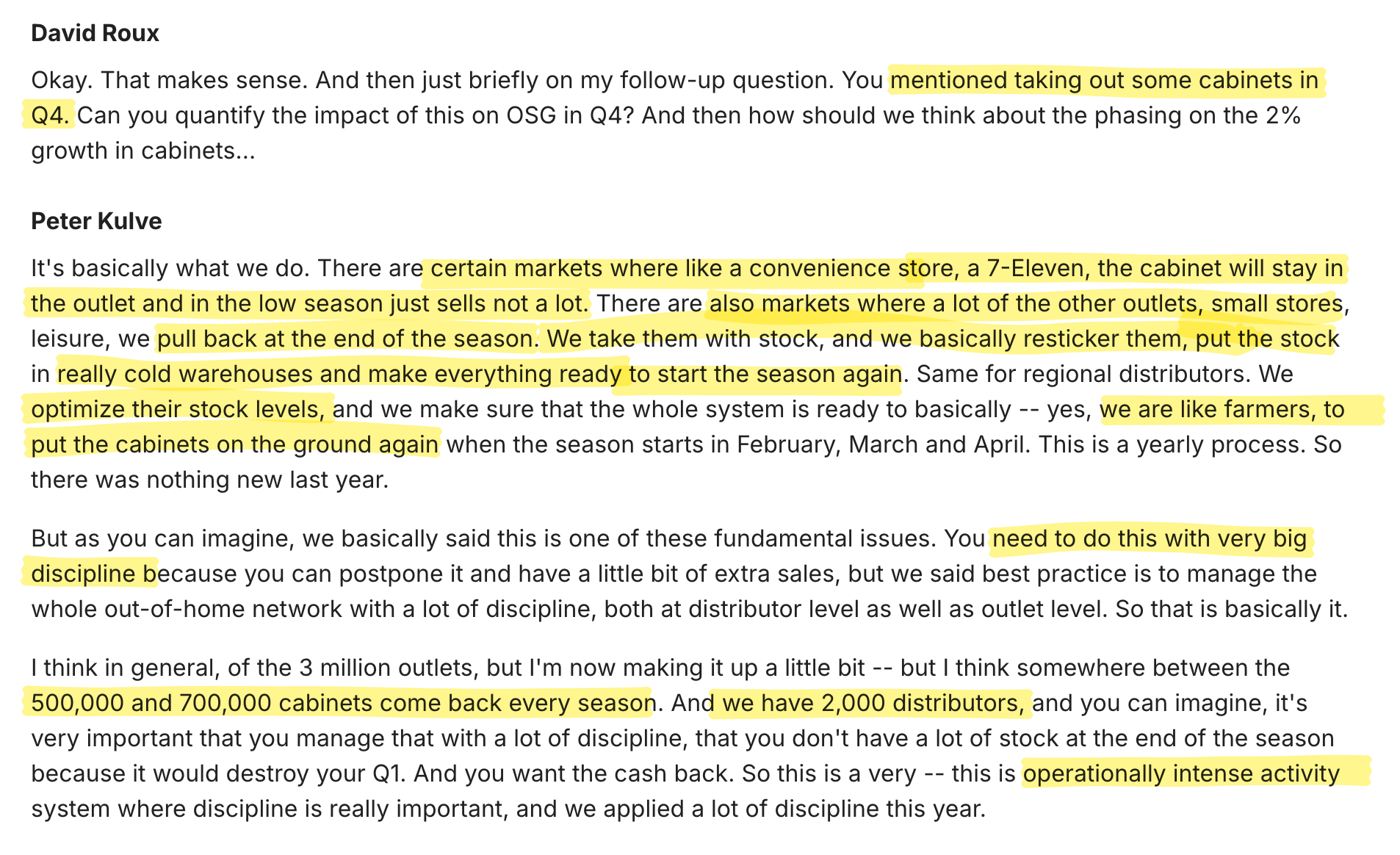

MICC operates a fleet of 3 million freezer cabinets, which is 2x larger than the next competitor (according to management). These are basically branded vending machines at convenience stores, malls, retailers, etc. This is a pretty unique (albeit capital intensive) asset for distribution and branding.

Cabinets are a key part of this as a critical enabler of growth and sometimes overlooked or misunderstood moat in our business. Our cabinets are like soft drinks chillers. They provide unique advantages that help us to maintain and grow market leadership. In 2025, we increased cabinet CapEx by around 10% to grow our market-leading fleet of 3 million cabinets.

The supply chain and working capital management behind these 3 million cabinets are crazy… some customers (like 7-Eleven) keep the cabinets plugged in year-round and navigate the seasonal sales volumes… for others, MICC picks up the cabinet during off-peak season, stores it in a cold-chain warehouse, and redeploys it for the selling season. They do this every year for 500-700k of their 3m fleet.

That sounds like an incredibly high barrier to the away-from-home market given the supply chain demands and capital intensity. And it’s starting to make sense how this business doesn’t mix with non-cold-chain products.

There are other nuances that I’m glossing over like the regional/geographic sales mix and profitability differences by geography. Short story: U.S. is the largest market, emerging markets have less per capita consumption and are growing much faster.

Why it’s interesting

The more I spend time on MICC, the more it looks like a classic botched spin-off with poorly communicated carve-out results & expectations (although this communication is improving as of 1Q26).

The initial pre-spin investor day presentation was held Sep 2025 and failed to include any firm guidance for 2026 or 2027. Instead, they alluded to 2028-2029 results following a period of increased investment and transition. Investors drew their own conclusions and expectations were high(er).

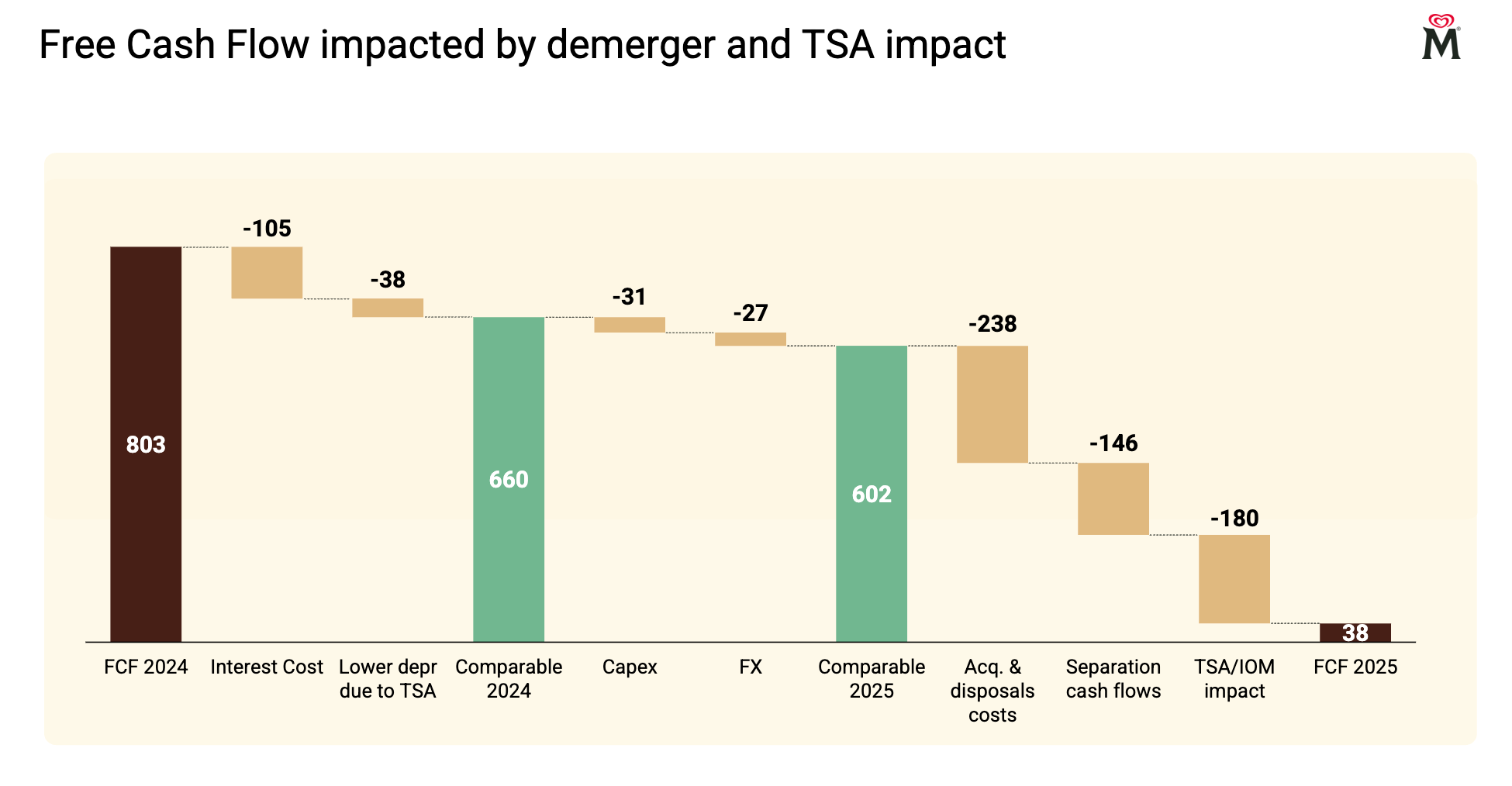

Then Q4 2025 results came out and the bar was reset. FY 2025 revenue was basically flat at €7.9bn, adjusted EBITDA fell to 6% to €1.26bn, and margins fell to 15.9% from 16.9%. Free cash flow was down to €38m from a comparable ~€600m. Net debt closed at ~€3bn, and the stock sold off hard after debut results (down 18-19%).

So what’s exciting about this?

1) Fundamentals + value creation algo

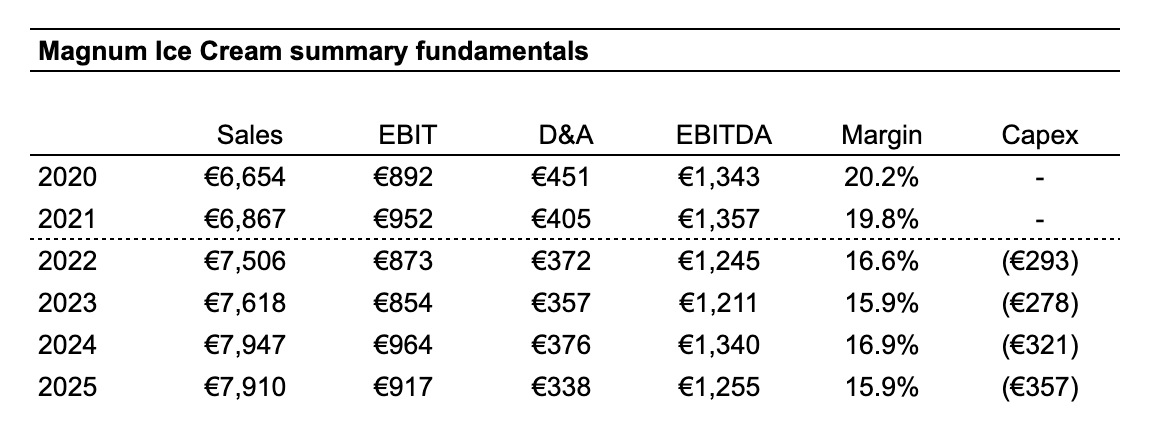

Starting with high level results for the past few years (note: Unilever separately disclosed ice cream segment results in 2020-2021):

It’s a straightforward financial picture: sales & EBITDA are mostly flat with margin degradation and increasing capex levels. Ick.

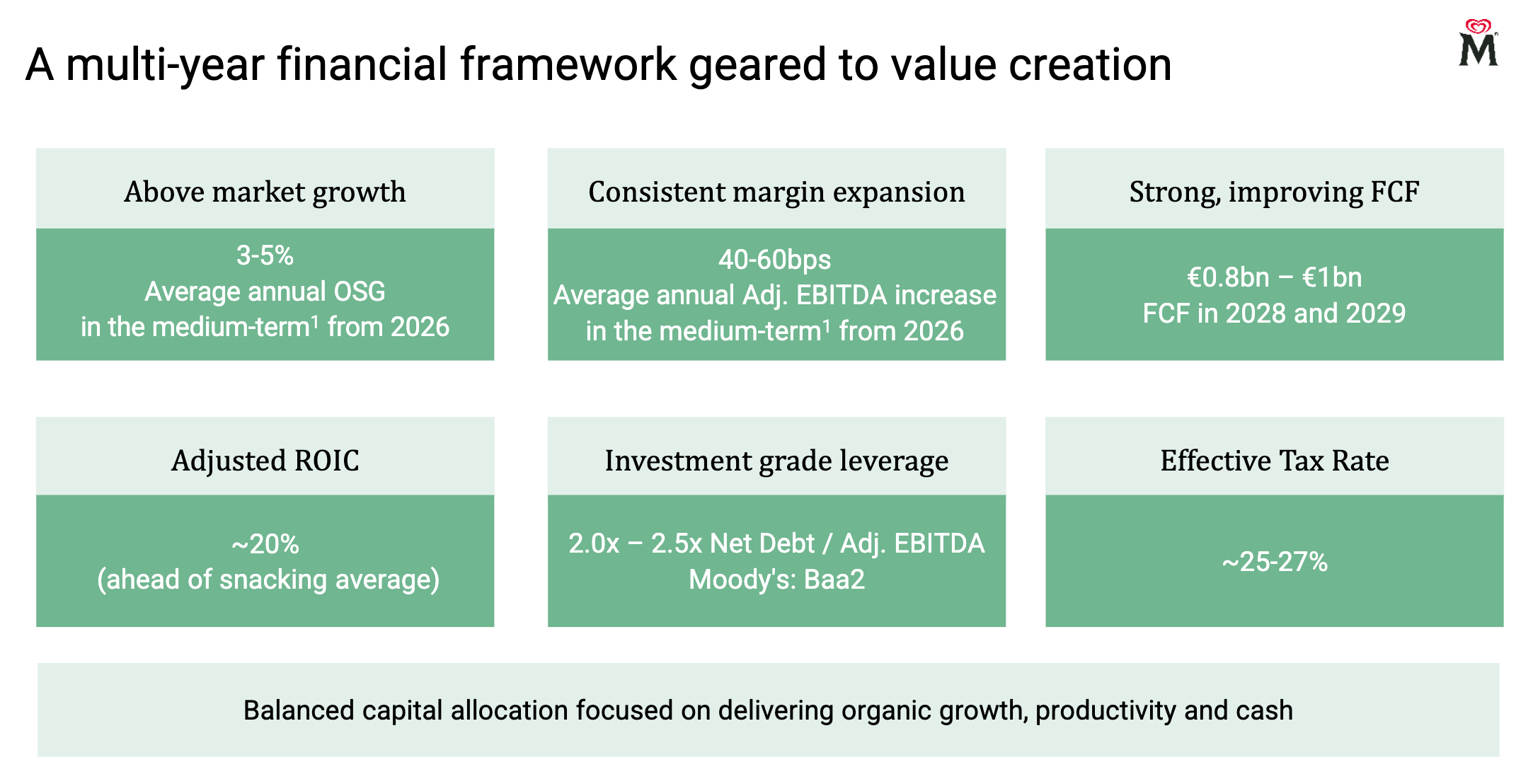

As a standalone company, management laid out the following “value creation framework” for 2026-2029: 3–5% organic sales growth, 40–60bps of annual EBITDA margin improvement, and €800m to €1bn FCF by 2028-2029. Promising.

If you do the math on 3-5% sales growth and 40-60bps margin expansion (17-18%), you’ll get somewhere between €1.5-1.7bn EBITDA by 2028 (sell-side is at €1.49bn). This works out to ~6-7x EBITDA and ~8-10x FCF on today’s price.

Seems cheap.

So why does this opportunity exist?

Carve-out results and guidance are incredibly confusing and messy (it’s never good when a spin-off fails to deliver a short-term guide at a pre-spin investor day). A look at forward EPS trends show this failure to bridge the carve-out numbers to short-term standalone results.

That’s just one piece of it…

On the other end, the short-term cash flow picture is very murky. Management says this business had ~€600m of pro-forma FCF in FY2025 when ignoring separation and transition costs. But those adjusting items took FCF near zero last year.

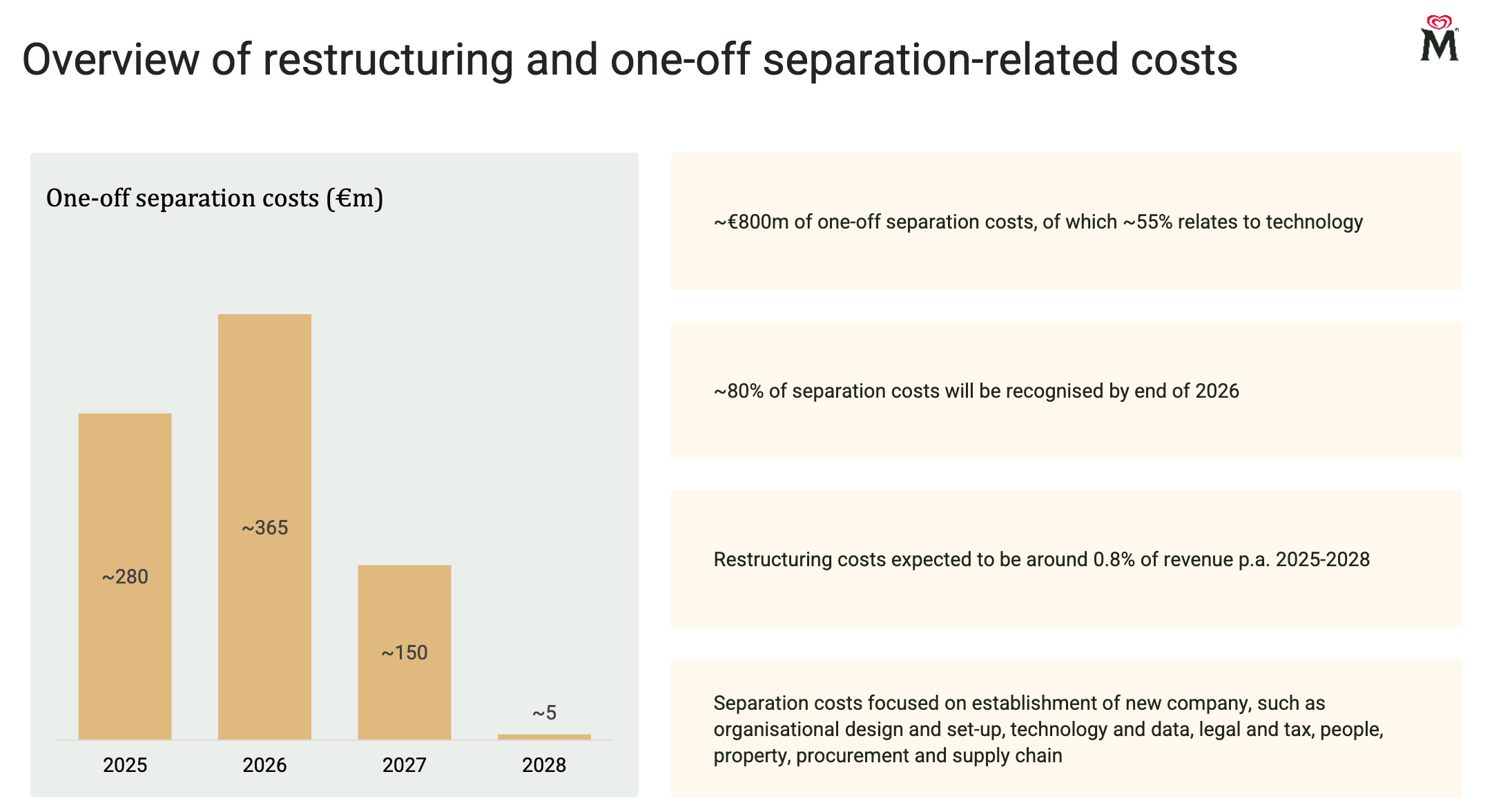

Transition costs will eat into a big chunk of 2026-2027 FCF…

Separation costs alone are €800m (10% of current market cap) with €365m coming in 2026 and €150m in 2027 before winding down to near zero in 2028.

On top of that, restructuring will cost ~0.8% per year on average. So here we are, management is telling us “this is complicated and we cannot guide to it.” Which amplifies the discounted valuation.

Analysts are expecting 200m+ FCF in 2026, but I think there’s a good chance it will be zero or negative this year. My math… 1.3bn EBITDA minus 180m interest, 160m taxes, 400m capex, and 425m separation & restructuring = 135m before working capital changes.

How will they achieve the 2028-2029 targets?

It’s clear this business had some deferred maintenance under Unilever’s ownership; fortunately, it operates in a market that’s already growing 3-4% annually. MICC volumes grew 1.1% and 1.5% in 2024 and 2025; and they’re guiding to 80bps of annual volume growth from here. So volumes is up, that’s good.

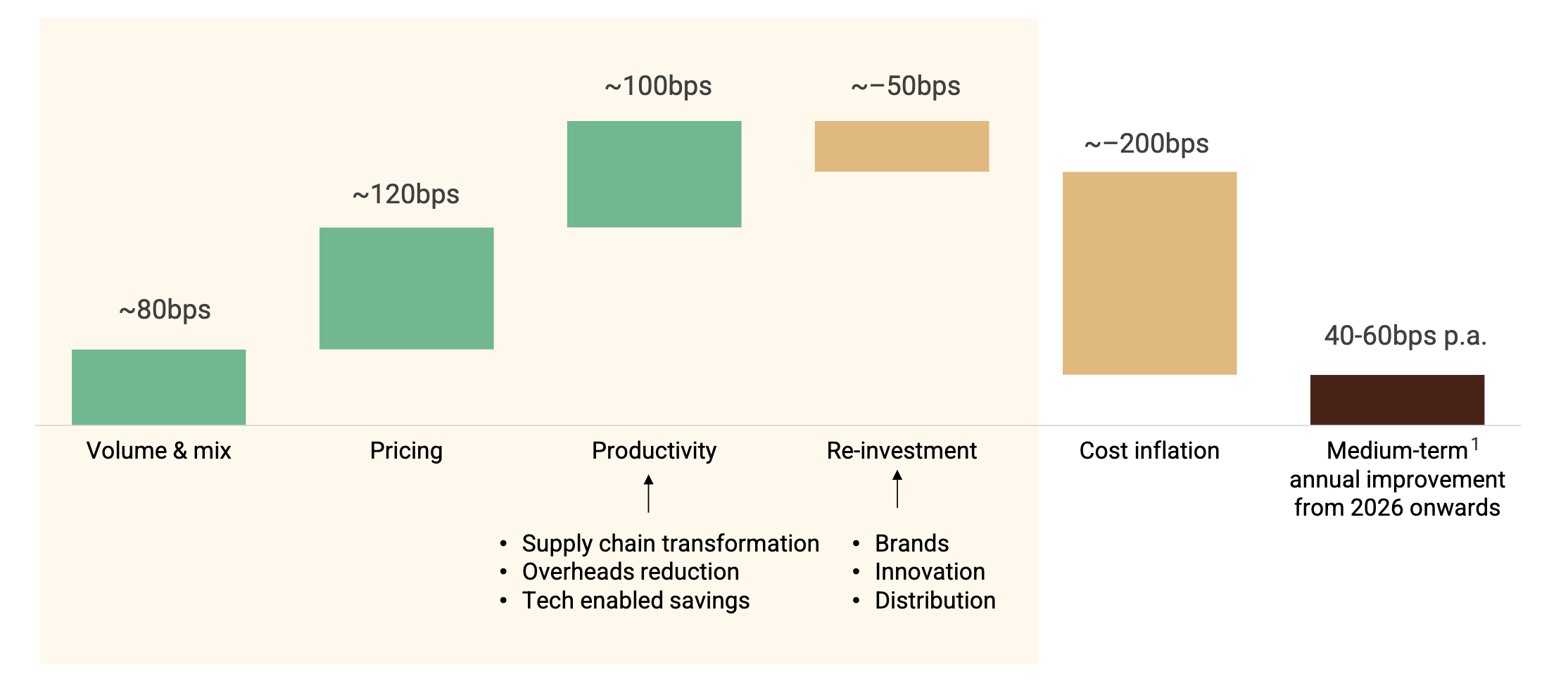

The other pieces to the margin improvement plan are fairly straightforward:

Net price declines of ~80bps per year — cost inflation at 200bps per year with price increases offsetting 120bps of that = roughly 80bps of price “investment” per year (this is likely a sales growth contributor)

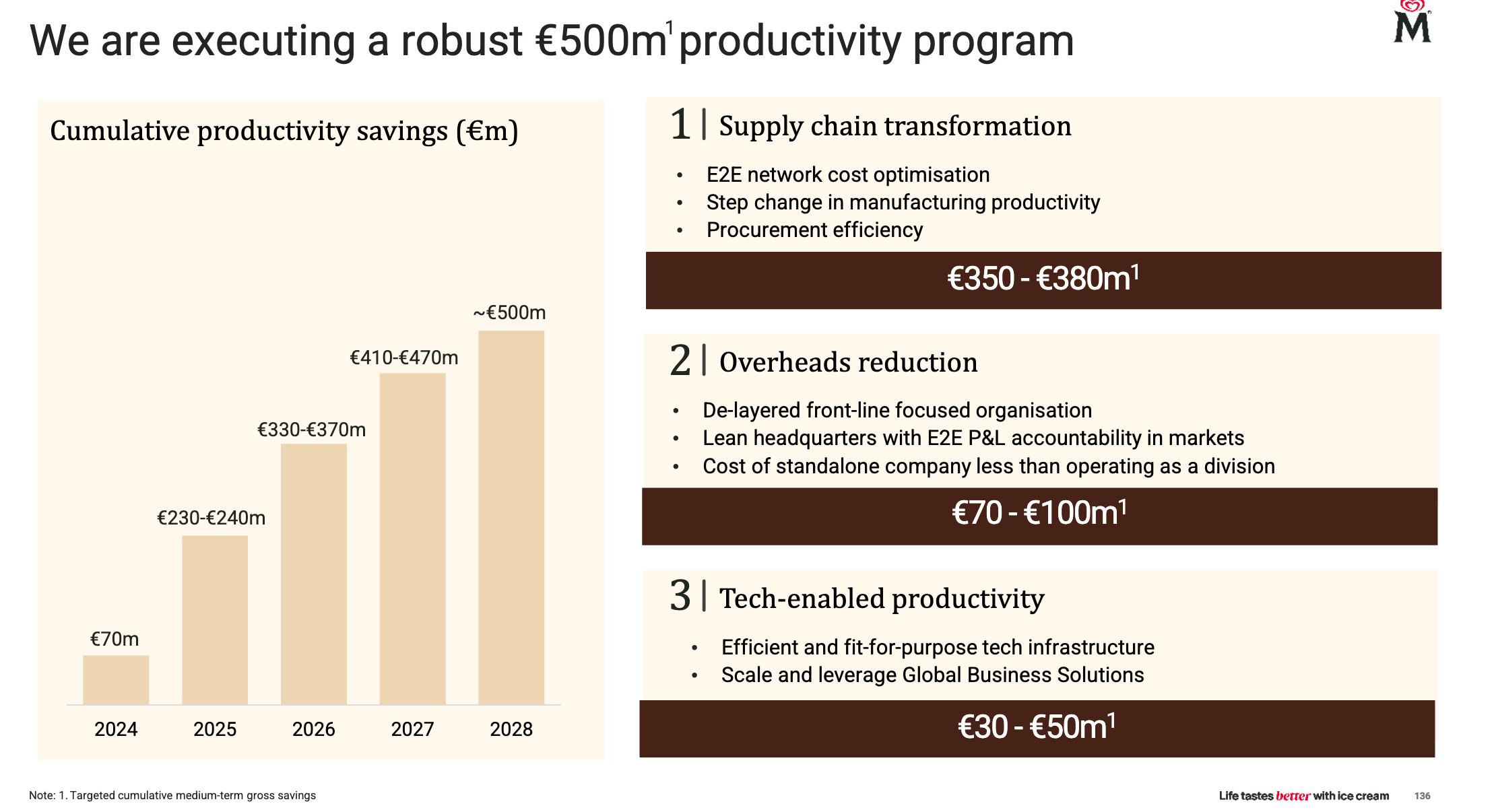

Productivity improvements — a €500m cost saving plan is underway with €260-270m savings expected during 2026-2028 (this is an earnings contributor)

Re-investment — higher marketing spend and increased capex levels add another 0.5% per year (again, likely a sales growth contributor)

Below are details on the timing and functional areas behind the cost saving program. If you net out the other pieces (volume, price/cost, and re-investment), this is the primary driver for the 40-60bps of annual margin expansion.

It’s also possible that commodity cost inflation headwinds in 2025-2026 turn into tailwinds for 2027. Cocoa represents ~22% of input costs and went parabolic the past 2 years. Here’s a 10-year chart of cocoa prices:

3) Valuation

For starters, there are 616m shares outstanding x $15 (USD) = $9.25bn market cap. At $1.17 per €1, that’s a €7.9bn market cap. Net debt is €3bn for a €10.9bn enterprise value.

Downside — Let’s assume EBITDA sticks around €1.2-1.3bn with €3bn net debt. At 6-7x EBITDA, that’s $10 per share or 33% downside.

Upside — I’m thinking about 2 approaches here:

First, if they achieve the €800m to €1bn FCF target and trade like the better CPG stocks (15-20x earnings) = $23-38 per share… that’s 50-150% upside

Second, the growth algorithm works out to €1.6-1.7bn EBITDA in the outer years… at 10-12x and no change in debt = $25-33 per share… that’s 67-120% upside

So that works out to 2-4x upside/downside ratio… Hmm…

Before getting too excited, it would make sense to: (1) handicap the odds of success (management teams rarely hit these multi-year targets with extreme precision); and (2) discount those 2029 results back to today.

Summing it up…

This situation reminds me of Kellogg (KLG) in 2023. That spin had a significant margin + earnings growth story but required a few years of reinvestment and cash outflows. It came out at a huge discount to peers and was eventually acquired as they made progress on long term goals.

I’m doing more work on these staples & CPG stocks. I like the Nomad Foods management change setup and MICC seems like a compelling 2x over a few years (also with a much cleaner-than-industry-average balance sheet). No positions yet, but I’m digging.

As usual, I love glossing over the risks when doing these write-ups… Input costs are killing margins right now: cocoa, dairy, sugar, energy, freight, and packaging all matter. Health trends, including GLP-1s, are a real risk; although management believes this will lead to more “premiumization.”

Disclosure: no position in MICC as of this writing

P.S. if you enjoyed this write-up, give it a like + share; help me spread the word :)

Resources:

Management has bought a lot of stock since the spin.

Nice writeup. I bought a Cuisinart ice cream maker a few years back which makes ice cream that tastes head and shoulders above anything store bought. Plus the Ninja Creami has to be taking share given all the buzz on social.