Quick Value #315 - Zoetis (ZTS)

Beaten down + massive valuation re-rating (30x earnings to 11x)

Today’s post:

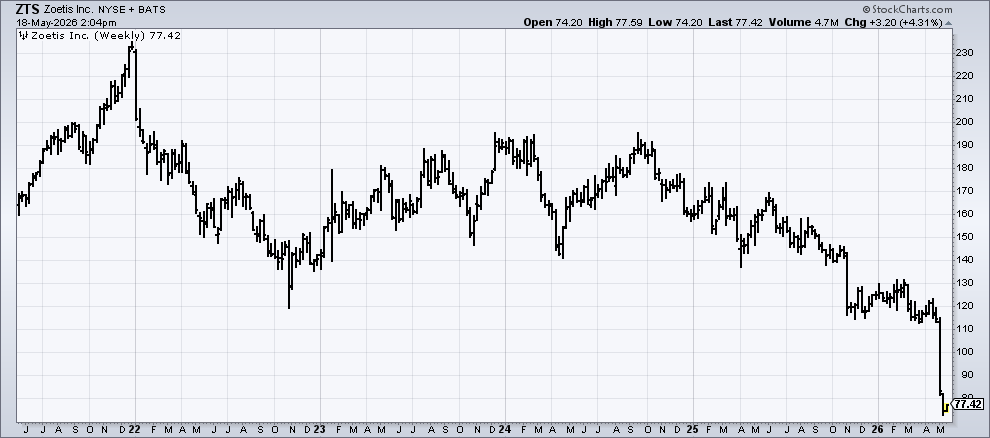

Shares down >60% from peak

Consistent cash flow and low leverage

Former compounder now trading at “deep value” price

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: 1) company background; 2) why the idea is interesting; and 3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

05/11/26 — Sale + spin at Enviri ($)

05/01/26 — Ice cream spin-off Magnum looks cheap

04/21/26 — Guide to analyzing “asset plays”

04/13/26 — Beaten down CPG stock Nomad Foods ($)

04/06/26 — Upcoming spin-off at Middleby ($)

03/23/26 — A look at GameStop fundamentals

03/16/26 — Green Dot upcoming sale + spin ($)

Quick Value

Zoetis (ZTS)

Ticker: ZTS

Price: $77

Shares: 420m

Market cap: $33bn

Valuation: 11x P/E

Theme: beaten downWhen I see shares plummeting ~40% over a short period of time, I can’t help but take a closer look…

Background

Let’s start with some backstory:

2013 — Pfizer took their animal health business, Zoetis (ZTS), public via IPO + split-off (not an official spin).

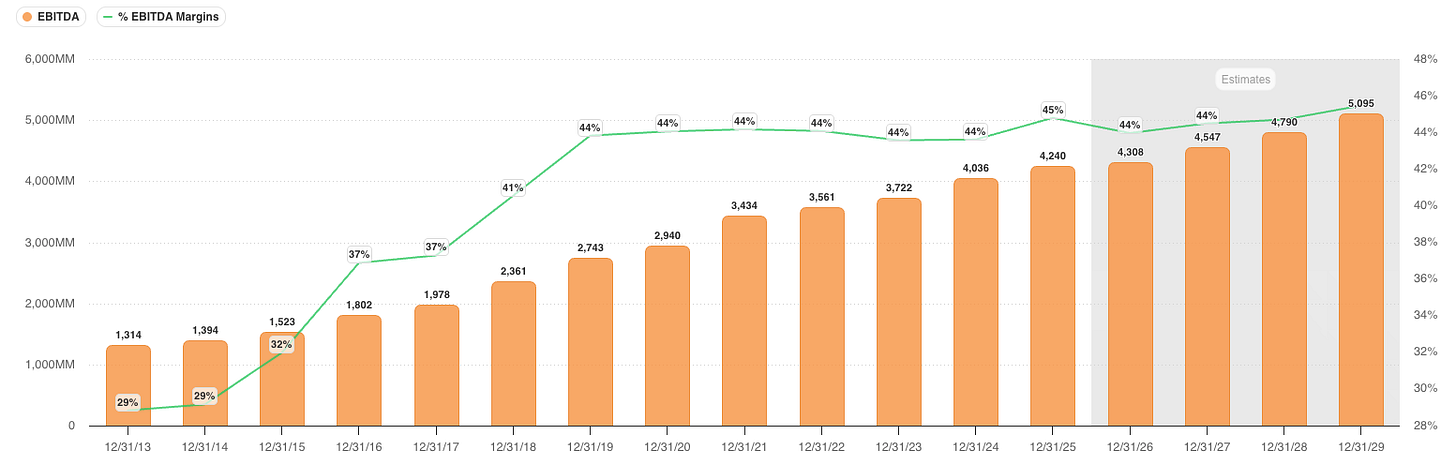

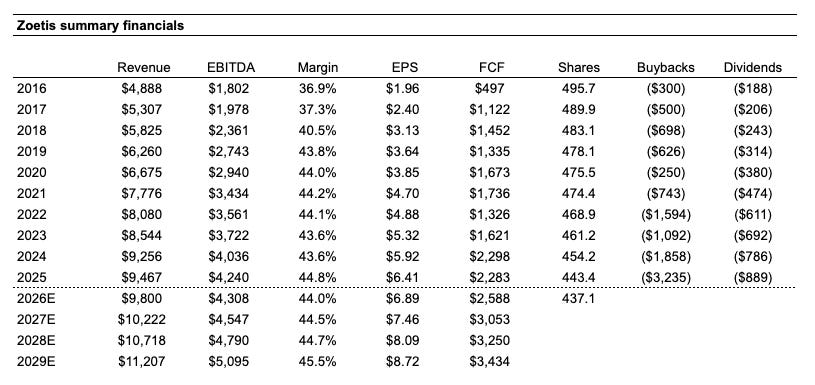

2013-2019 — This was a period of massive earnings optimization. EBITDA grew from $1.3bn to $2.7bn (13% per year) as margins increased from 37% to 44%. Shares went from $31 to $133.

EBITDA & margin trends 2013-2029E 2019-2024 — Both revenue and EBITDA grew ~47% (total) during this period as margins were flat around 44%. Shares went from $133 to $163.

2025 — Growth slowing below industry levels as new product launches disappoint leading to guidance cuts. Shares fell from $163 to $126.

2026E — Another downward revision in guidance during 1Q26 results and key portions of the business turning negative YoY. Shares fell from $126 to $77 (today).

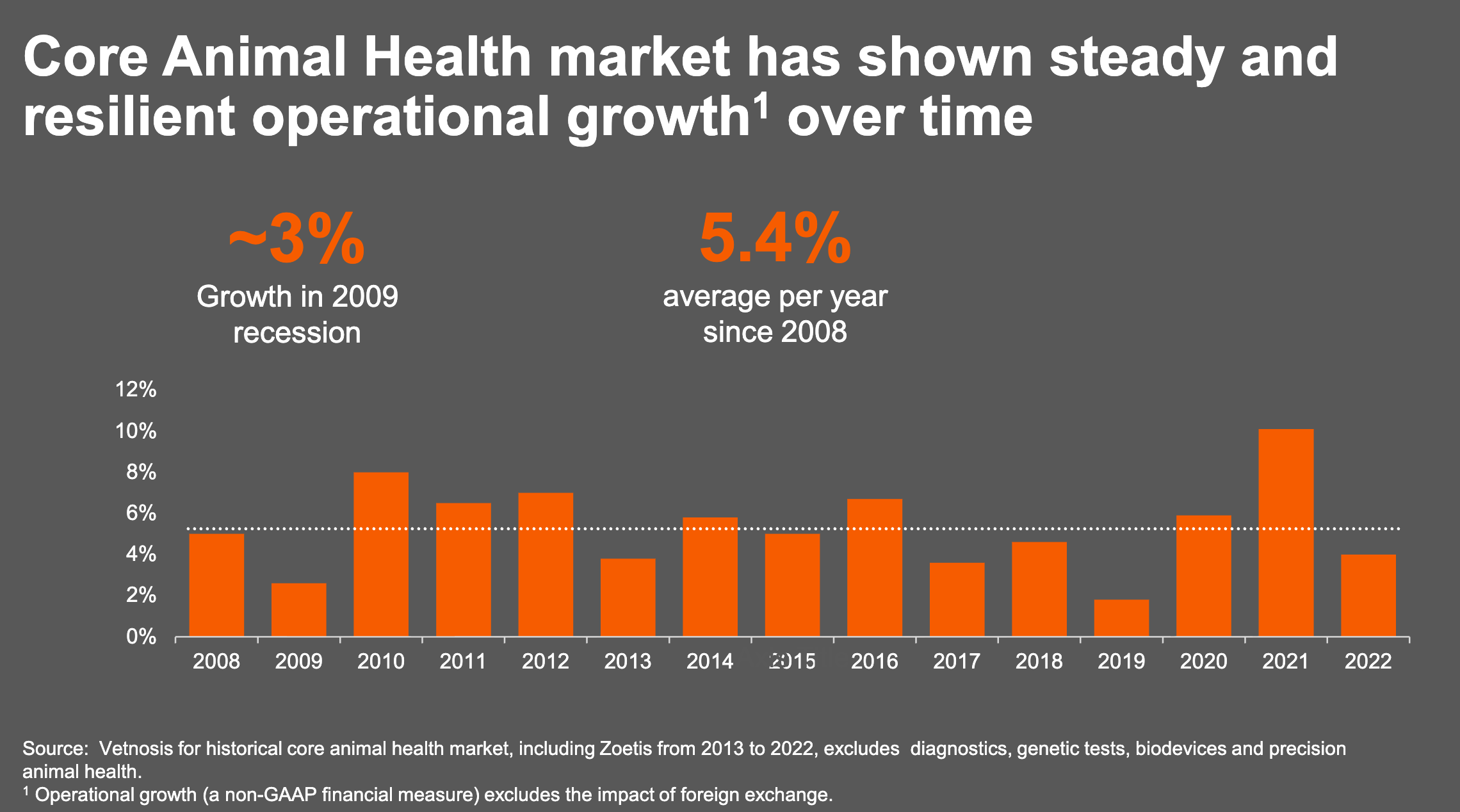

Animal health is a ~$50bn market growing 5-6% annually (lots of tailwinds). The market is split into:

Livestock — supporting production of animal protein (beef, dairy, swine, poultry, fish, etc.)

Companion-animals — supporting pet animals (mainly dogs, cats, and horses)

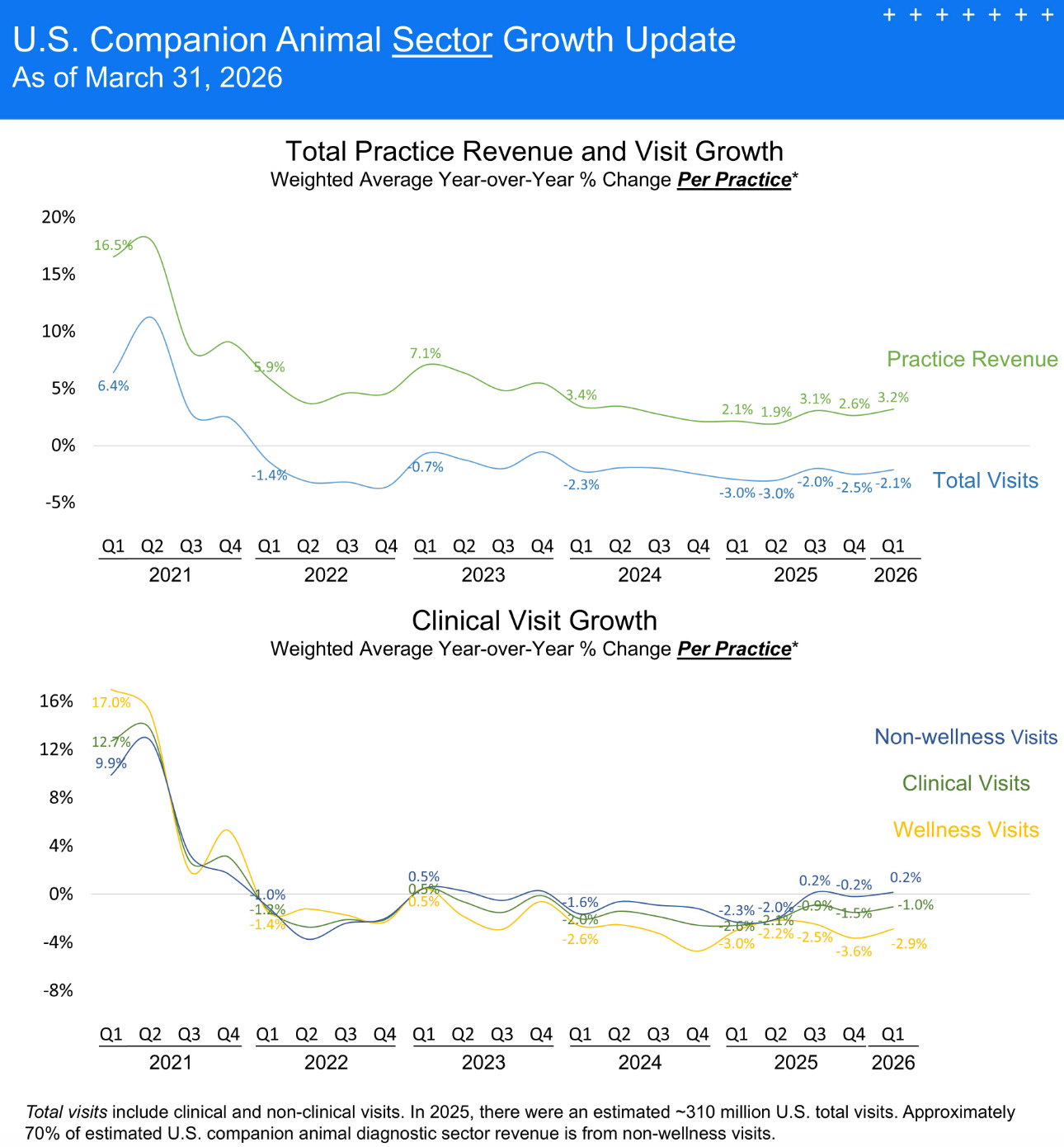

Customers are veterinarians or third-party veterinary distributors. So vet visits and those trends are a key driver for companion sales. Visitation trends have been negative for a few years now:

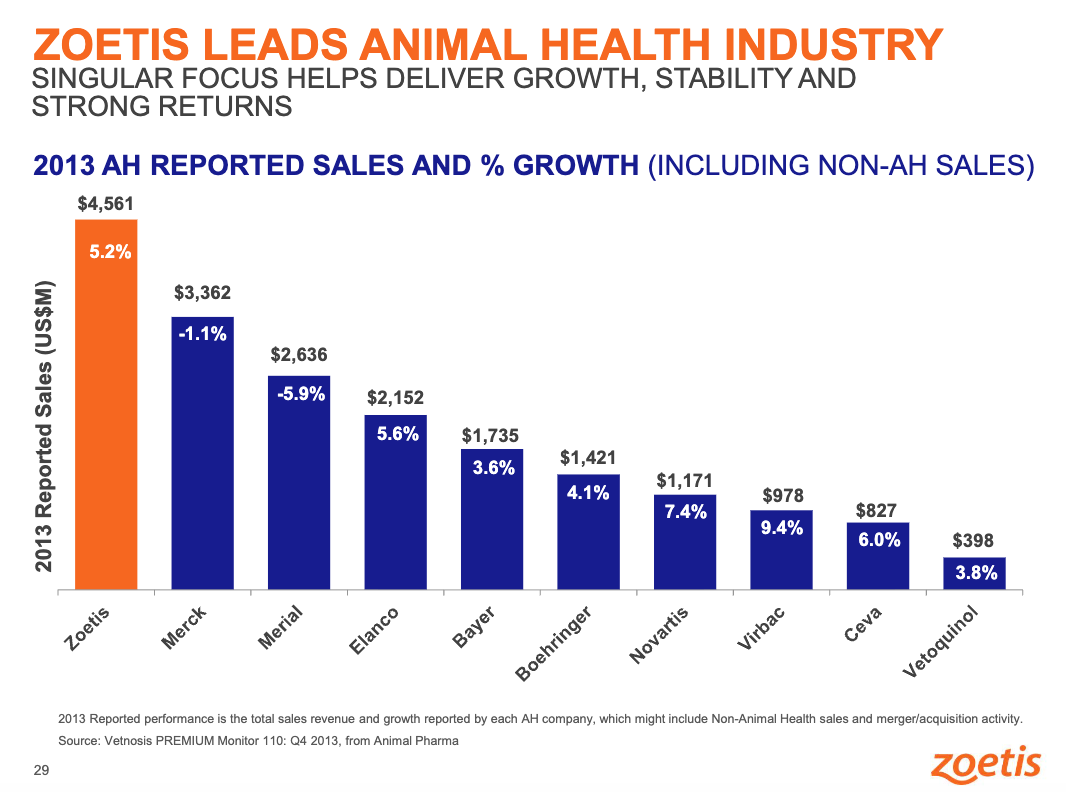

Zoetis is the market leader in animal health (slide below is from the 2013 split-off presentation):

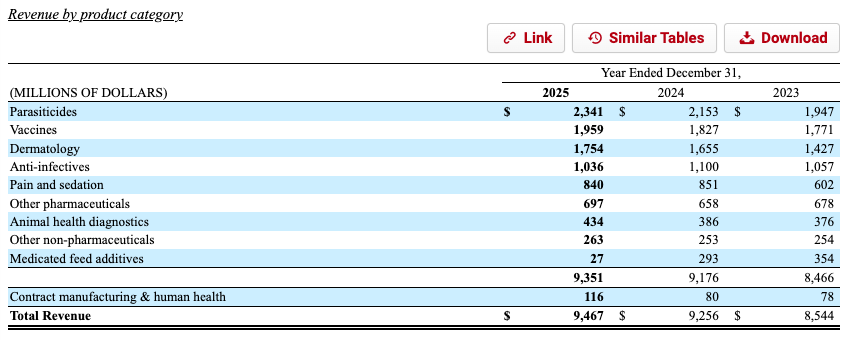

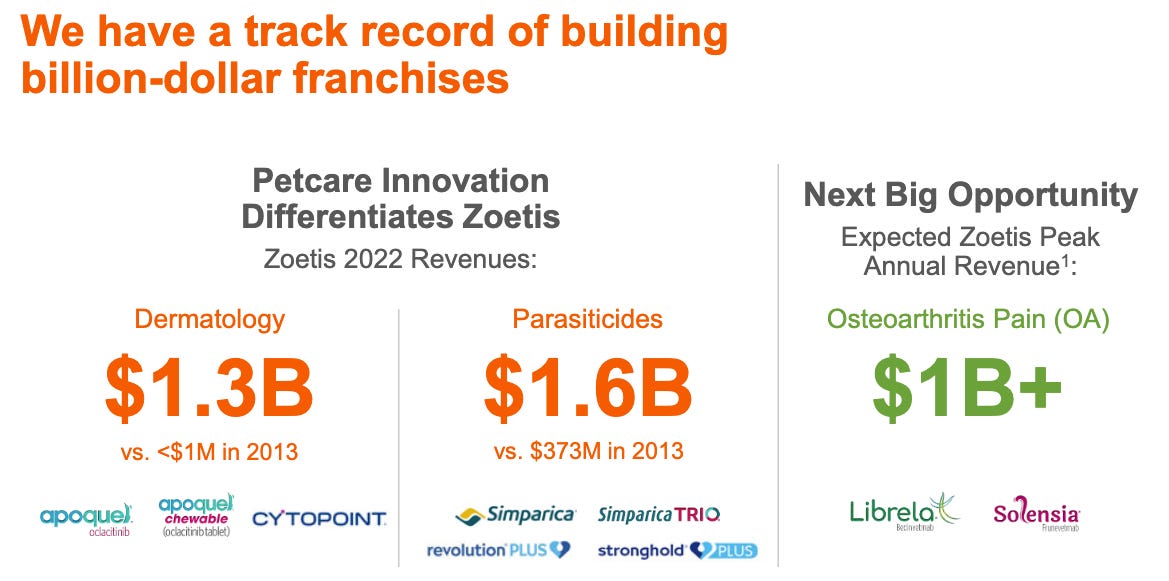

The product portfolio is fairly diverse across categories. Parasiticides is perhaps the most lucrative market (think flea and tick medicine) since it’s recurring in nature.

Product concentration:

Parasiticides — Simparica/Simparica Trio = 16% of 2025 sales

Dermatology — Apoquel/Apoquel Chewable = 12% of sales

Cytopoint (dermatology), Librela (pain) and our ceftiofur line (anti-infectives) = 14% of sales

Top 10 products = 57% of sales

Why it’s interesting…

Shares are down from a peak of $200+ to ~$77 today (60%+ drop). For a $32bn market cap (today) with low leverage in a growing industry, that’s fairly unusual. The stock is looking cheap (~11x 2026 earnings) and you likely have growth/quality investors selling to value + mean-reversion buyers.

So why are shares beaten down?

Let’s start with with how they got here…

At the time of the Pfizer split, Zoetis had 2 things going for them: (1) a massive cost reduction story; and (2) a period of meaningful blockbuster product launches.

Those cost initiatives produced a multi-year run of significant margin improvement (37% to 44% EBITDA margins), and it was a host of actions that contributed (cut low-margin SKUs, consolidating teams, manufacturing improvements, overhead reduction, etc.):

For product launches, the 2013-2020 period produced several blockbusters: Apoquel + Cytopoint in dermatology and Simparica + Simparica Trio in parasiticides. This group now produces ~one-third of revenue (>$3bn annually).

Librela + Solensia in pain and sedation were supposed to be the next batch of blockbusters launched in 2021. After a solid start, sales are now declining from safety issues. The 2025-2026 product slate looks less promising with launches designed to protect/extend existing products.

Translation: after a solid start at the time of the Pfizer spin, Zoetis has a lighter pipeline at a time where competing product launches are eating into core categories. Will touch on the pipeline more later.

How are the fundamentals?

This is where things start to get interesting…

We can see the “reset” in sell-side estimates (black line = share price, blue line = NTM EPS estimates, orange line = 2Y forward EPS estimates):

While earnings are still growing, that rate of growth is slowing and they are nearing an inflection where EPS growth could turn negative (orange line 2-year forward estimates still collapsing).

Historic financials are what you’d expect from a perceived “compounder” — 8% annual revenue growth since 2016, 10% EBITDA growth, and 14% EPS growth, all with modest leverage.

Aside from a few acquisitions, most/all free cash flow is going to buybacks and a modest dividend (2-3% yield at today’s price). The buyback pace hasn’t slowed recently ($606m in 1Q26 vs. $443m in 1Q25), but it’s potentially a risk if they opt to reinvest for growth.

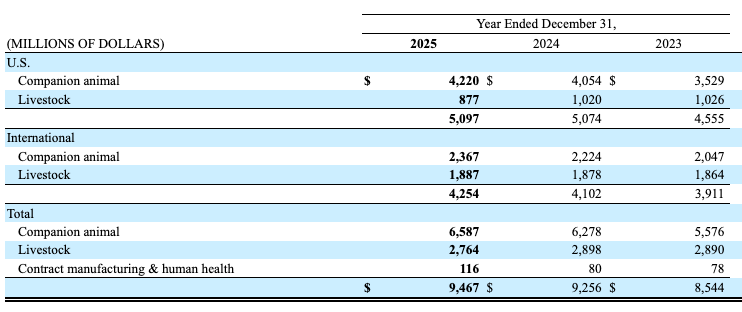

Underlying these fundamentals are a “domestic vs. international” and “livestock vs. companion” story too.

U.S. sales for livestock products were consistently declining from 2023-2025, and companion animal sales fell 11% in 1Q26 (bad)

International sales are consistently growing in both livestock & companion markets from 2023-1Q26 (good)

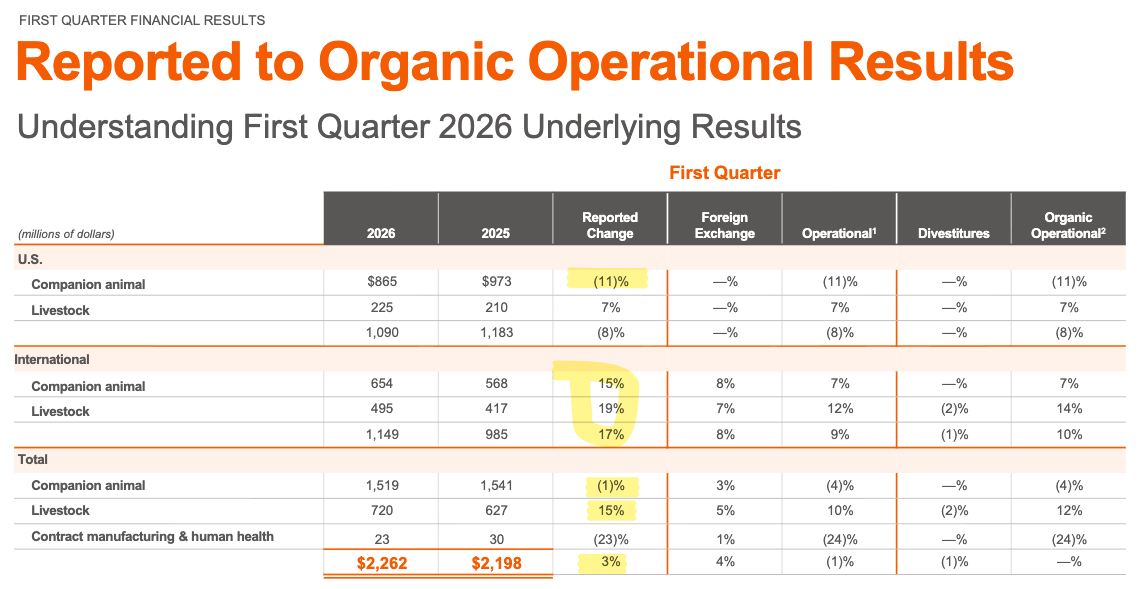

Q1 results highlight how quickly things are changing here…

US sales, which are >50% of total sales, fell 8% YoY with the companion animal business falling 11%. Management called out vet visit trends and increased competition (Elanco and others knocking on the door).

While International sales grew 17% YoY in Q1, they included a $100m benefit from a “fiscal year realignment.” Non-US subsidiaries were historically reported on a one-month lag which is being eliminated, so growth was really ~6.5% which is still good.

One final comment on the fundamentals before reviewing the outlook…

EBITDA margins are consistently 43-44%.

While that sounds amazing, peers are half to two-thirds that amount (~20% for ELAN, VETO, VIRP and ~33% for MRK animal health segment). If competition is rising, are ZTS margins more likely to compress down to peer levels? Probably… At the time of the 2013 spin, margins were 37%.

Hmm…

What’s the outlook from here? How can they turn the corner?

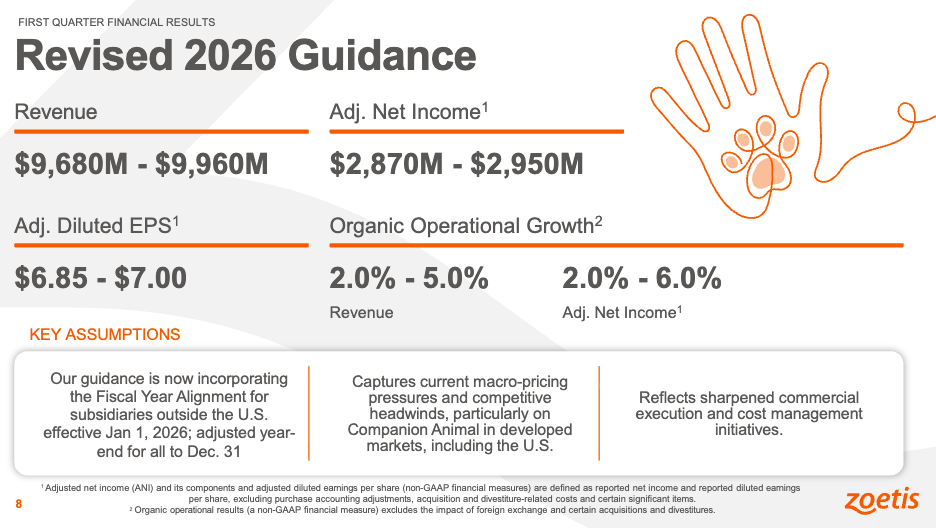

Guidance calls for ~$9.8bn revenue (2-5% growth) and $6.90 EPS (7-9% growth) at the mid-point. These were revised lower from an original 2026 guide of 3-5% sales growth and 9-11% EPS growth (market position worsening).

EPS guidance assumes a 419-421m share count so maybe there’s an opportunity for repurchases to contribute here.

The question is whether guidance adequately reflects near-term pressure from competition and pricing.

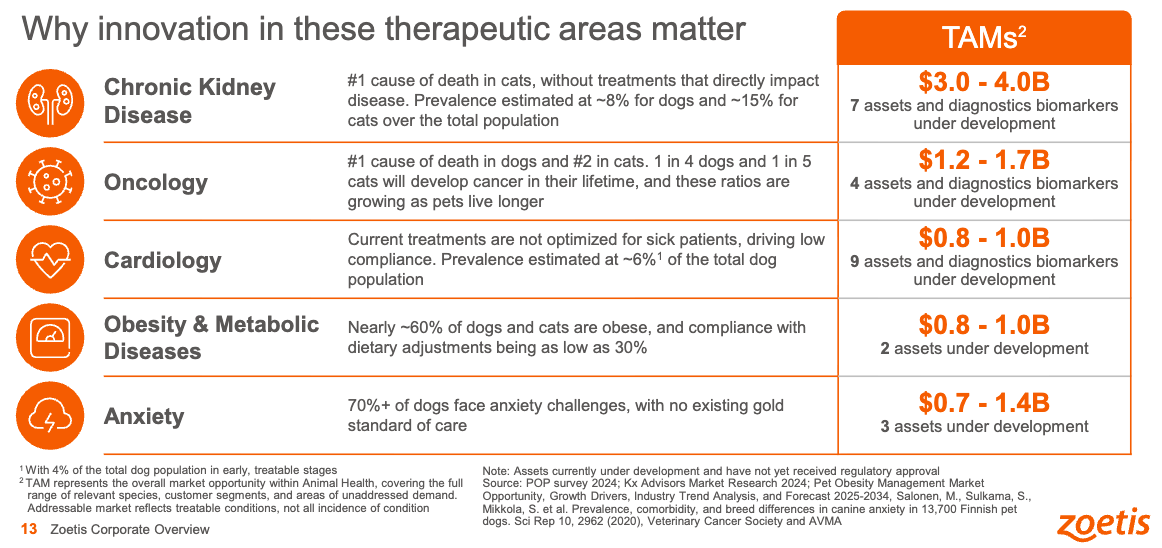

Beyond 2026, there are several large and untapped markets in play (kidney disease, oncology, cardiology, obesity) which have a $7-9bn TAM according to management:

Most of the products targeting these markets aren’t set for launch until 2027-2028+ so you’re looking at a business where the current portfolio will mostly drive results for the next 12-24 months and ~half that portfolio is facing near-term headwinds.

Hmm…

What could shares be worth?

Maybe there’s some light at the end of this tunnel…

First, this stock has completely re-rated to never-before-seen valuation levels. Shares were selling for 20x earnings (or more) right out of the gate in 2013 and 25x earnings for most of 2025.

Today, the valuation is half that.

There are several pure-play animal health comps with varying product & geographic mixes (MRK, IDXX, ELAN, VIRP, PAHC, VETO). That group is trading at 17-18x earnings and 10-12x EBITDA. As of today, ZTS is the cheapest in the group despite being the market leader.

What’s fascinating is this chart of ELAN’s historic valuation levels.…

Shares were levered >5x with low/no sales growth and declining earnings. The stock got as cheap as 9.7x earnings / 9.3x EBITDA. That’s pretty much where ZTS is today… Hmm…

My take on ZTS valuation:

Upside — Let’s say the pipeline pans out and they successfully launch at least 1-3 new blockbusters by 2028… At 15-20x earnings of $8.00-8.10 (current 2028 sell-side estimates) = $120-160 per share or 56-108% upside.

Downside — Let’s give ZTS some credit for revenue growth since this is a growing market and they’ll still have sizable product launches in 2027-2028. Assuming $10bn revenue (vs. $9.8bn 2026 guide) and 37% EBITDA margins (2013 levels) = $3.7bn EBITDA. A low-end 8x multiple with $7.1bn net debt and 420m shares = $54 per share or 30% downside.

I’ll call this a 2-3x upside/downside ratio.

Compelling…

Summing it up…

For the upside case to play out, you have to believe: (1) the drug pipeline is solid and will produce a few winners by 2028; (2) that guidance/expectations adequately reflect current weakness in the existing portfolio; and (3) that margins are sustainable despite increasing competition.

In my view, that’s a lot of stuff to get right…

On the bright side, a “much worse looking” ELAN back in 2023-2025 wasn’t trading much cheaper than ZTS today. And don’t forget, this is still a lucrative + growing end-market with volume tailwinds.

There’s a lot more going on than can be covered in a brief write-up like this, but the core bet here is mean reversion. I’ll add this to my watchlist and at least take a cursory look at competitors to get a better sense for the market.

Disclosure: no position in ZTS.

Resources:

Grant's wrote this up a couple months back. Solid stuff.