Quick Value #309 - GameStop (GME)

Profitable for first time since 2018 + sitting on pile of cash; now on the cusp of a mega acquisition?

Today’s post:

After the meme stock era, CEO Ryan Cohen has stabilized ops at core retail business (profitable for first time since 2018)

Board announced significant long-term incentive comp plan for Cohen in Jan 2026

Cohen shared thoughts around “transformational” acquisition(s) in Jan 2026

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: 1) company background; 2) why the idea is interesting; and 3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

03/16/26 — Green Dot upcoming sale + spin ($)

03/09/26 — CBIZ growth to value transition

03/02/26 — Ziff Davis sum of the parts ($)

02/09/26 — Wholesale changes in the VDL portfolio ($)

02/02/26 — A look at Allison Transmission’s recent acquisition

01/26/26 — Multi-pronged special sit Teleflex ($)

01/19/26 — A look at the KBR upcoming spin-off

Quick Value

GameStop Corp (GME)

Ticker: GME

Price: $23

Shares: 448m

Market cap: $10.3bn

Valuation: 18x pre-tax earnings

Theme: JockeyI’ll admit, this one is pretty far afield for me… but I’ve been curious about the news around this situation, enough to take a closer look. Here are my notes…

Background

GameStop operates 3,200 retail stores (as of FY24) across the U.S., Canada (since closed), Australia, and Europe selling video game hardware and accessories (consoles, controllers, etc.), software (new and used video games), and collectibles (apparel, toys, trading cards, etc.).

Some history is required to get the full picture here (note: GME uses the retail fiscal year so I’m mixing some fiscal and calendar years here):

2002-2016 — GameStop came public via IPO (~$2-3 per split-adjusted share). Revenue grew steadily from ~$1.1bn to $9bn+ and store count expanded from ~1,000 to >7,000. Shares went from $2 to $6.

2017-2019 — Secular decline fears ramped. Sold Spring Mobile AT&T retail stores. Revenue from $9bn+ to ~$6bn and saw first year of operating losses (FY18). Ryan Cohen takes initial stake in 2019. Shares went from $6 to $1.50.

2020-2022 — The “meme stock” era. Shares peaked at ~$120 (split-adjusted). Cohen named Board Chairman in 2021. Operating losses totaled $630m from 2020-2022. Shares from $1.50 to ~$18.

2023-2024 — Cohen named CEO late 2023. Store closures accelerate (~4,400 to ~3,200 at end of FY24). Operating losses fall from >$300m to $26m. Shares from $18 to $32.

2025-2026 — Store closures paving way to first year of profitability since 2018. Raised $3.4bn equity at ~$24.50/share. Raised $4.2bn from 0% convertible notes with conversion prices around $30. Announced long-term incentive plan for CEO Ryan Cohen. Shares from $32 to ~$23 (today).

Quite the journey for this company…

Today, Cohen owns roughly 9% of GameStop shares and this “bet” centers squarely around his capital allocation plans. If you’re unfamiliar with Cohen (founded and sold Chewy, activist investments, etc.) you can catch up via this wikipedia page.

Why it’s interesting…

No amount of fundamental analysis will paint a picture for what GameStop will look like in 3-5 years. An investment here is mostly (entirely?) tied to the optionality from CEO Ryan Cohen and how they plan to deploy $9bn+ cash & securities. (Full transparency: I like bets on optionality.)

1) Fundamentals (the present)

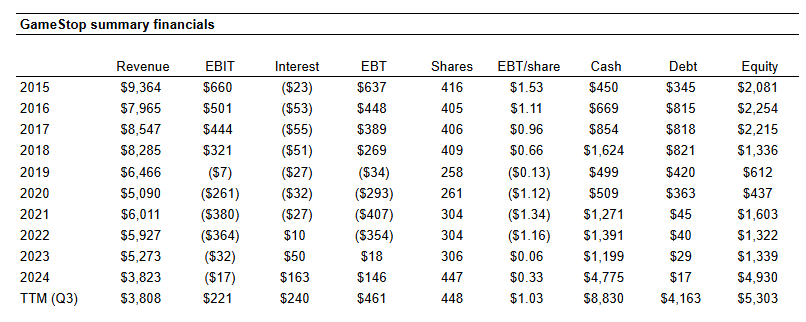

Here is the overarching fundamental picture from 2016-3Q25:

As of Q3, pre-tax earnings are ~$1 per share with $11.60 per share in net cash & securities.

How is it possible that a company lost $1bn+ from 2019-2024 and is now turning in $220m+ EBIT at the operating company level while revenues continue to decline?

There are 3 factors helping out here: (1) gross margin is improving from a higher mix of collectibles which are more profitable; (2) SG&A continues to decline; and (3) leases are rolling off fast.

Through 3 quarters of 2025, collectibles were >30% of sales vs. ~16% in FY2022. At the same time, gross margins went from 23% to 32%. Hmm… how sustainable is this trend?

Next, SG&A is running $913m over the past 12 months vs. $1.7bn as of Oct 2022. That’s a 46% decline in overhead while revenue declined 36%. So both gross profit and overhead are contributing to the earnings turnaround.

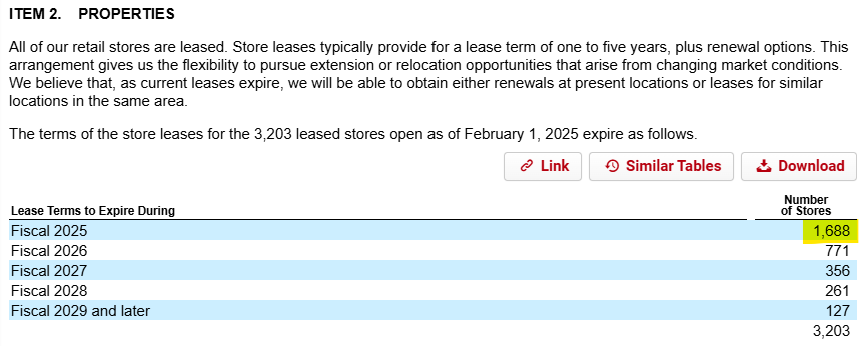

Last, Cohen stepped into an enviable lease situation with ~53% of store leases expiring in FY2025 (as a reference, Circuit City had only ~10% of their leases expiring within 4 years when they filed for bankruptcy in 2009).

It’s no surprise they’re quickly moving toward profitability with a chance to walk away from significant chunks of underperforming stores. In fact, I wouldn’t be surprised to see earnings trends improve throughout 2026 based on the lease schedule alone.

What is the current earnings power at GME?

At the operating company level (core GameStop stores), we have a business producing $220m EBIT on $3.8bn total revenue.

In addition, the company’s pile of cash & securities produced $240m net interest income over the last 12 months and a run-rate closer to $360m.

Combined, that’s $220m operating company EBIT + $360m investment EBIT = $580m or $1.30 per share (pre-tax). At $23, you’re effectively paying 17-18x pre-tax earnings for this business.

Granted, they borrowed $4.2bn at 0% interest which they’re capturing a nice spread on. Those converts will either need to be repaid or converted into equity. So it’s not quite as favorable as the picture I’m painting.

Realistically, treat it as $5.1bn net cash & securities ($11.60 per share) and $0.50/share pre-tax earnings from the retail operating company. That works out to 23x pre-tax earnings for the core business net of cash. Not super cheap.

2) Jockey (the future)

Forget all of that fundamental stuff for a moment…

Ryan Cohen has been CEO since late 2023 and we’ve (so far) seen a major improvement in core earnings and a significant amount of capital raised. What’s next from him?

There are 2 “developments” that seem important here:

The board granted Cohen a massive long-term pay package tied to performance

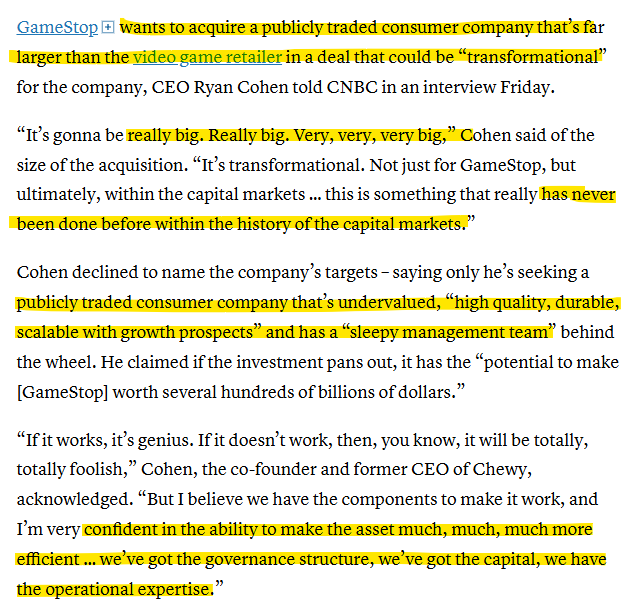

Cohen stated he wants to acquire a large, cash-flowing, consumer business

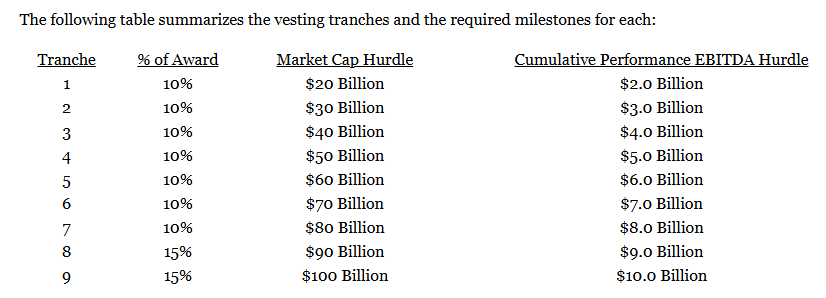

The pay package has major shareholder alignment. Cohen takes no salary, receives no cash bonuses, and no other stock incentives.

Instead, he has an “all or nothing” incentive plan consisting of options to buy 171.5m shares at a price of $20.66 broken down into 9 tranches with hurdles for market cap and cumulative EBITDA:

I like that it’s structured as pre-defined options which should prevent excessive dilution. We’re still waiting on the proxy filing to get important details and disclosures around this package which has not yet been approved by shareholders.

So what will they (he) buy?

We’re now reading tea leaves here, but it’s certainly interesting to speculate. Here are comments from Cohen during a recent Jan 2026 CNBC interview:

Hmm…

It sounds like conversations are potentially already in motion here, some of this commentary reads as though a 2026 timeline could be realistic.

What could they be looking at? Well here are some consumer businesses with a market cap between $10-40bn that are trading between 10-20x earnings:

There are several retailers in here which make sense from the growth comment (LULU, DECK, ULTA, HAS). Best Buy (BBY) is intriguing since it could have some synergy/overlap with GME stores and has a market cap below $15bn. Plenty of homebuilders, casinos, and auto parts on the list as well, but do those fit the “durable” and “growth” criteria?

The biggest deterrent (to me) would be seeing GME become another MicroStrategy bitcoin treasury stock, but Cohen said he views crypto as mostly an inflation hedge.

Summing it up…

At this point I’m just keeping some notes for myself and speculating on what this business could look like in a few years (different is the answer).

Things I’d want to understand or think about further:

If GME walks away from ~half their store base, what could earnings look like at the core retail business?

What will they do with the retail concept 3-5 years from now? Does it stabilize or do they sell it after getting profitable?

What acquisition targets are truly realistic? Both from a fit perspective and a size/affordability perspective.

Leave a comment if you’ve thought deeper about this one or what the company could be looking at acquiring.

Disclosure: no position in GME

P.S. I have not read any of Burry’s work on this stock.

US stores are the only profitable bits it looks like (~$153M op. inc. T9M-Nov25). Very impressive considering it doesn't include final X-mas shopping and compared to T9M-Nov24 of -$42M. FY24 US ended at -$2M. Assuming he 'only' matches Q4-24 performance of +$40M (seems unlikely given 2025 performance), US would be ~$200M operating income for 2025.

Best Buy (per seeking alpha) trades ~8x-9x EV/EBIT. At 6x-9x $200M gives $1.2B to $1.8B for GME USA.

If he drops AUS/EUR it will help profits. Per the financials, proceeds from divestitures were -$3.4M at Nov25 and $0 at Nov24. Assume he can get away without too much of a dent divesting the non-US businesses.

So let's say $5B net investments, $1-2B for US GME and ~$10B market cap meaning optionality costs $3-4B. So basically 30-40% of your money would be 'on risk' so to speak.

Downsides for me include the bitcoin position and comments like "If it works, it’s genius. If it doesn’t work, then, you know, it will be totally, totally foolish". A bit concerning. Feels closer along the spectrum to Musk than Buffett. Which is fine. It just is what it is.

My conclusion would be that there is no logical way to price the 'option' of Cohen. Is it 'worth' paying $4B to have this guy invest $5B of your money + whatever clever retail/deal making he can do? No sensible way to do that math.

I think Burry's comments in Jan are the thesis. Burry 'believes' in Ryan, who is young and is going to work for a long time. Period. That's the deal.

If you believe this guy is good at building retail/consumer businesses and will keep all his efforts under the GME banner, then it's probably worth it. He's obviously skilled.

It might be easier to reverse the thinking. Assume you agree with my back-of-napkin math and bought a 10% position size.

Would you lose sleep betting 4% of your capital on Cohen doing something smart over time?