Quick Value #320 - Somnigroup (SGI)

A dominant industry player on a spree of vertical integration deals

Today’s post:

Dominant industry player during deep industry recession

Multi-year targets call for MSD sales growth and 20%+ EPS growth through 2028

Pending acquisition adds deep vertical integration

For new subscribers — these write-ups are meant to be a “jumping off point” for the idea generation process (i.e. a surface level review). Each write-up includes: (1) company background; (2) why the idea is interesting; and (3) fair value estimate.

Check out past write-ups here and my home base page here.

Recent write-ups include:

06/23/26 — Guide to GoodCo / BadCo situations (a look at Tripadvisor) ($)

06/15/26 — Campbell’s is another beaten down staple

06/01/26 — All-stock cabinet merger MasterBrand

05/31/26 — A case study of a stub business investment

05/26/26 — My 4 favorite special sits right now ($)

Quick Value

Somnigroup International (SGI)

Ticker: SGI

Price: $78

Shares: 233m (pro-forma for LEG acquisition)

Market cap: $18bn

Valuation: 24x P/E

Theme: M&A

I’ve previously written about (and owned) shares of Leggett & Platt (LEG) which is set to be acquired by Somnigroup in an all-stock merger by yearend 2026…

It seems fitting to give the acquirer a quick review.

Background

SGI is a vertically integrated manufacturer, wholesaler, and retailer of mattresses and bedding products.

They have undergone a significant transformation over the past few years:

2012 — Tempur-Pedic acquires Sealy Corp to become Tempur Sealy

2013-2019 — Period of low/zero growth in sales and EBITDA from: Sealy integration, breakup from Mattress Firm relationship, and rise of DTC brands like Casper, Purple, etc. (Note: Mattress Firm filed for bankruptcy in 2018)

2020-2024 — Pandemic/stimulus buying plus the acquisition of UK retailer Dreams pushed annual sales from ~$3bn (2016-2019 average) to ~$4.9bn (2021-2024 average)

2025 — Tempur Sealy acquires Mattress Firm for $5.1bn in cash & stock deal to create vertically integrated bedding manufacturer & retailer, changes name to Somnigroup Interational (SGI)

2026 — SGI announces $2.5bn all-stock acquisition of Leggett & Platt (LEG) to add vertical integration capabilities

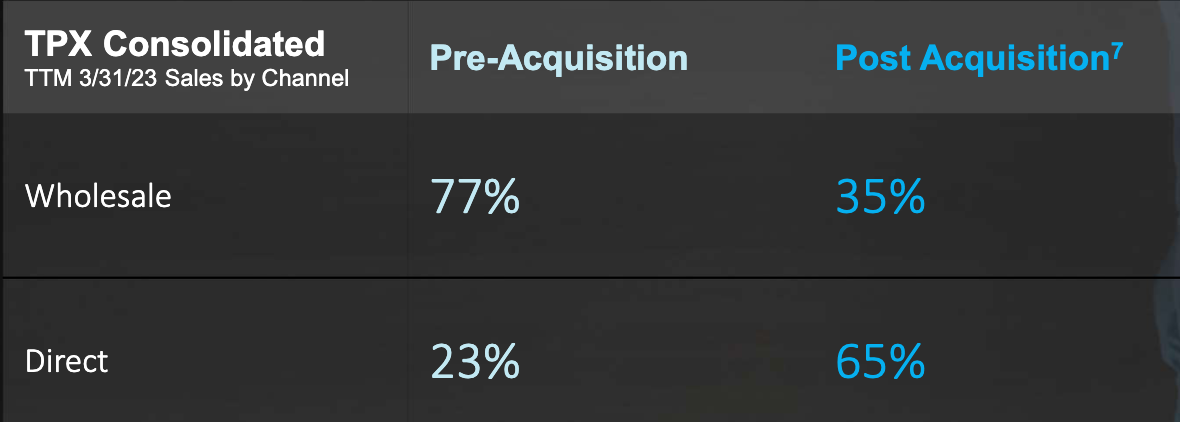

Prior to the Mattress Firm acquisition, SGI was primarily a manufacturer and wholesaler (77% of sales). That model flipped with the addition of MF’s 2,000+ retail stores:

Today, SGI owns a collection of mattress brands (Stearns & Foster and Tempur-Pedic on the premium-end and Sealy’s on the value-end) with robust distribution via 2,100 retail stores in the U.S. (Mattress Firm) and another 200 stores in the U.K. via Dreams.

They are the dominant industry player with revenue 5-6x higher than peers.

What is the state of the industry today?

Bedding is a $120bn global market of which SGI has $7bn annual sales. Mattresses as a sub-category are closer to $50-$60bn with 2025 industry volumes at ~70% of normal replacement levels.

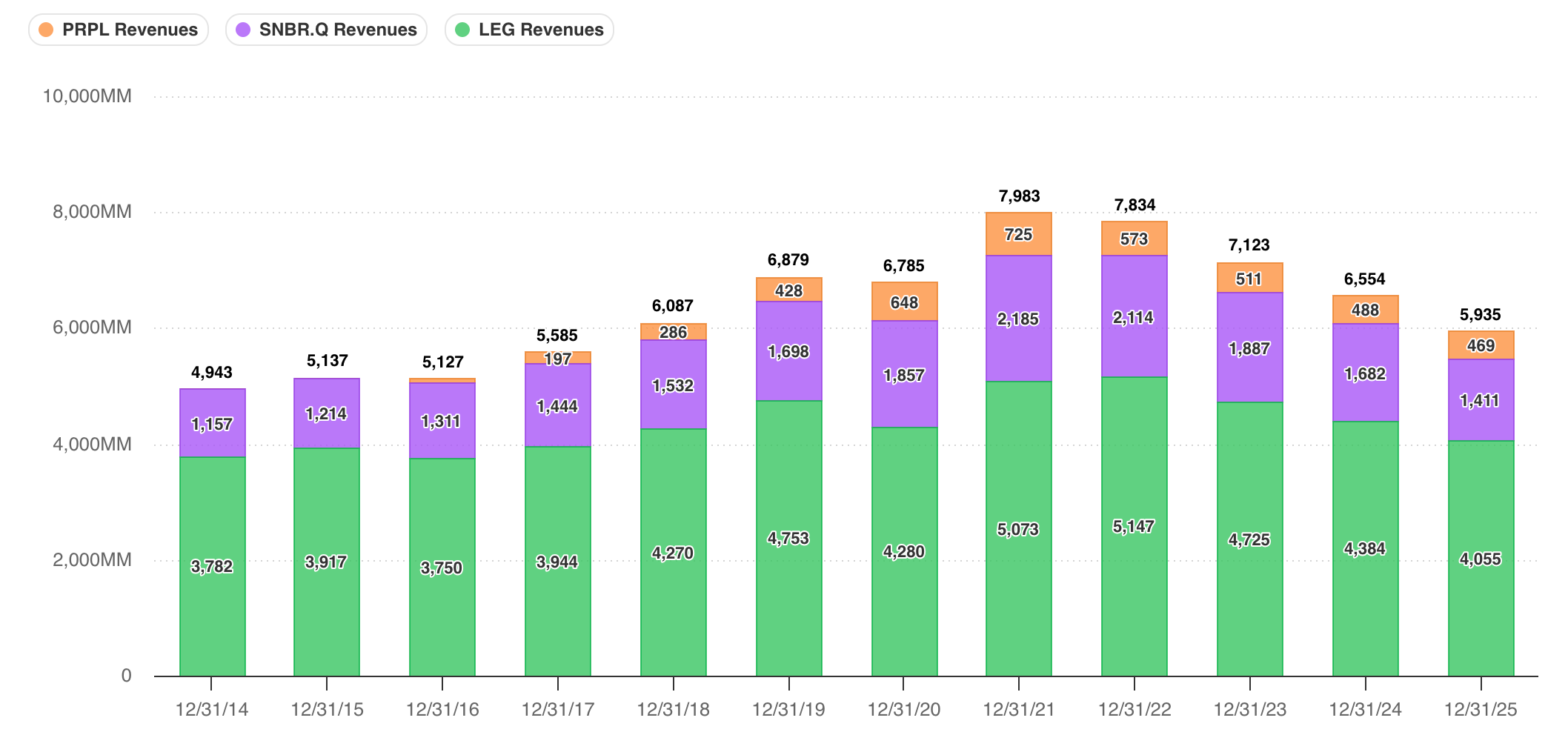

The chart below highlights annual revenue for Purple, Leggett, and Sleep Number (now bankrupt). It perfectly captures the industry’s DTC-fueled growth from 2014-2019, pandemic spike in 2021, and slow decline thereafter:

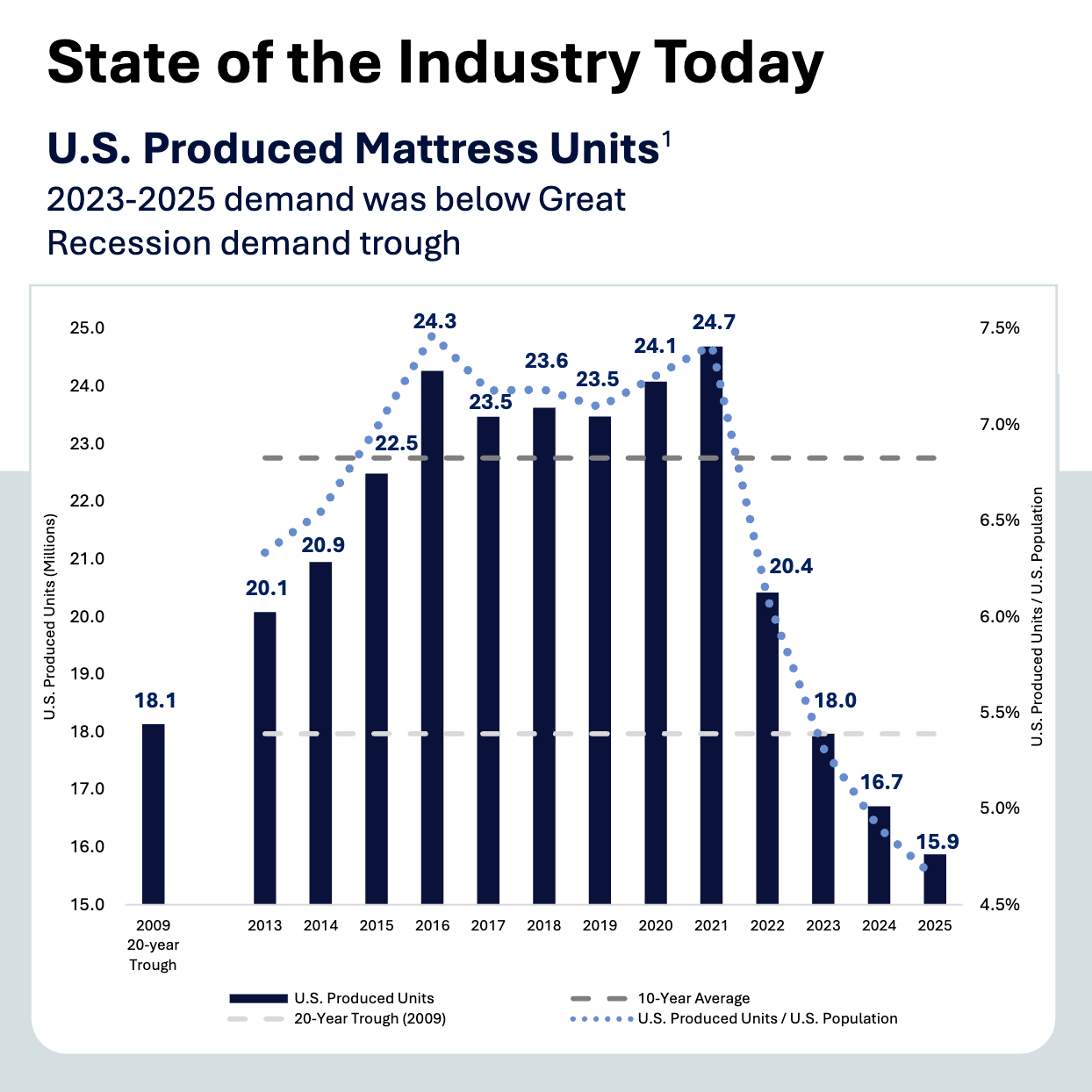

Domestic production volumes were 15.9m in 2025 which is 12% below 2009 trough levels and 30% below 10-year average levels:

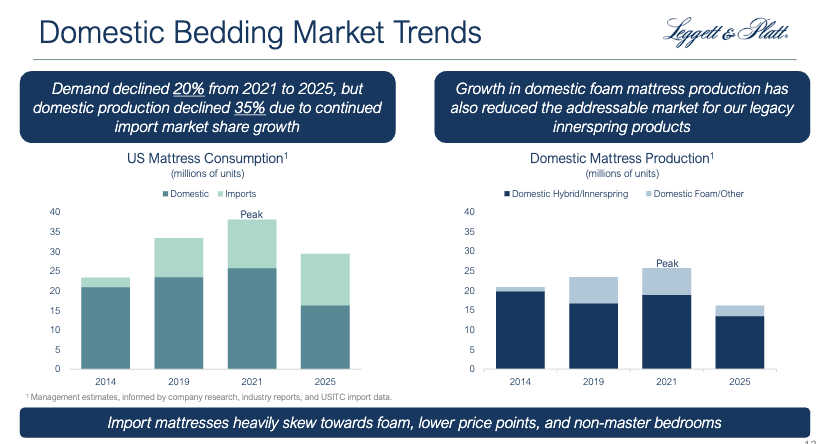

Pandemic & stimulus demand was one contributor to those collapsing volumes… rising imports are another:

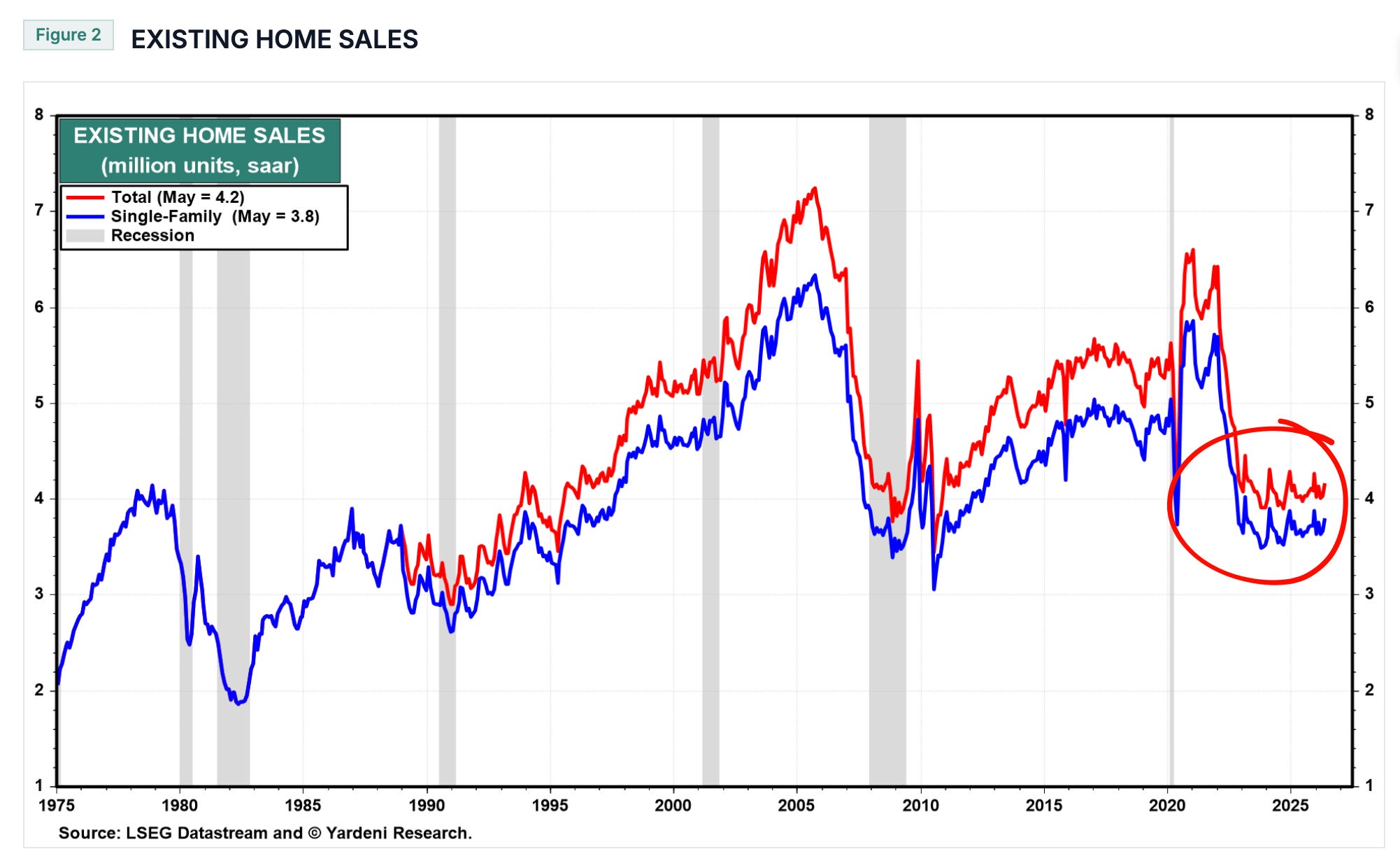

And a weak housing market is yet another (new mattress purchases are closely tied to moving into a new home):

Despite the incredible industry weakness, SGI remained (and remains) a profitable company.

Why it’s interesting…

There are 2 main reasons to like this idea here…

Leggett acquisition comes at a bargain price of <6x EBITDA and ~10-12x EPS

SGI is the dominant player in an industry operating WAY below historic volumes

First, a look at the fundamentals at SGI

Some highlights:

Legacy SGI went through a tough period during the rise of DTC brands like Casper and Purple. From 2014-2019, sales & EBITDA were essentially flat.

Then COVID came, and with it a boost in online shopping and stimulus money. Tack on the Dreams acquisition (2020) and sales jumped ~50% from the 2014-2019 average.

Results plateaued again from 2021-2024 leading up to the Mattress Firm acquisition (2025).

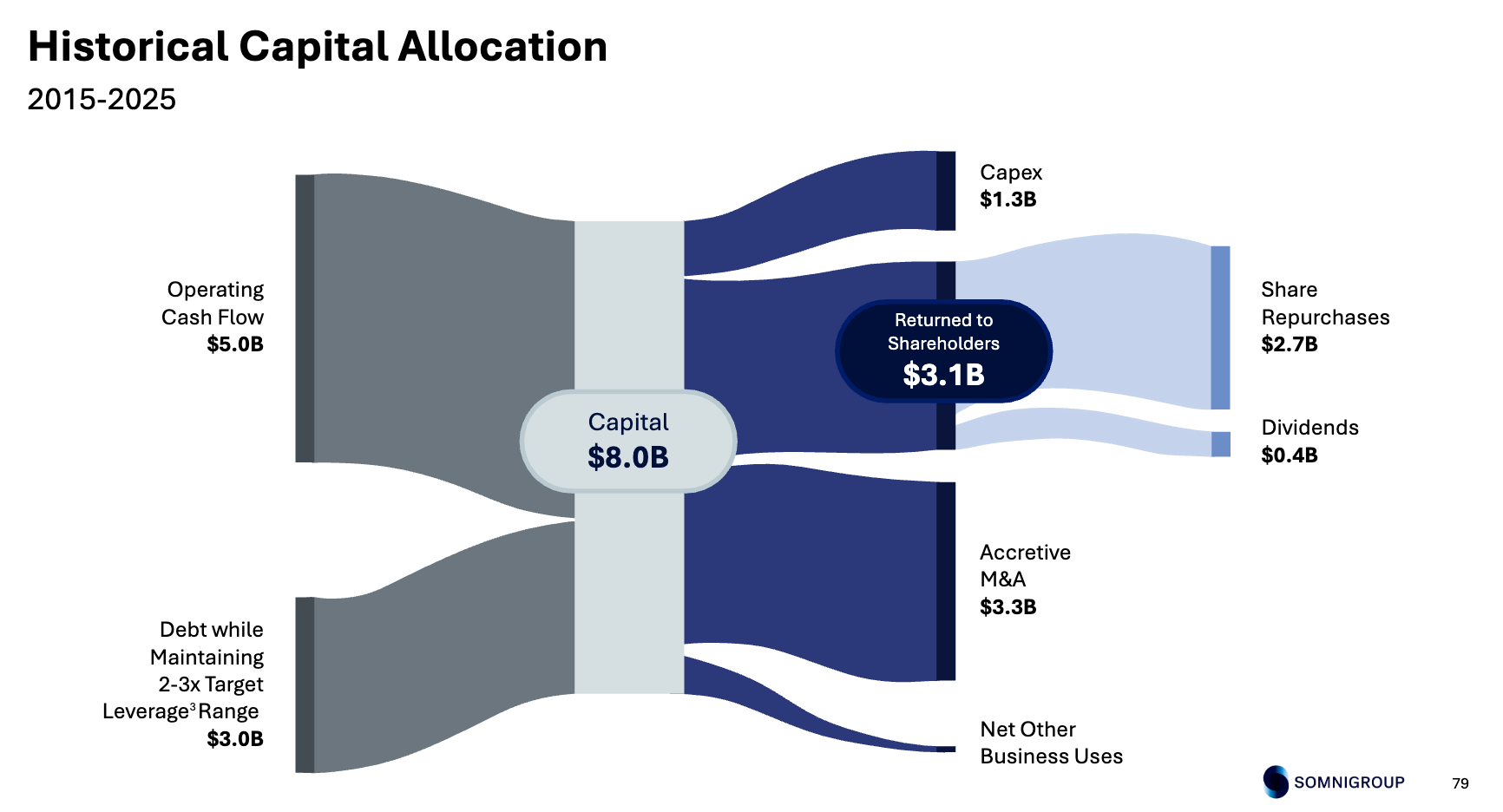

Along the way, management invested heavily in buybacks, levering up the balance sheet to do so.

To recap — this is a high-teens EBITDA margin business with low capex requirements (~2% of sales) and performing well during an industry downturn which sent at least 3 competitors into bankruptcy (Mattress Firm, Serta, Sleep Number).

So what’s the outlook from here?

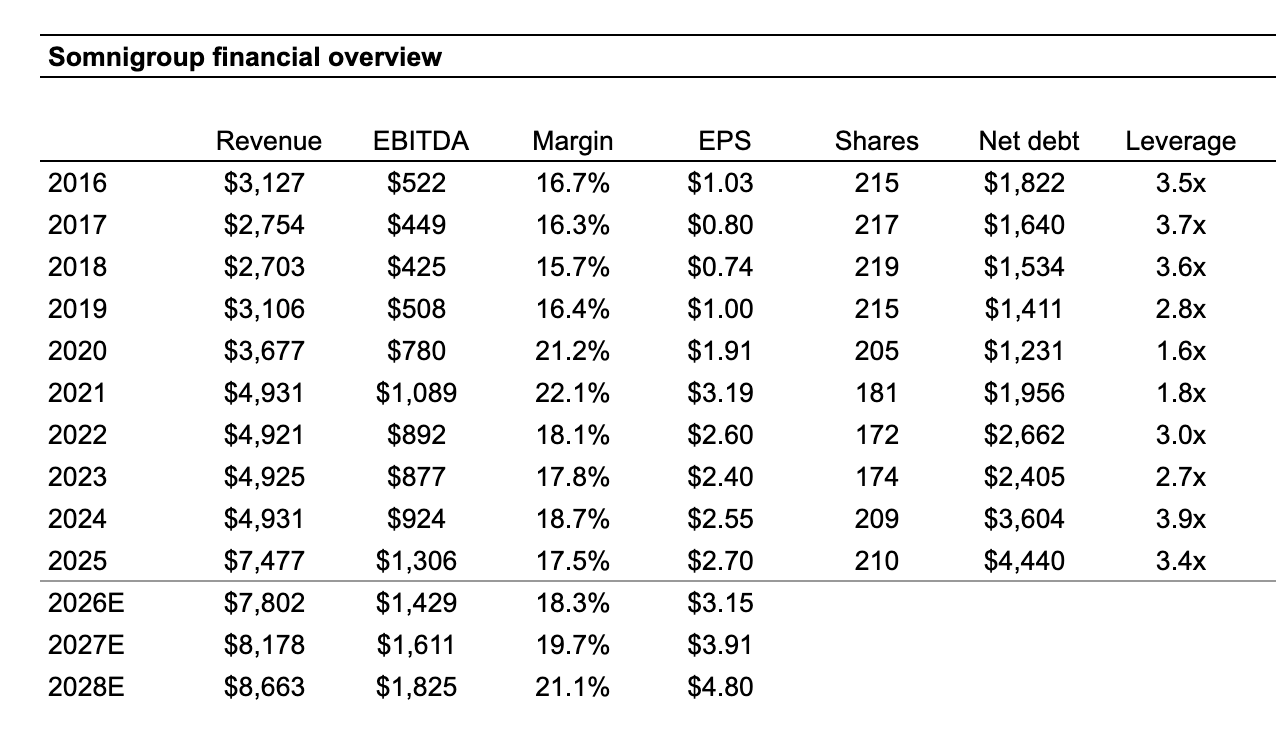

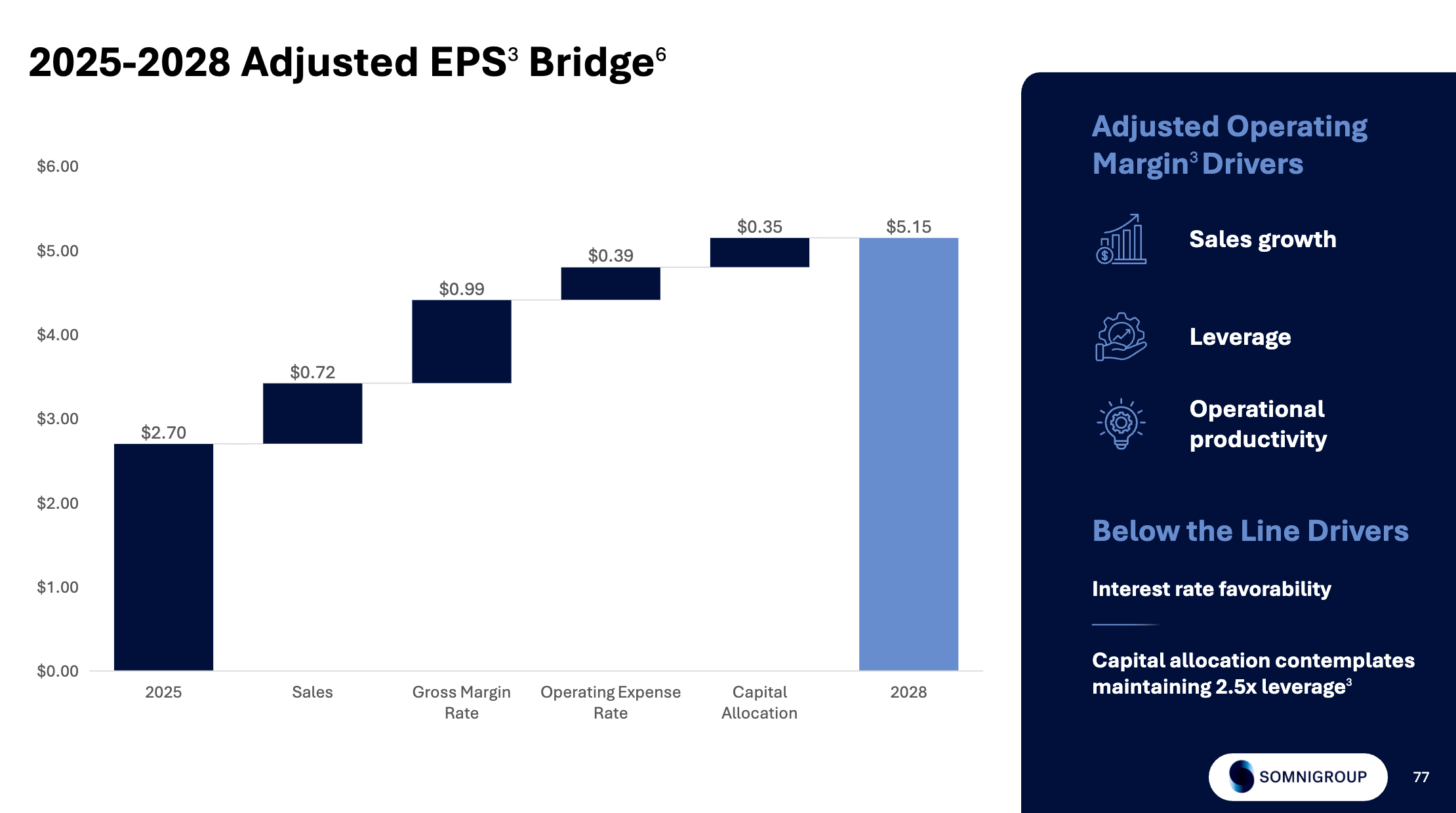

During a March 2026 investor day, management laid out 2026-2028 multi-year targets, including mid-single-digit sales growth and 20%+ EPS growth ending in $5.15 by 2028:

These multi-year targets anticipate a modest recovery in industry volumes (LSD growth), so it’s not baking in a full-blown “return to normal” scenario.

In the near term, 2026 guidance calls for $7.8bn sales (+4% YoY) and $3.00-3.40 EPS (+20% YoY). Not bad for the first full year after the Mattress Firm deal.

What about this Leggett (LEG) acquisition?

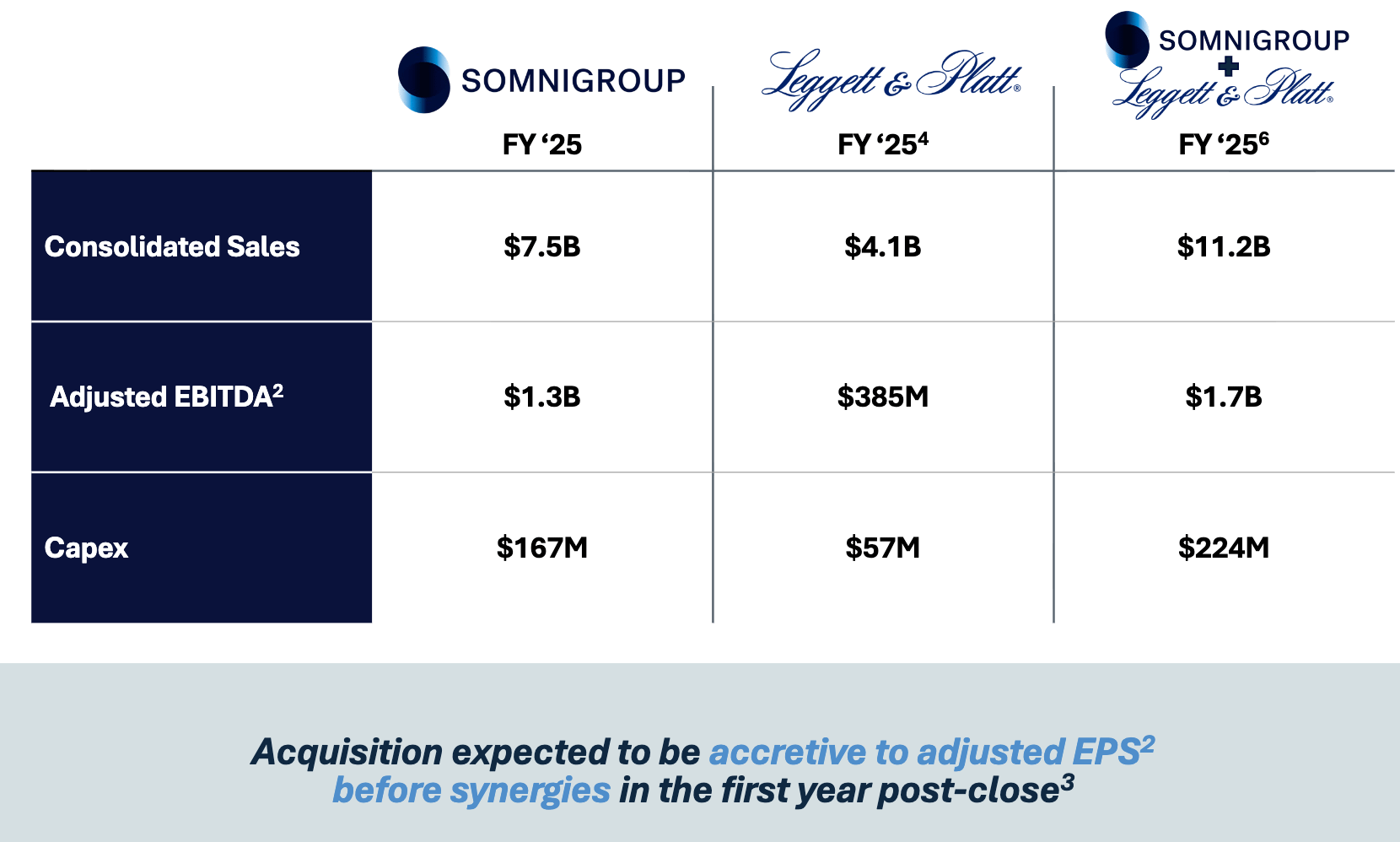

The $2.5bn all-stock deal is set to close by yearend 2026, after which SGI revenue will increase by 50% from $7.5bn to $11bn+

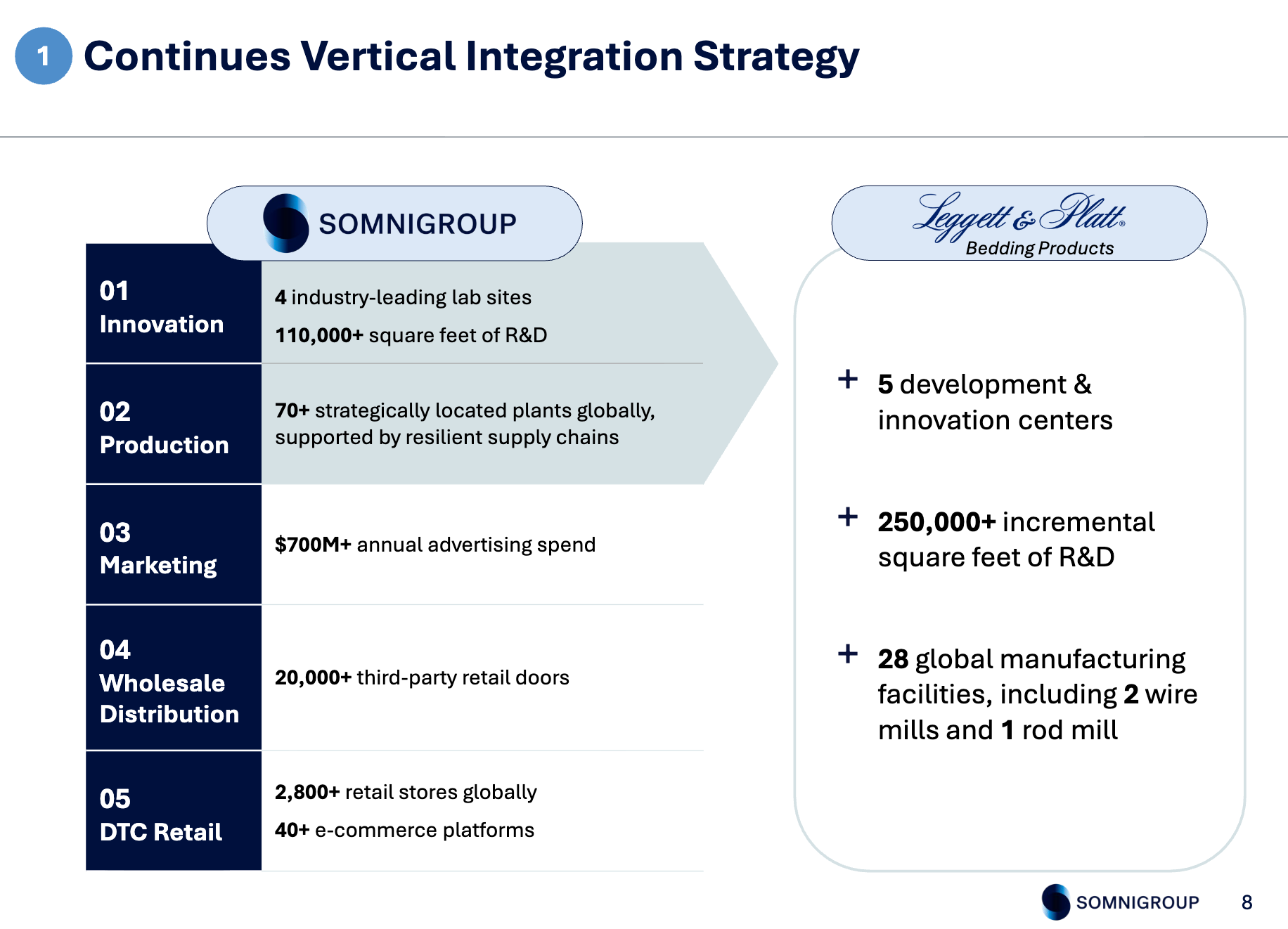

This acquisition adds deeper vertical integration into upstream components used in the bedding manufacturing process. LEG brings 28 manufacturing plants, 5 R&D centers, and several non-bedding business lines (auto, furniture, specialty products, etc.).

This is a really smart acquisition for SGI…

They are issuing ~20m shares while trading at ~24x 2026 EPS to buy a very cheap LEG at less than 6x EBITDA and 10-12x EPS.

Granted, LEG suffered much more than SGI as production levels declined since they produce input components used in the final assembly of mattresses like: rods, springs, and wire. As of today, LEG has delevered a ton and the business is stabilizing.

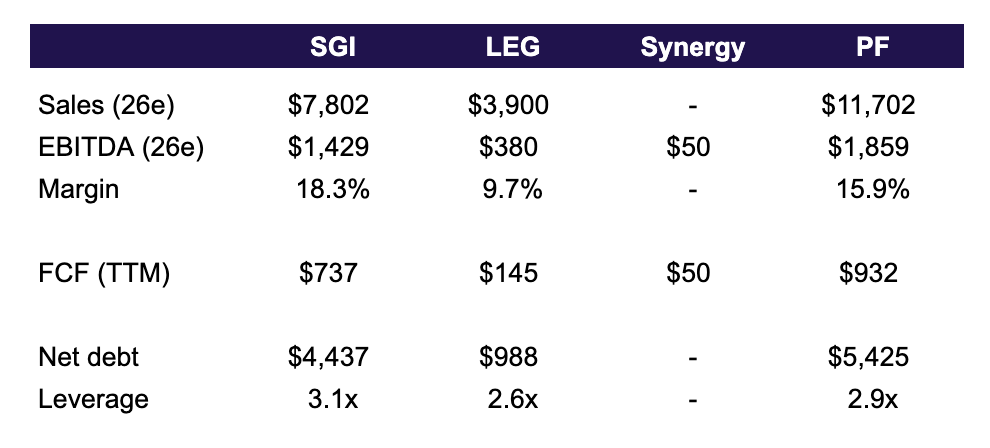

Pro-forma financial picture…

Once the deal closes, the pro-forma share count will increase to ~233m.

At $78, this leaves SGI at a ~$18bn market cap. Net debt jumps to ~$5.4bn for a $23.5bn pro-forma enterprise value.

Here’s my math when piecing these 2 together:

At a $23.5bn enterprise value, you’re getting SGI at 12.7x EBITDA and 20x P/FCF, certainly not cheap.

The real opportunity is the combination of normalizing industry volumes plus the LEG bargain acquisition…

And both management teams laid this case out with their financial projections in the merger proxy:

SGI management projections

LEG management projections:

Hmm…

So what could shares be worth?

Historically, SGI trades at a bit of a premium valuation: 16x P/E and 10x EV/EBITDA over the last 20-years:

Upside:

Let’s say legacy SGI hits $1.9bn EBITDA by 2028 and LEG chips in another $400m plus $50m in cost synergies = $2.45bn EBITDA by 2028. At 10x = $24.5bn EV (not far from today).

Assume debt remains unchanged at $5.4bn and you get $82 per share which is virtually unchanged from today.

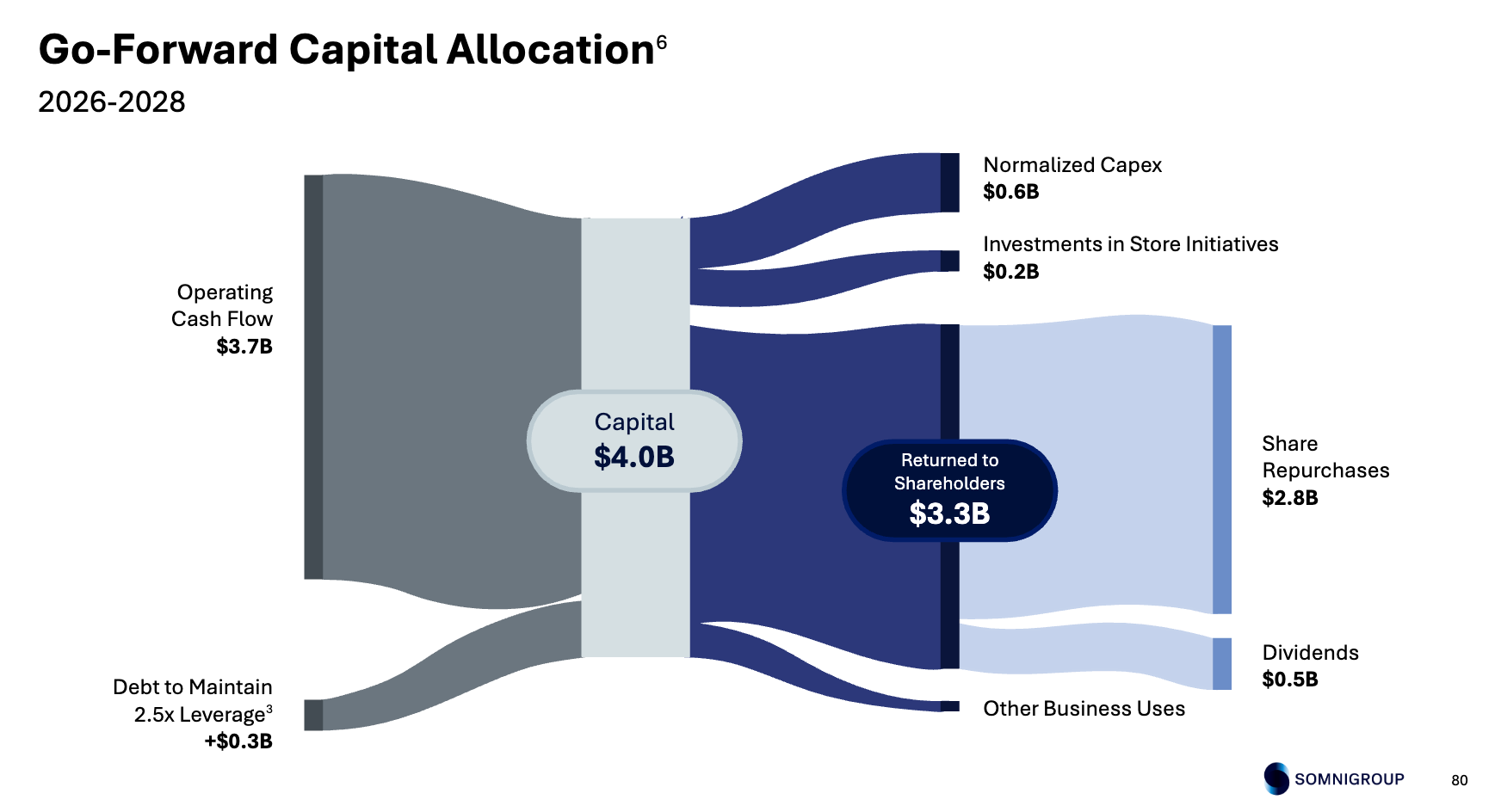

But this ignores any cash generation which is meaningful (see chart below) — standalone SGI expects $3bn cumulative FCF from 2026-2028 = $13 per share and let’s call it another $435m from LEG = $2 per share.

Valuing the business at $82 + cash flow at $15 = $97 per share by 2028 (+26% upside)

Downside — Using a downside multiple of 11.7x earnings and 8.1x EBITDA on 2026 pro-forma results ($930m FCF and $1.86bn EBITDA) = $41-46 per share (45% downside).

That’s an upside/downside ratio of ~0.6x, pretty unappealing…

Summing it up…

This is a fairly simple bet — deal integration plus macro recovery feeds into a multi-year earnings growth story.

And it’s only implying a partial industry recovery, so maybe you have some optionality if things improve more than expected. (Analyst estimates are only giving the company credit for $4.80 2028 EPS vs. the $5.15 target.)

The starting valuation is a bit rich for me and the risk/reward isn’t asymmetric enough. It’s unclear to me how industry volumes may continue shifting online, which might eventually kill some of Mattress Firm’s 2,000+ store base.

But it’s an interesting way to play a housing market recovery and simultaneously own the dominant player in a large industry.

I’m parking this one on the watchlist for now, but could get interested at a price in the $60s (risk/reward >2x).

Disclosure: no position in SGI or LEG

Resources: